Another mart in the market

CONVENIENCE stores and mini-marts may appear similar – but they are not.

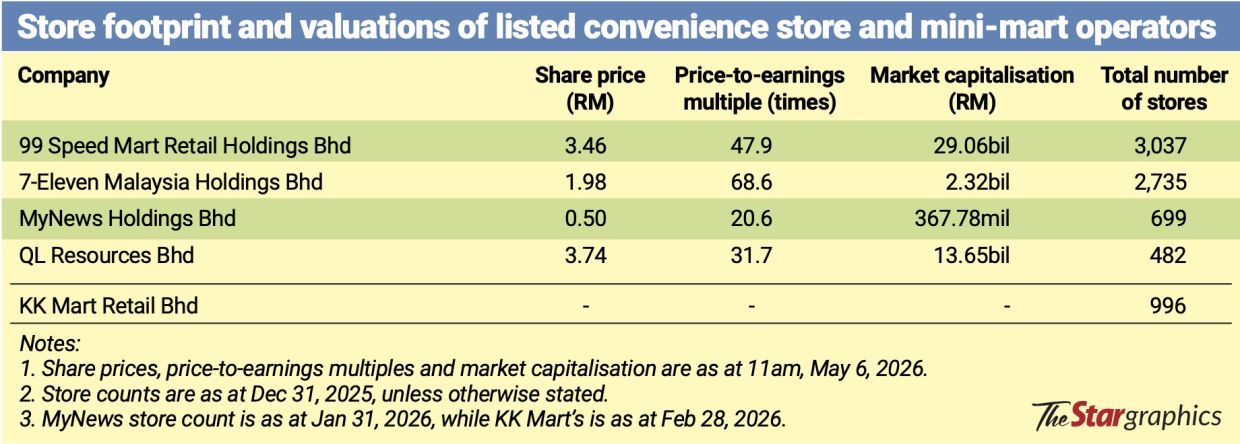

In Malaysia’s listed retail scene, differences in operating models, basket size and growth trajectories translate into very different valuations (see table).

The listing has naturally drawn comparisons with 99 Speed Mart Retail Holdings Bhd among investors, as both operate grocery-based retail networks and fall under Bursa Malaysia’s consumer products and services sector.

But beyond the shared classification, analysts and fund managers say the two operate on distinct retail models.

Different retail models, different economics

KK Super Mart operates a 24-hour convenience store model focused on quick, small-basket purchases, while 99 Speed Mart runs a 13-hour mini-market format targeting household stock-up shopping with higher transaction values.

99 Speed Mart’s average basket size stood at RM21.70 in 4Q25, about double KK Super Mart’s average transaction value of RM10.45.

Fund managers say this difference also extends into valuation.

Based on its financial year ended June 30, 2025 (FY25) earnings per share of 2.77 sen, KK Mart could potentially command an IPO valuation of about 97 sen per share if priced at around 35 times earnings (broadly in line with 99 Speed Mart’s IPO multiple), implying a market capitalisation of roughly RM3.4bil upon listing.

Still, market participants caution that a direct comparison may oversimplify differences in scale, liquidity and operating quality between the two retailers.

One fund manager says KK Mart is likely to be priced at a discount to 99 Speed Mart given its smaller scale, lower liquidity and more concentrated ownership structure.

“I would value KK Mart at a substantial discount to 99 Speed Mart as it will be significantly smaller and will not be an index play,” he says, adding that KK Mart may not benefit to the same extent from broad-based consumer support programmes such as Sumbangan Asas Rahmah cash assistance.

“Also, the distant number two in each sector normally trades at a sizeable discount to the sector leader.”

At the time of writing, 99 Speed Mart was trading at RM3.37 a share, giving it a market capitalisation of RM28.39bil.

According to Bloomberg data, it was valued at about 47 times trailing earnings and 38 times forward earnings.

Another fund manager notes that valuation support for retail stocks is also shaped by investor base and liquidity considerations.

“When big funds go large in the consumer sector, they generally prefer large-cap names because of liquidity. Foreign funds in particular are unlikely to look at smaller caps unless they are specifically mandated to do so.”

He adds that this helps explain why larger peers such as 99 Speed Mart tend to attract broader institutional participation.

