Changes in the interest of borrowers

WHEN 23-year-old Khairul Osman got his first job after graduating from university last year, one of the first things he did was to buy a car.

Being a fresh graduate, he did not have the means to make a full cash settlement, so he did what most people would normally do. He applied for a loan from a bank.

A couple of years later, having saved some money, he wanted to pay off the loan.

However, a well-meaning friend advised him against it. The reason for this? Rule of 78.

Rule of 78 is a method of calculating loan interest where total interest is frontloaded in the early periods of a flat or fixed rate loan and any early settlement will not benefit the customer as there are no savings – negligible, if at all.

Last month, the Hire Purchase (Amendment) Bill 2025 was passed. It abolishes Rule of 78 and the use of a flat interest rate for, as the name suggests, hire purchase loans.

Under the amendment, the effective interest rate (EIR) and reducing balance method will be used instead of Rule of 78.

The market has welcomed this move, with many saying it has been long overdue.

Scrapping Rule of 78 is expected to enhance fairness and transparency in lending practices.

“It burdens borrowers because they pay higher interest charges at the beginning with little benefit if they repay in full ahead of schedule,” a former senior banker tells StarBiz 7.

He notes that if and when this is scrapped, it will enhance and promote consumer rights and transparency as well as ensure financial institutions offer a fair deal to their clients.

“Most consumers are not even aware of the significance of Rule of 78,” he says.

Lenders have a grace period of 18 months to comply with the new ruling.

Similarly, the government has passed the Consumer Credit Bill 2025, which establishes a fresh regulatory framework for the credit sector which includes personal loans.

“The lower-income or less-informed customers who were previously disadvantaged by not knowing the financial implication of front-loaded interest computations will now have additional information that best suit their financial needs,” says the senior banker.

This not only promotes greater transparency but also encourages early debt repayment, which can lead to personal financial improvement, he adds.

“Overall, it can promote greater fairness and trust in the financial system.”

Jimmy Tee, partner, assurance – financial services at PwC Malaysia, reckons this development is a milestone in structuring and regulating credit, enhancing transparency in the system that determines interest payments.

He notes that Rule of 78 makes early loan settlement less attractive to consumers. This has been the main catalyst for the shift from Rule of 78 in many economies such as the United States, the United Kingdom, European Union and Australia, particularly for consumer loans.

“From a country perspective, it presents tangible financial and social benefits and potentially speeds up the replacement cycle for motor vehicle ownership as consumers can make early settlements with less worry about the additional interests paid due to early settlement,” Tee says.

He notes that financial institutions can take advantage of the 18-month grace period to get operationally ready and educate consumers on how they will be impacted by these changes.

RAM Ratings senior vice-president of financial institution ratings Wong Yin Ching says it is a positive step for borrowers, although it remains crucial to continue fostering financial literacy and credit awareness.

“The reform also aligns Malaysia’s consumer credit framework with global best practices adopted by advanced markets that have moved towards more equitable and transparent lending standards,” says Wong.

KPMG in Malaysia head of financial services Kevin Foo says the removal of Rule of 78 ensures that interest is calculated based on the actual outstanding loan balance rather than predetermined allocations.

“This change offers greater equity to borrowers who choose early settlement. It promotes more transparent lending practices, and may enhance borrower confidence and encourage more prudent financial management.”

Foo notes that this is in line with Bank Negara Malaysia’s push for ethical lending and consumer protection. Interestingly, it could lead to reforms in other financing products, further developing Malaysia’s financial landscape.

The country’s automotive industry may also benefit, as consumers could be encouraged to replace or trade in their vehicles after repaying their loans earlier, Foo adds.

Like the rest, Ernst & Young PLT Malaysia deputy assurance leader and partner Datuk Megat Iskandar Shah says the rationale behind this legislative change is to primarily improve transparency.

“The EIR method truly reflects the financing cost borne by customers and is consistently applied for many other banking products such as mortgages, fixed deposits, current & savings accounts.”

He points out even in Singapore, loans have already transitioned to EIR-based calculations for hire purchase loans, reflecting a more mature and transparent financial system.

Shift in profit structure

While it is quite clear that abolishing Rule of 78 and using a flat interest rate will more often than not, benefit consumers, the question now is will banks have to bear the brunt?

Not necessarily, the experts say, but there may be some changes that lenders will have to embrace.

The ex-senior banker says abolishing Rule of 78 will first and foremost, significantly change how banks manage their interest revenue.

“Under Rule of 78, banks front-load interest income, securing a larger share at the beginning of the loan term, benefiting their bottom line enormously.

“Removing this system might lead to higher early loan repayments and increased portfolio turnover, as borrowers will no longer be penalised with hefty interest payments upfront.”

He says this will likely diminish immediate interest income and banks may experience a shift in profit structure, potentially lowering overall profits.

However, this will also encourage more responsible borrowing and early settlement behaviour, he adds.

“It might even lead to fewer cases of non-performing loans.”

Hong Leong Investment Bank analyst Raymond Ng Ing Yeow says the impact on banks’ bottom line is expected to be insignificant.

