Does Jujiang Construction Group (HKG:1459) Have A Healthy Balance Sheet?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Jujiang Construction Group Co., Ltd. (HKG:1459) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does Jujiang Construction Group Carry?

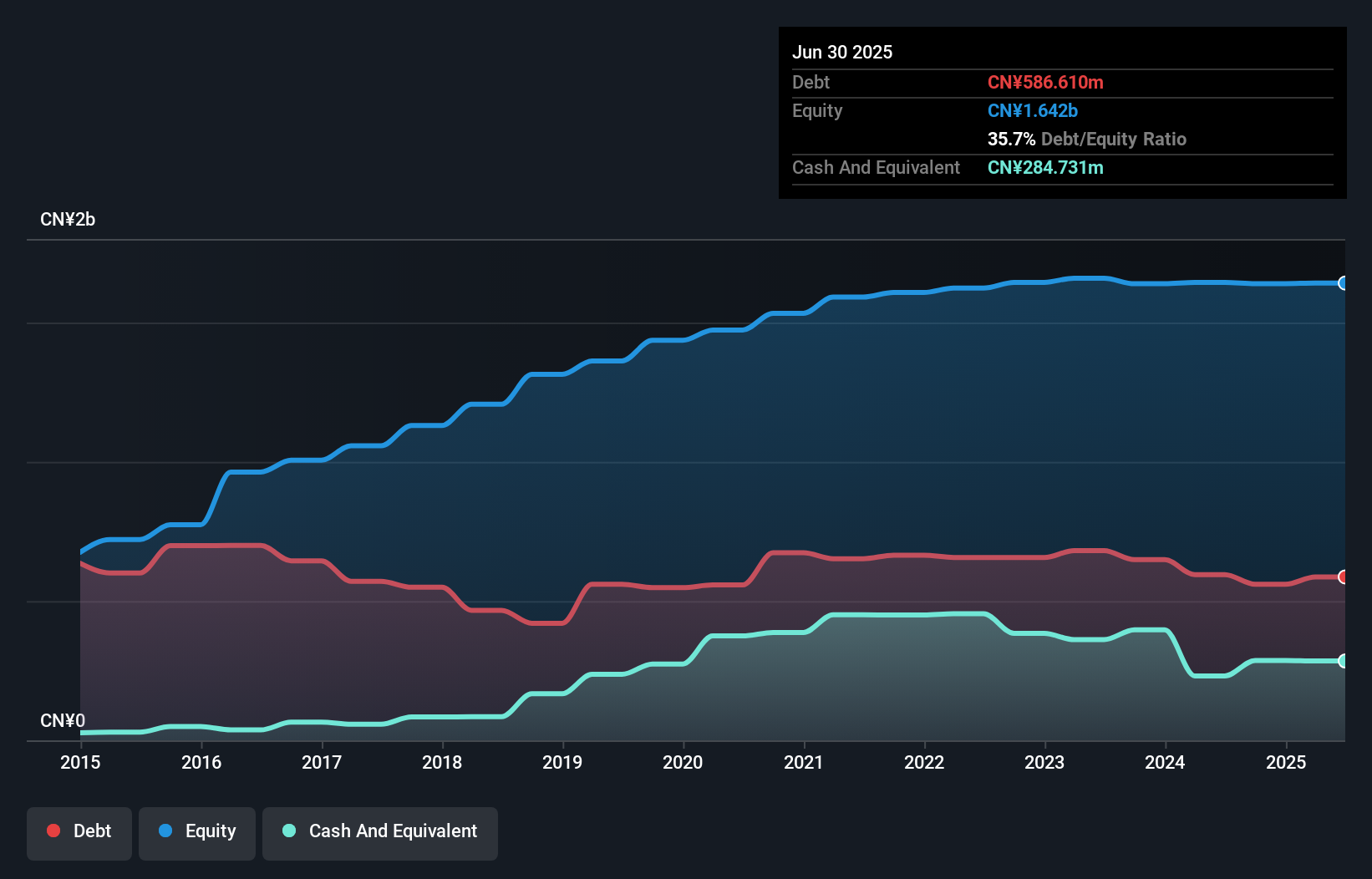

As you can see below, Jujiang Construction Group had CN¥586.6m of debt, at June 2025, which is about the same as the year before. You can click the chart for greater detail. However, it does have CN¥284.7m in cash offsetting this, leading to net debt of about CN¥301.9m.

A Look At Jujiang Construction Group's Liabilities

Zooming in on the latest balance sheet data, we can see that Jujiang Construction Group had liabilities of CN¥4.50b due within 12 months and liabilities of CN¥97.5m due beyond that. Offsetting this, it had CN¥284.7m in cash and CN¥5.02b in receivables that were due within 12 months. So it can boast CN¥700.1m more liquid assets than total liabilities.

This excess liquidity is a great indication that Jujiang Construction Group's balance sheet is almost as strong as Fort Knox. Having regard to this fact, we think its balance sheet is as strong as an ox. When analysing debt levels, the balance sheet is the obvious place to start. But it is Jujiang Construction Group's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

View our latest analysis for Jujiang Construction Group

Over 12 months, Jujiang Construction Group made a loss at the EBIT level, and saw its revenue drop to CN¥5.3b, which is a fall of 34%. That makes us nervous, to say the least.

Caveat Emptor

While Jujiang Construction Group's falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. Indeed, it lost CN¥4.0m at the EBIT level. Having said that, the balance sheet has plenty of liquid assets for now. That should give the business time to grow its cashflow. The company is risky because it will grow into the future to get to profitability and free cash flow. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Be aware that Jujiang Construction Group is showing 2 warning signs in our investment analysis , and 1 of those makes us a bit uncomfortable...

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.