PVH (PVH) Is Down 7.4% After Earnings Beat But Margin Squeeze - Has The Bull Case Changed?

- PVH Corp. reported third-quarter 2025 sales of US$2,294.3 million, slightly above last year, but net income fell to US$4.2 million and diluted EPS from continuing operations dropped to US$0.09, while confirming only slight revenue growth for the upcoming quarter.

- Despite beating its own guidance and continuing a long-running share repurchase program that has retired 64.52% of shares since 2015, PVH flagged ongoing margin pressure from tariffs and supply chain transitions, highlighting the gap between brand momentum and current profitability.

- We’ll now examine how PVH’s earnings beat but cautious guidance and operational headwinds affect its longer-term investment narrative.

Find companies with promising cash flow potential yet trading below their fair value.

PVH Investment Narrative Recap

To own PVH, you need to believe its Calvin Klein and Tommy Hilfiger brands can convert current “momentum” into healthier, more consistent profitability. The latest quarter reinforced that brand heat is intact, but the key near term catalyst is margin repair, which is still under pressure from tariffs and supply chain resets. That pressure, alongside softer earnings and unchanged near term revenue guidance, keeps execution risk around margins as the biggest issue to watch.

Against that backdrop, the completion of a long-running buyback that has retired 64.52% of shares since 2015 stands out. While the repurchases do not fix the tariff and operational headwinds, they magnify the impact of any future earnings recovery per share, tying capital allocation directly to the same margin and growth levers that now need to work.

Yet investors should also be aware that PVH’s ongoing exposure to shifting global tariff regimes and the resulting margin strain could...

Read the full narrative on PVH (it's free!)

PVH’s narrative projects $9.4 billion revenue and $707.7 million earnings by 2028. This implies 2.3% yearly revenue growth and about a $239 million earnings increase from $468.5 million today.

Uncover how PVH's forecasts yield a $96.79 fair value, a 23% upside to its current price.

Exploring Other Perspectives

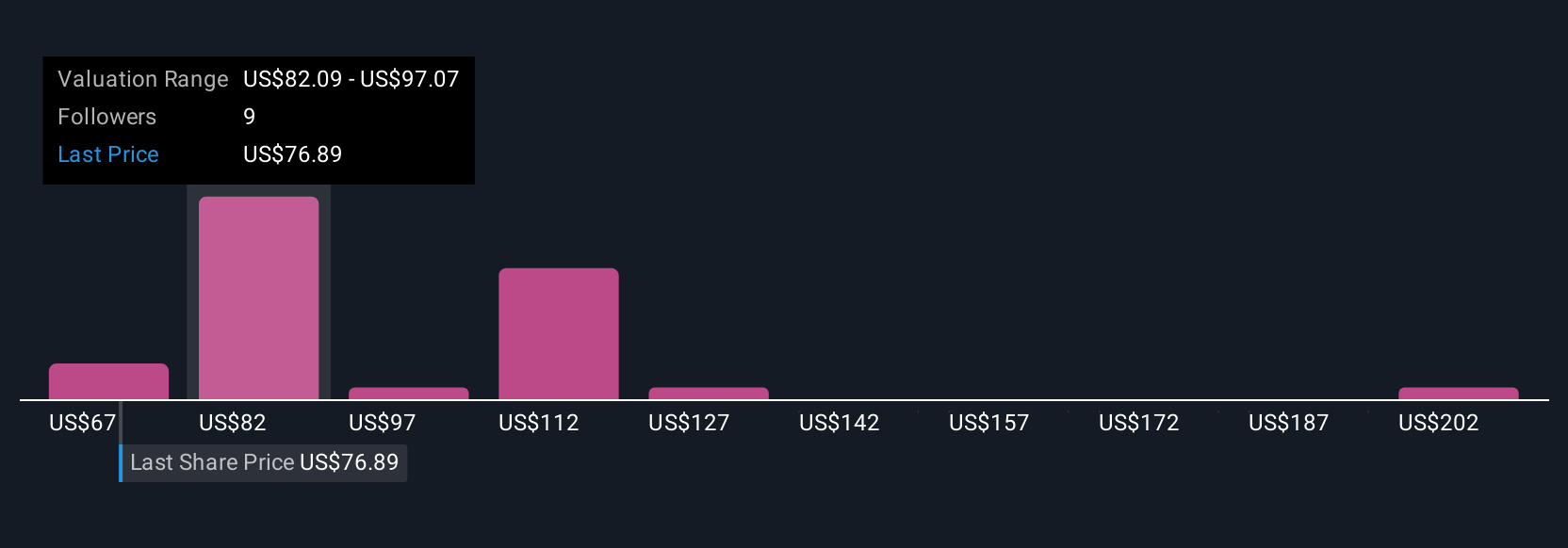

Seven members of the Simply Wall St Community estimate PVH’s fair value anywhere between US$67.10 and US$216.96, reflecting very different expectations. When you set those views against the current tariff driven margin pressure, it underlines how important it is to weigh several independent perspectives before deciding how PVH might fit into your own portfolio.

Explore 7 other fair value estimates on PVH - why the stock might be worth 15% less than the current price!

Build Your Own PVH Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your PVH research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free PVH research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate PVH's overall financial health at a glance.

Contemplating Other Strategies?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com