Why GlobalFoundries (GFS) Is Up 8.7% After New U.S. Security Role And Green Targets

- Recent developments underscored GlobalFoundries’ role as a core U.S. semiconductor manufacturer, with Department of Defense-trusted supplier status, substantial federal backing, and long-term government and industrial chip contracts embedded in critical aerospace, communications, and military programs.

- At the same time, GlobalFoundries is expanding a centralized abatement system in Singapore as part of its plan to cut greenhouse gas emissions by 42% from 2021 levels by 2030 and reach net zero by 2050, aligning long-term growth with national security and sustainability priorities.

- We’ll now examine how GlobalFoundries’ government-backed, secure manufacturing footprint could reshape its investment narrative for long-term-oriented investors.

AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

GlobalFoundries Investment Narrative Recap

To own GlobalFoundries, you need to believe in a future where secure, government-backed, specialty chip manufacturing remains essential, even without leading-edge nodes. The latest confirmation of its role as a trusted U.S. defense supplier and recipient of substantial federal backing reinforces the core long term catalyst of capacity expansion for defense, automotive, and communications customers. It does little, however, to reduce key risks around high capital intensity and exposure to pricing pressure in more commoditized mobile and IoT chips.

Among recent developments, the expansion of GlobalFoundries’ centralized abatement system in Singapore stands out, because it ties its manufacturing footprint to measurable emissions reduction targets. For investors focused on long term contracts and government support, this matters: large customers and public funding programs increasingly scrutinize supply chain emissions, so credible progress on greenhouse gas reduction may support future procurement decisions, even as competition from leading-edge foundries and in-house chipmaking remains a structural risk.

Yet investors should also understand how rising capital needs and pricing pressure could still weigh on GlobalFoundries’ margins and cash generation...

Read the full narrative on GlobalFoundries (it's free!)

GlobalFoundries' narrative projects $8.6 billion revenue and $1.4 billion earnings by 2028. This requires 8.0% yearly revenue growth and about a $1.5 billion earnings increase from -$115.0 million today.

Uncover how GlobalFoundries' forecasts yield a $39.43 fair value, in line with its current price.

Exploring Other Perspectives

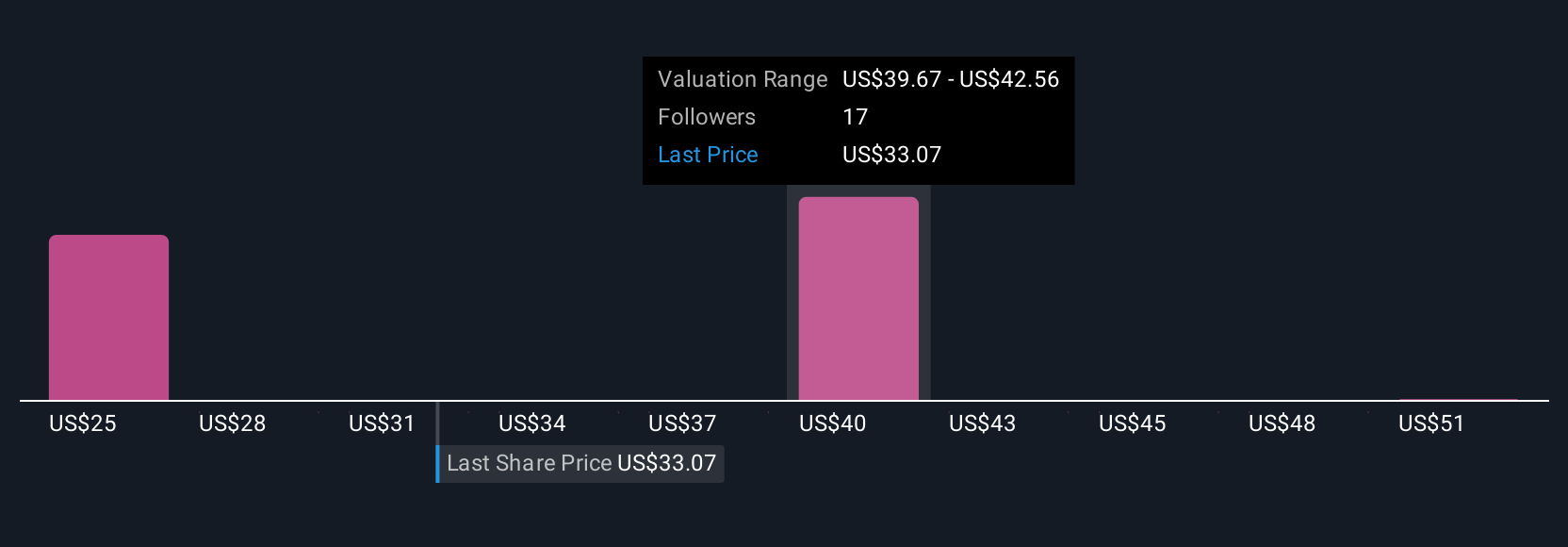

Four members of the Simply Wall St Community currently estimate GlobalFoundries’ fair value between US$30.16 and US$54.14, reflecting very different expectations. When you set those views against the company’s heavy capital expenditure needs and dependence on sustained demand in automotive and communications chips, it underlines why many investors compare several perspectives before forming a view.

Explore 4 other fair value estimates on GlobalFoundries - why the stock might be worth 23% less than the current price!

Build Your Own GlobalFoundries Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your GlobalFoundries research is our analysis highlighting 1 key reward that could impact your investment decision.

- Our free GlobalFoundries research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate GlobalFoundries' overall financial health at a glance.

Interested In Other Possibilities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 37 companies in the world exploring or producing it. Find the list for free.

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com