KOSÉ (TSE:4922) Valuation Check After Prolonged Share Price Weakness and Mixed Growth Signals

KOSÉ (TSE:4922) has quietly slid over the past month, even as revenue and net income continue to grow year over year. This invites a closer look at whether the market is overly discounting its long term prospects.

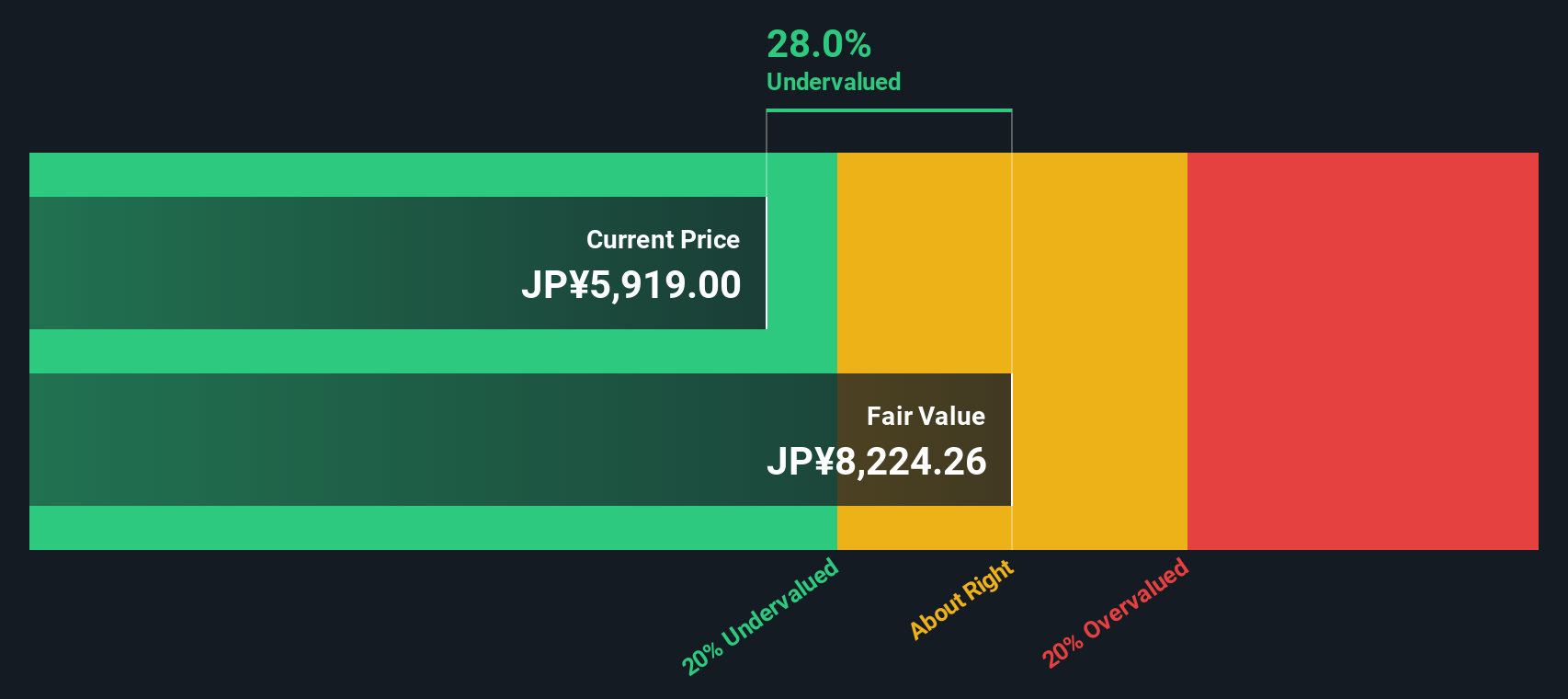

See our latest analysis for KOSÉ.

Despite solid revenue and net income growth, KOSÉ’s 30 day share price return of minus 9.79 percent and steep five year total shareholder return of minus 67.89 percent suggest sentiment is still cautious rather than improving.

If KOSÉ’s recent slide has you reassessing the sector, this could be a good moment to widen your watchlist and uncover opportunities among fast growing stocks with high insider ownership.

With the share price lagging both analyst targets and our estimate of intrinsic value despite improving fundamentals, investors now face a key question: is this a mispriced turnaround story, or is the market already discounting future growth?

Price to Earnings of 40x: Is It Justified?

KOSÉ is trading on a price to earnings ratio of 40 times, and that looks stretched when set against its weak long term share price performance.

The price to earnings multiple compares what investors pay today for each unit of current earnings. It is a key yardstick for mature, profitable consumer brands like KOSÉ. At 40 times earnings, the market is effectively placing a rich premium on each unit of profit, despite the company having seen earnings decline by 9.8 percent per year over the past five years and recording negative earnings growth of 5.6 percent over the last year.

Relative to both the personal products industry and valuation models, that premium stands out. The stock trades well above the Japan personal products industry average multiple of 24.4 times and the peer average of 24.5 times. It also exceeds an estimated fair price to earnings ratio of 30.1 times that our analysis suggests the market could reasonably converge toward if expectations moderate.

Explore the SWS fair ratio for KOSÉ

Result: Price to Earnings of 40x (OVERVALUED)

However, risks remain, including potential margin pressure in a competitive beauty market and the possibility that analyst optimism fades if earnings growth disappoints.

Find out about the key risks to this KOSÉ narrative.

Another View: DCF Points to a Very Different Story

While the 40 times earnings multiple makes KOSÉ look expensive, our DCF model tells a contrasting story. According to that view, the shares trade about 38.7 percent below an estimated fair value of ¥8,547, which implies the market could be underpricing the company’s long term cash flows.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out KOSÉ for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 907 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own KOSÉ Narrative

If you see the numbers differently or want to dig into the details yourself, you can build a personalized view in just a few minutes: Do it your way.

A great starting point for your KOSÉ research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Ready for more high conviction ideas?

Do not stop with one opportunity when the Screener can surface fresh, data driven ideas tailored to the themes and risk levels you actually care about.

- Capture potential price dislocations by targeting companies that appear inexpensive on cash flow metrics using these 907 undervalued stocks based on cash flows before the market closes the gap.

- Participate in structural trends in automation and predictive analytics by focusing on innovators at the intersection of medicine and algorithms with these 30 healthcare AI stocks.

- Explore the evolving landscape of digital finance by zeroing in on businesses building utility around blockchain and tokens through these 81 cryptocurrency and blockchain stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com