“I do think 99 Speed Mart deserves a higher valuation because of its market cap, liquidity and size. Smaller caps typically come with liquidity constraints.

“Still, the growth rate by small cap companies should be faster than the big cap.”

He says valuation should also take into account historical performance rather than forward assumptions alone, including how quickly stores ramp up and recover their investment costs.

Earnings trends and past performance

KK Super Mart has steadily expanded its store network from 547 outlets in mid-2022 to 996 as of February 2026, effectively nearly doubling its footprint over four years, with annual additions ranging from about 100 to 130 stores per year.

99 Speed Mart, meanwhile, has grown from 2,024 stores in end-2021 to 3,037 outlets by end-2025, adding more than 1,000 stores over the same period, albeit from a significantly larger base.

Separately, a research analyst notes that while KK Mart’s IPO valuation will naturally be benchmarked against 99 Speed Mart, the two are not directly comparable in terms of earnings quality.

“They serve different shopping needs, with customers spending roughly half as much per visit at KK Mart versus 99 Speed Mart,” she notes.

At current trading levels, she adds that simply applying 99 Speed Mart’s valuation multiple to KK Mart may not fully capture the picture, given its smaller store revenues and recent softness in existing outlet performance.

KK Mart’s net profit fell 4.5% to RM96.99mil in FY25, from RM101.6mil a year earlier, as store-level performance softened.

Average daily transactions per store declined to 465 in FY25 from 502 in the previous financial year, while average daily sales per outlet eased to RM4,865 from RM5,304.

“Investors will likely want more comfort on whether that sales momentum can recover before forming a strong view on what KK Mart is worth.”

KK Mart’s proposed listing comprises an offer for sale of up to 630 million existing shares and a public issue of 210 million new shares.

The exercise also includes a placement to two cornerstone investors, whose identities have not been disclosed in the prospectus exposure.

Selling shareholders include founder and group managing director Datuk Seri Chai Kee Kan and his wife Datin Seri Loh Siew Mui, via K8 Resources Bhd, with their combined stake expected to fall to as low as 71.85% post-listing, from 95.05% previously.

KK Super Mart traces its origins back to 2001, when it began as a small partnership store in Kuchai Lama, Kuala Lumpur, operating from a shoplot and focusing on sundry and grocery retailing.

Today, the group operates a nationwide network of about a thousand stores, supported by a single distribution centre in Balakong Jaya, Selangor.

Its footprint spans all states except Perlis, Kelantan, Terengganu and Sabah, with about 67.9% of outlets concentrated in Kuala Lumpur and Selangor.

On the supply chain side, KK Mart works with about 520 local suppliers and manages approximately 6,852 stock keeping units (SKUs), with around 38% of the SKUs distributed through its Balakong distribution centre.

Expansion strategy

KK Mart is targeting to surpass 1,500 stores by FY28, supported by plans to open about 302 new stores over the next 15 months.

Each new store typically requires a capital expenditure (capex) of about RM200,000 to RM300,000, excluding inventory, with initial stocking costs of around RM230,000 per outlet.

Accordingly, the group estimates the total capex for the planned opening of 302 new stores, including initial inventory, at about RM145mil.

To support its long-term expansion, KK Mart plans to relocate its Balakong distribution centre to a larger facility in the Klang Valley by end-2027.

It also aims to strengthen its logistics network through a hub-and-spoke model, including the rental of additional distribution centres in Penang and Johor by end-2029.

The timing of KK Mart’s proposed listing comes amid a softer backdrop for consumer stocks on Bursa Malaysia.

Bursa Malaysia’s Consumer Products and Services Index, which has a combined market capitalisation of about RM269bil, was trading at 512.2 on Wednesday, down 4.62% year-to-date.

The index has remained relatively flat over the past year, rising just 0.9% from 507.65 previously, after reaching a recent peak of 564.31 on Jan 27, 2026.

The sector currently trades at a price-to-earnings multiple of about 26 times.

Still, market observers point out that the proposed listing environment is considerably more favourable than a year ago, when KK Mart was dealing with reputational pressures and boycott calls arising from a product controversy that had weighed on public sentiment towards the retailer.