“This is because the rule’s abolishment will be implemented prospectively, applying only to new loans, and not retrospectively to existing ones.

“The new structure will incentivise banks to deploy capital elsewhere when existing loans are settled early.

“Furthermore, we believe the introduction of new financing products is likely to be on the cards, which involve setting higher interest rates for loans with flexible tenures, whilst offering lower rates to customers who commit to avoiding early settlement,” Ng says.

The senior banker concurs with Ng, adding that banks need to adjust their product pricing and risk management strategies to cope with any decreased upfront interest income.

“The transition period might see some product price adjustments to preserve profitability, whereby the industry will need to figure out the best course of action moving forward,” he says.

He warns that the regulators need to be mindful and prevent any “new fees” to make up for the loss of upfront interest income.

All said, Ng agrees this is a structural improvement in Malaysia’s retail credit framework and supports more efficient household deleveraging while reducing cost asymmetry for early settlement, particularly among lower-income borrowers.

“From a macro perspective, the move complements broader financial sector reforms aimed at improving consumer protection and fostering inclusive credit growth, without materially disrupting bank earnings. Over time, it may contribute to healthier credit behaviour and improved trust in formal lending channels,” Ng adds.

RAM’s Wong also says the abolishment of the Rule of 78 and flat-rate method for computing hire purchase and personal loan interest is expected to have minimal impact on banks’ profitability. “The policy will only apply to new facilities once implemented and will not affect existing loans.”

