Powell Industries (POWL) Is Up 7.1% After Backlog-Fueled Utility And Data Center Demand Shift - Has The Bull Case Changed?

- Earlier in fiscal 2025, Powell Industries reported that diversification beyond its core oil, gas and petrochemical markets helped drive higher revenues in electric utility and light rail traction power, supported by rising electrical power needs from data centers.

- The company also highlighted a very large US$1.40 billion backlog and US$1.20 billion of new orders, underscoring how its broadened customer base across utilities, transport and other industrial markets is underpinning forward revenue visibility.

- We will now examine how this backlog-supported expansion into electric utility and data center-related demand may reshape Powell Industries’ investment narrative.

These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Powell Industries Investment Narrative Recap

To own Powell Industries, you need to believe it can turn its record US$1.40 billion backlog and growing presence in utilities and data center power into durable earnings, even as consensus now points to modest revenue growth and a forecast earnings decline. The latest backlog update supports the near term revenue catalyst by extending visibility, but it does not remove the key risk that recent profit momentum may slow if new orders, mix or pricing soften.

The most relevant recent update is Powell’s fiscal 2025 result, which showed higher full year sales of US$1,104.32 million and net income of US$180.75 million alongside that large backlog and US$1.20 billion of new orders. Together with stronger contributions from electric utility and light rail traction power tied to data center demand, these results link the order book directly to near term earnings, while also sharpening the question of how sustainable this level of profitability will be.

Yet investors should be aware that, despite the strong backlog, analysts currently expect Powell’s earnings to decline over the next few years...

Read the full narrative on Powell Industries (it's free!)

Powell Industries' narrative projects $1.3 billion revenue and $169.4 million earnings by 2028. This implies 5.7% yearly revenue growth and a $6.0 million earnings decrease from $175.4 million today.

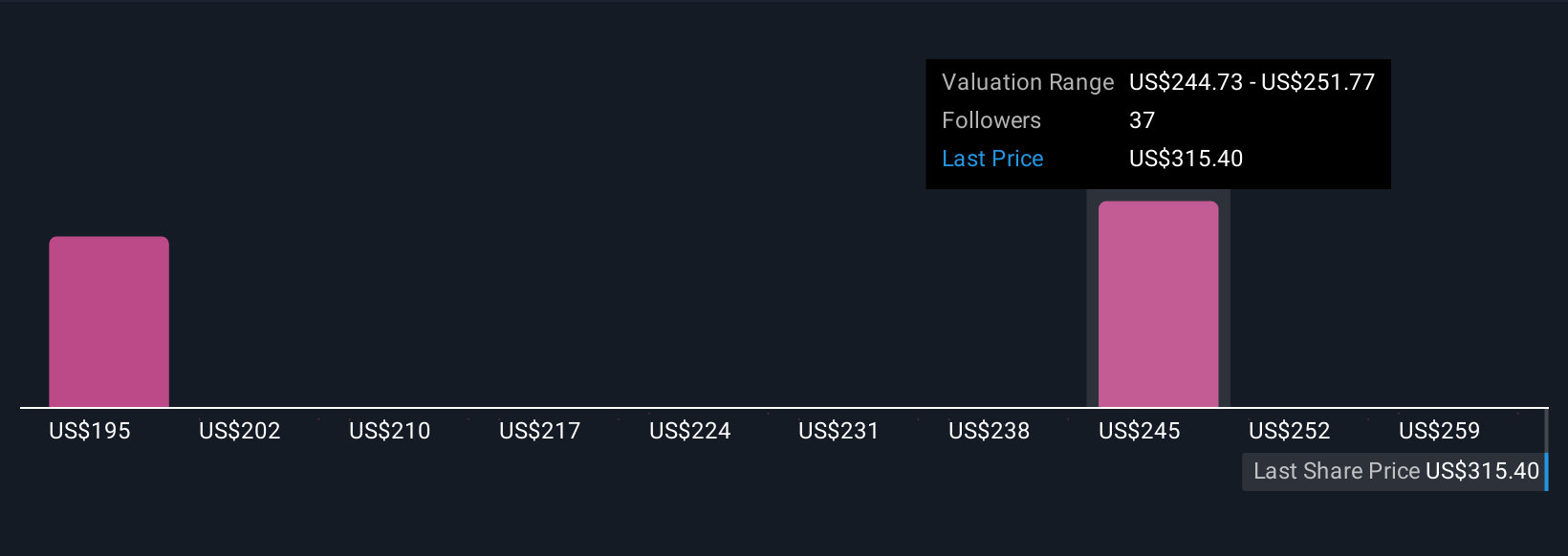

Uncover how Powell Industries' forecasts yield a $269.26 fair value, a 21% downside to its current price.

Exploring Other Perspectives

Four members of the Simply Wall St Community value Powell Industries between US$201.78 and US$269.26 per share, highlighting how far individual views can spread. Set this against the consensus expectation of declining earnings despite a large backlog and you can weigh how different scenarios might affect Powell’s ability to convert orders into long term profit growth.

Explore 4 other fair value estimates on Powell Industries - why the stock might be worth 41% less than the current price!

Build Your Own Powell Industries Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Powell Industries research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Powell Industries research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Powell Industries' overall financial health at a glance.

Searching For A Fresh Perspective?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 37 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com