Alaska Air Group (ALK): Reassessing Valuation After Q4 Guidance Cut and Operational Disruptions

Alaska Air Group (ALK) just slashed its Q4 earnings outlook after a rough stretch that combined an internal IT outage, government driven flight cancellations, and higher fuel costs, forcing investors to reassess near term expectations.

See our latest analysis for Alaska Air Group.

Even with the guidance cut, the stock has bounced hard in the near term, with a 7 day share price return of 15.84 percent and a 3 year total shareholder return of 11.42 percent. This suggests momentum is cautiously rebuilding after a tough year.

If this rebound has you rethinking airlines and travel, it might be worth scanning other aerospace and defense stocks to see how the broader transportation and defense space is repricing risk and opportunity.

With earnings guidance reset and analysts still seeing more than 30 percent upside to their price targets, the key question now is whether Alaska Air shares remain undervalued or if the market has already priced in the recovery story.

Most Popular Narrative: 24.4% Undervalued

With Alaska Air Group closing at $49.65 against a narrative fair value of about $65.71, the story hinges on sustained growth in premium demand and loyalty economics.

The analysts have a consensus price target of $66.286 for Alaska Air Group based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $80.0, and the most bearish reporting a price target of just $56.0.

Want to see what has analysts modeling a step change in earnings power, richer margins, and a future multiple below today’s industry norm, all at once? Read on.

Result: Fair Value of $65.71 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, rising unit costs and integration hiccups at Hawaiian could easily erode the expected margin gains that underpin the current upside narrative.

Find out about the key risks to this Alaska Air Group narrative.

Another Angle on Valuation

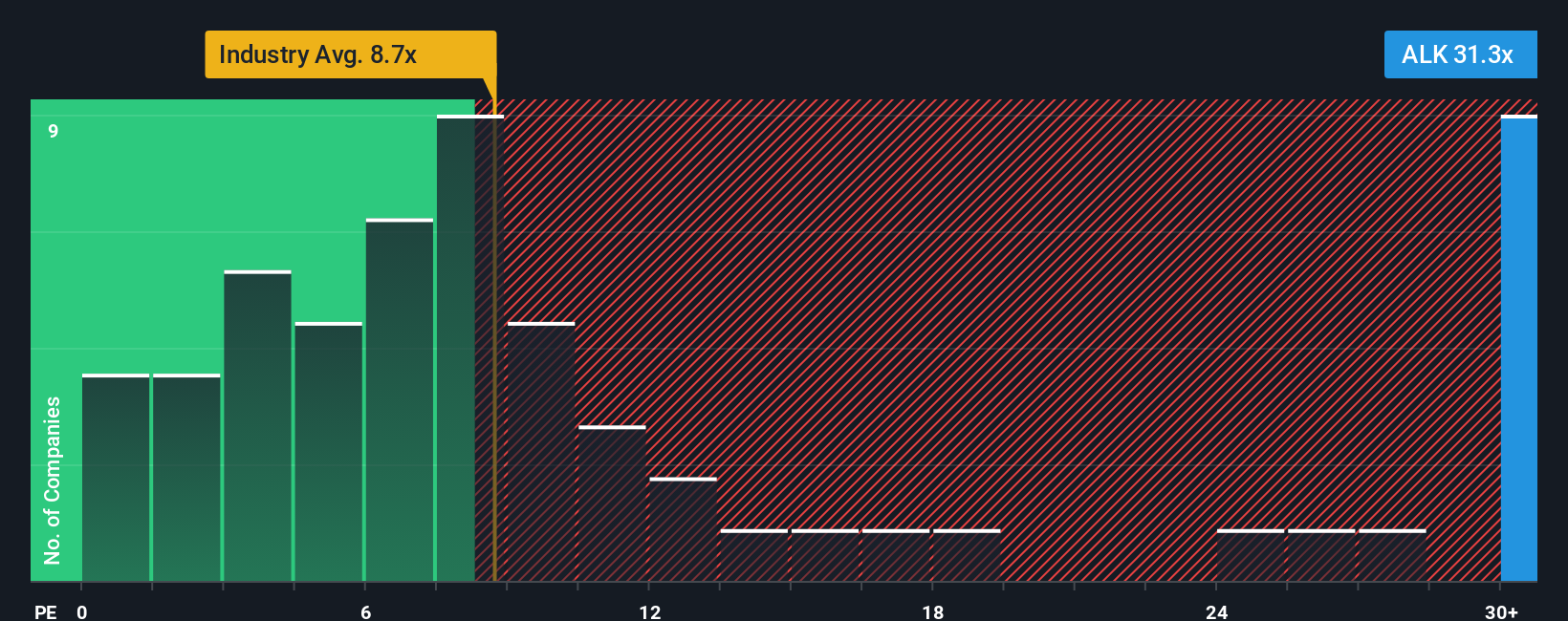

While narrative fair value points to upside, the earnings multiple tells a tougher story. Alaska Air trades on a P/E of 38.4 times, far richer than both the global airlines average of 9.1 times and its own fair ratio of 56.6 times. This raises questions about valuation risk if growth stumbles.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Alaska Air Group Narrative

If you see the story differently or want to stress test the numbers yourself, you can build a fresh narrative in just minutes: Do it your way.

A great starting point for your Alaska Air Group research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Ready for more actionable investment ideas?

Before you move on, use the Simply Wall St Screener to uncover fresh opportunities that match your style, so you are not leaving potential returns on the table.

- Capture early stage growth stories by reviewing these 3575 penny stocks with strong financials that pair speculative upside with improving fundamentals and stronger balance sheets.

- Capitalize on the AI revolution through these 26 AI penny stocks riding structural demand for automation, data infrastructure, and intelligent software solutions.

- Lock in reliable income potential by targeting these 15 dividend stocks with yields > 3% that combine solid payouts with sustainable cash flows and resilient business models.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com