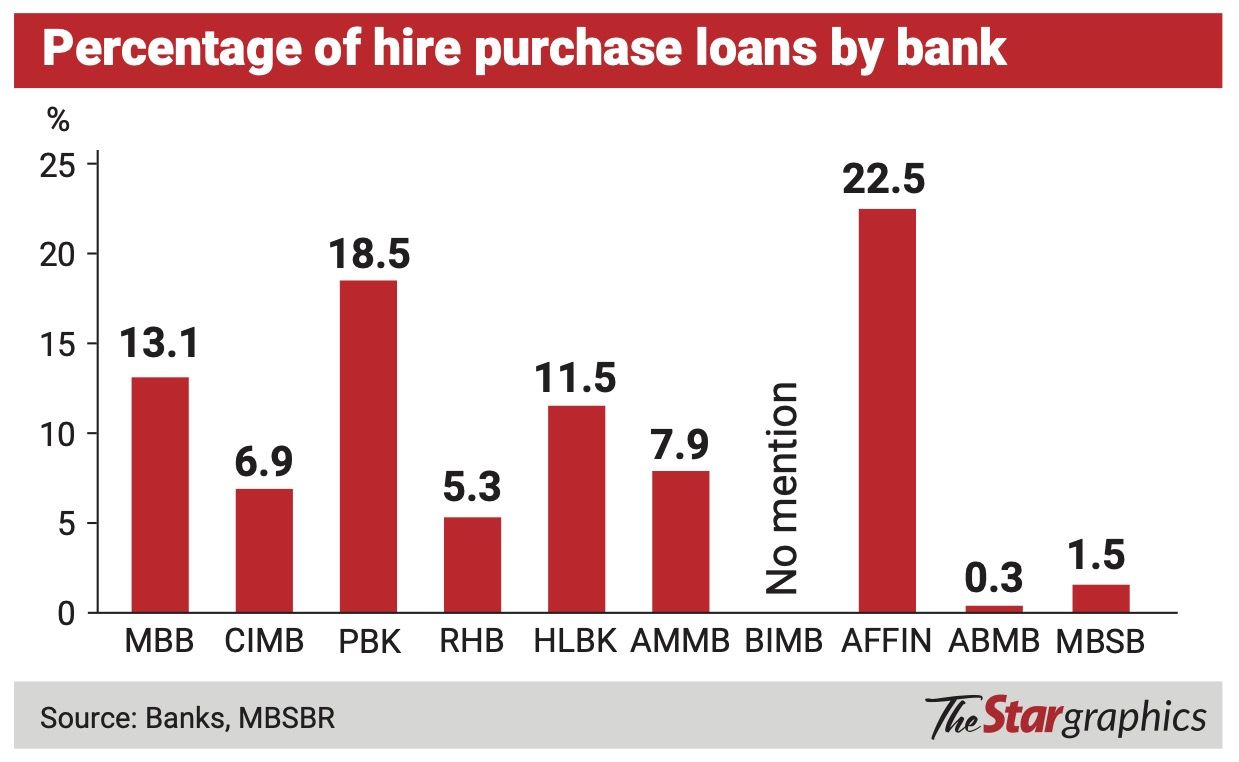

Hire purchase loans – 10% of total system

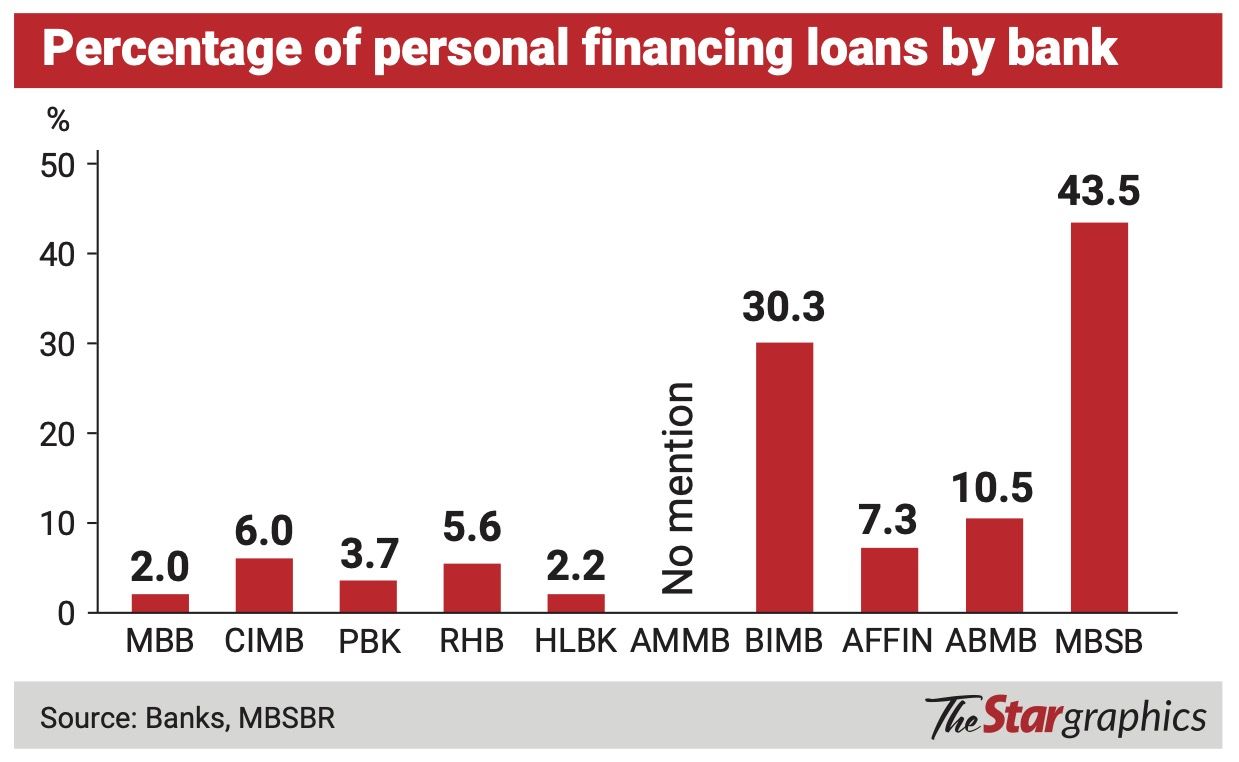

Wong notes hire purchase financing currently constitutes around 10% of total system loans, while personal financing accounts for 5%, a significant share of which is already on variable rates.

“Moreover, banks have been recognising interest income based on the EIR method since the adoption of the Malaysian Financial Reporting Standards (MFRS) 9 in early 2018.

“Hence, when comparing the Rule of 78 and flat-rate methods (which front loads interest charged) with the proposed reducing balance approach, any potential adverse impact on bank earnings would only arise in cases of early loan settlement by borrowers,” she adds.

PwC’s Tee also points out that banks have been reporting under the MFRS International Financial Reporting Standards (IFRS) equivalent, and the recognition basis of the interest income has been adjusted to be aligned with the EIR basis.

“Encouragingly, there will be minimal impact on the profitability of banks with the abolishment of Rule of 78,” he says, adding that there may be some loss of income for banks arising from customers who opt for early settlement.

Typically, the early settlement calculation under Rule of 78 will result in a higher settlement amount as compared to the reducing balance approach, he adds.

KPMG’s Foo also notes that with the abolishment of Rule of 78, banks will no longer enjoy the advantage of collecting a larger portion of interest upfront from hire purchase and personal financing borrowers.

“However, since these loans represent a smaller share of banks’ overall profit, the impact on profitability should be minor.

“Instead, the change could promote more transparent lending practices, strengthen customer trust, and enhance banks’ long-term resilience,” Foo says.

Like Wong, he notes that it aligns Malaysia’s lending framework with international best practices by ensuring that interest is calculated based on the actual outstanding loan balance.

In terms of other changes that financial institutions may have to embrace is to upgrade or modify their accounting systems to accommodate the abolishment of Rule of 78, especially for hire-purchase and personal financing products.

“Banking systems will need to be reconfigured to support the remaining balance method, which is more complex and requires real-time recalculations. Legacy infrastructure built around Rule of 78 may not be compatible with the new approach without significant updates,” Foo adds.

Currently, the lenders with the most exposure to hire-purchase loans are Affin Bank Bhd, Public Bank Bhd, Hong Leong Bank Bhd and Malayan Banking Bhd.

It will be interesting to see how these financial institutions plan their strategies around this latest development within the banking sector.

Will they come out with new, more “expensive” financial products or will this set the precedent for better value products?

One thing’s almost certain – customers will enjoy more transparency when it comes to loan payments, and those who adopt strict fiscal discipline will reap the rewards.