What Hormel Foods (HRL)'s 2026 Outlook and 60th Dividend Hike Means For Shareholders

- Hormel Foods recently reported fiscal 2025 results showing net sales of US$12.11 billion with net income of US$478.2 million, and issued fiscal 2026 guidance calling for US$12.2 billion–US$12.5 billion in net sales, GAAP EPS of US$1.29–US$1.39, and operating income of US$0.96 billion–US$1.03 billion.

- The company paired this outlook with a 1% dividend increase, marking its 60th straight annual raise, underscoring management’s confidence despite a pressured consumer backdrop and ongoing cost headwinds.

- We’ll now examine how Hormel’s 2026 guidance for higher earnings and continued dividend growth shapes the company’s broader investment narrative.

We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Hormel Foods Investment Narrative Recap

To own Hormel, you need to believe its branded protein and snacks portfolio can steadily convert modest volume and pricing gains into healthier margins, while the dividend record adds appeal. The key near term catalyst is management’s effort to rebuild profitability after a year of compressed margins, with the biggest risk still coming from volatile input costs that could blunt the impact of 2026’s targeted earnings recovery; this latest guidance does not fundamentally change that risk profile.

The most relevant development here is the new fiscal 2026 outlook calling for US$12.2 billion to US$12.5 billion in sales and GAAP EPS of US$1.29 to US$1.39, after fiscal 2025 EPS of US$0.87. For investors watching catalysts, this guidance sets a clear profitability bar at a time when management is still contending with commodity inflation and softer demand in parts of foodservice and international, making execution against that earnings range especially important.

Yet behind the reassuring 60 year dividend streak, investors should be aware of the pressure that persistent and volatile commodity inflation could still place on margins and cash flows...

Read the full narrative on Hormel Foods (it's free!)

Hormel Foods' narrative projects $13.0 billion revenue and $952.2 million earnings by 2028. This requires 2.5% yearly revenue growth and about a $197.7 million earnings increase from $754.5 million today.

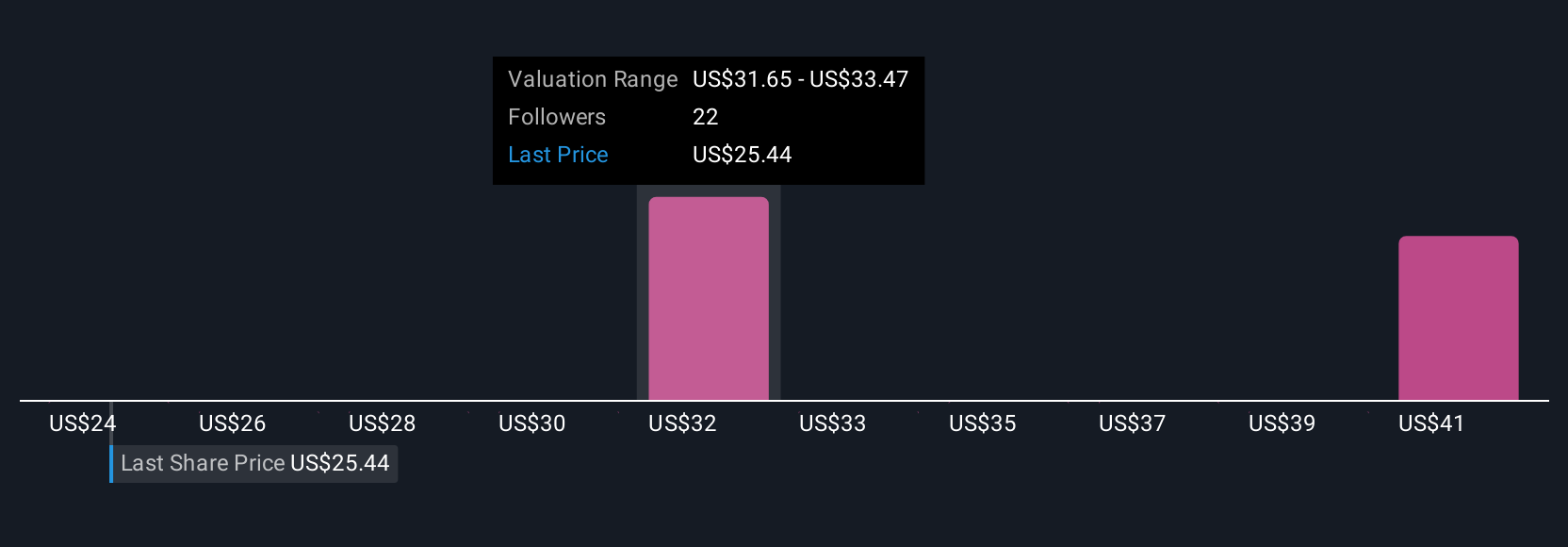

Uncover how Hormel Foods' forecasts yield a $26.69 fair value, a 10% upside to its current price.

Exploring Other Perspectives

Five members of the Simply Wall St Community currently see Hormel’s fair value between US$24.36 and about US$47.20, a wide spread of individual expectations. Against that backdrop, the company’s own 2026 earnings guidance brings the ongoing risk of commodity cost volatility into sharper focus for anyone assessing how resilient Hormel’s profit recovery could be.

Explore 5 other fair value estimates on Hormel Foods - why the stock might be worth as much as 94% more than the current price!

Build Your Own Hormel Foods Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Hormel Foods research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Hormel Foods research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Hormel Foods' overall financial health at a glance.

No Opportunity In Hormel Foods?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com