How Illumina’s (ILMN) Analyst Earnings Upgrade Will Impact Investors

- Illumina was recently upgraded to a Zacks Rank #1 (Strong Buy) after analysts steadily raised earnings estimates over the past three months, signaling a more favorable profit outlook.

- This shift in analyst expectations, including a consensus earnings estimate increase of 4.5%, highlights growing confidence in the company’s underlying business momentum.

- Now, we’ll explore how this recent earnings estimate upgrade and improving analyst sentiment interact with Illumina’s existing investment narrative.

Find companies with promising cash flow potential yet trading below their fair value.

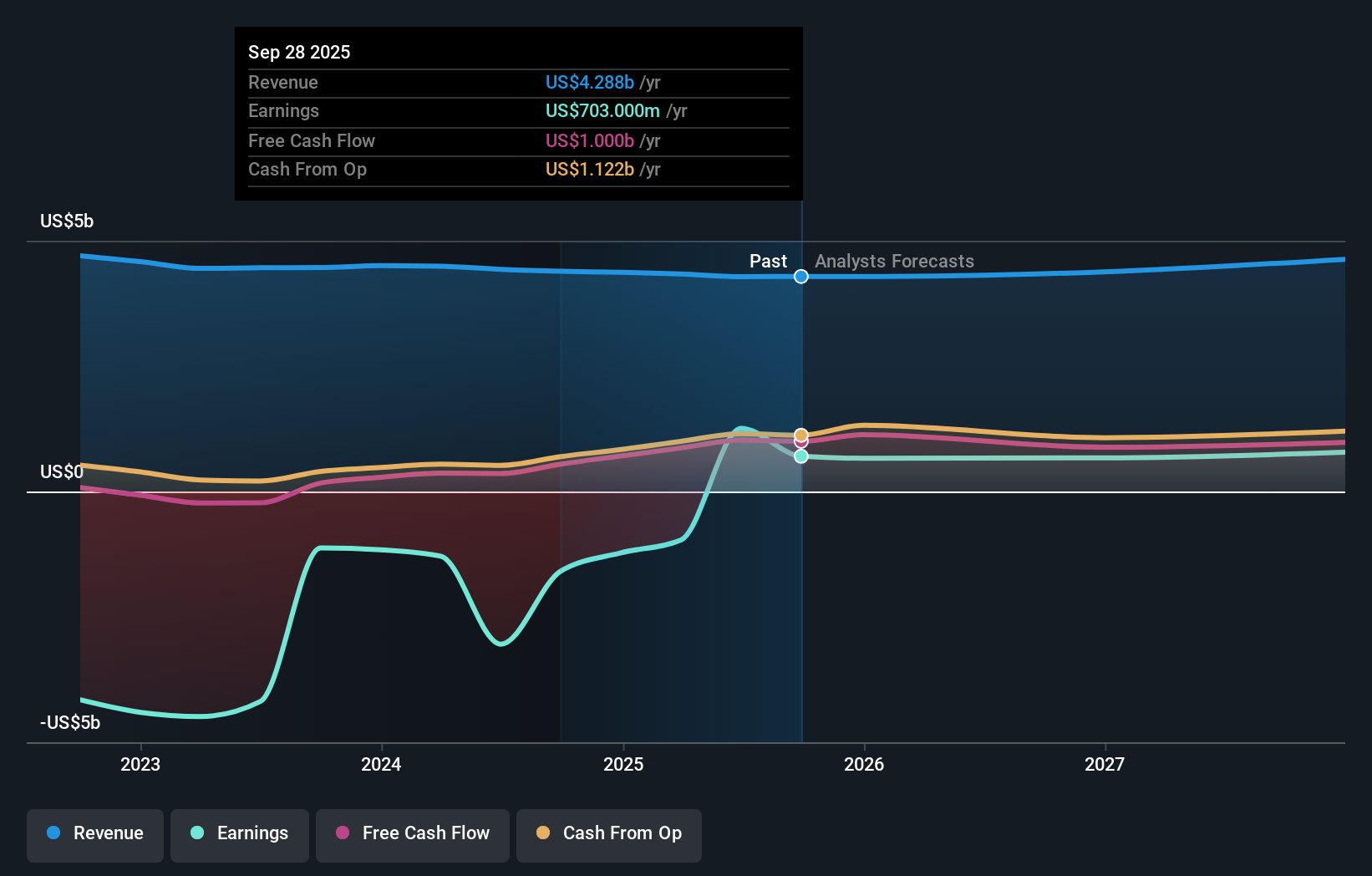

Illumina Investment Narrative Recap

To own Illumina, you generally need to believe in long term growth in sequencing and clinical genomics despite moderating revenue forecasts and intense competition. The recent Zacks Rank #1 upgrade reflects improved earnings expectations in the near term, but it does not materially change the key short term catalyst, which remains execution on higher margin clinical and multiomics opportunities, or the biggest risk, which is ongoing weakness and uncertainty in research and China demand.

The most relevant recent development alongside the upgraded earnings outlook is Illumina’s raised 2025 guidance, which pointed to a smaller core revenue decline and better visibility into the year. That guidance update, paired with analysts lifting earnings estimates, reinforces the idea that cost discipline and mix shift to clinical and multiomics can support profitability even while overall revenue growth remains modest and research budgets and Chinese demand stay under pressure.

Yet while sentiment has improved, investors should also be aware of how persistent funding and regulatory pressures could still weigh on...

Read the full narrative on Illumina (it's free!)

Illumina's narrative projects $4.8 billion revenue and $873.5 million earnings by 2028. This requires 3.6% yearly revenue growth and an earnings decrease of about $426.5 million from $1.3 billion today.

Uncover how Illumina's forecasts yield a $119.84 fair value, a 7% downside to its current price.

Exploring Other Perspectives

Four fair value estimates from the Simply Wall St Community span roughly US$102 to US$157 per share, highlighting how widely individual views on Illumina’s potential diverge. When you weigh those opinions against the recent earnings estimate upgrades and raised 2025 guidance, it becomes clear that examining multiple perspectives can help you think more critically about how execution and end market risks might shape the company’s longer term performance.

Explore 4 other fair value estimates on Illumina - why the stock might be worth 21% less than the current price!

Build Your Own Illumina Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Illumina research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Illumina research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Illumina's overall financial health at a glance.

Interested In Other Possibilities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com