How Record Output And A Higher Dividend At Suncor Energy (TSX:SU) Has Changed Its Investment Story

- Suncor Energy recently reported past third-quarter 2025 results that exceeded expectations, supported by record upstream production, higher refinery throughput guidance, and a 5% increase in its quarterly dividend to C$0.60 per share, while returning C$1.40 billion to shareholders through buybacks and dividends.

- This combination of stronger operations, upgraded 2025 production and refining guidance, and increased cash returns highlights management’s confidence in the company’s cash-generating capacity and capital allocation framework.

- We’ll now examine how Suncor’s upgraded production guidance and increased dividend influence the existing investment narrative for the company.

Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

Suncor Energy Investment Narrative Recap

Suncor still appeals most to investors who believe its integrated oil sands and refining model can keep generating solid cash flows despite a challenging long term carbon and demand backdrop. The Q3 2025 beat and upgraded 2025 guidance strengthen the near term catalyst of higher volumes and margins, but they do not materially reduce the structural risks from emissions policy and the global energy transition.

The 5% dividend increase to C$0.60 per share, combined with C$1.40 billion in quarterly buybacks and dividends, ties the latest results directly to the existing catalyst of growing cash returns. For investors focused on capital discipline and income, this reinforces the current narrative that Suncor is prioritizing returning excess cash while its operations run near record levels.

But despite these positives, investors should still be aware of how rising carbon costs and tighter emissions rules could...

Read the full narrative on Suncor Energy (it's free!)

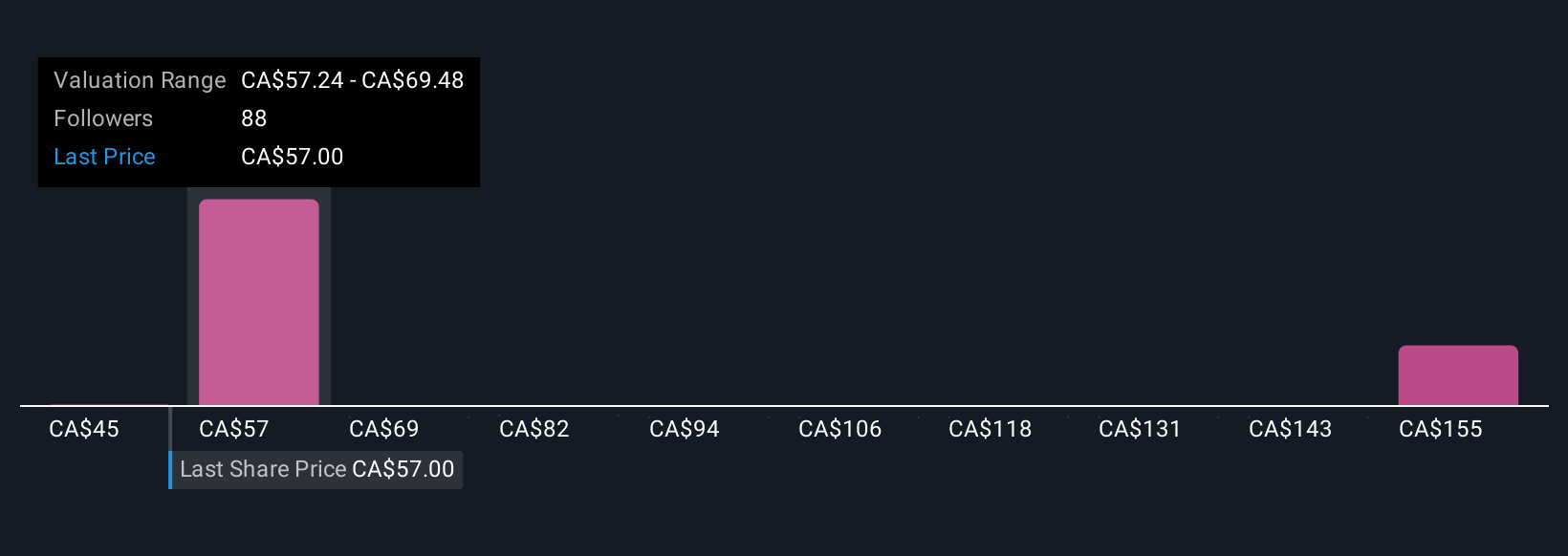

Suncor Energy’s narrative projects CA$48.1 billion in revenue and CA$5.0 billion in earnings by 2028. This implies a 1.1% yearly revenue decline and an earnings decrease of CA$0.7 billion from CA$5.7 billion today.

Uncover how Suncor Energy's forecasts yield a CA$65.55 fair value, a 7% upside to its current price.

Exploring Other Perspectives

Twelve members of the Simply Wall St Community currently see Suncor’s fair value anywhere between C$52.72 and C$183.09, underscoring how far opinions can diverge. Set this wide range against the recent production and refining guidance upgrades, and you have several distinct stories about how durable Suncor’s cash generating profile might really be, which are worth comparing in more detail.

Explore 12 other fair value estimates on Suncor Energy - why the stock might be worth 14% less than the current price!

Build Your Own Suncor Energy Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Suncor Energy research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Suncor Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Suncor Energy's overall financial health at a glance.

No Opportunity In Suncor Energy?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com