Is Gold Royalty (GROY) Quietly Redefining Its Deal-Making Strategy With New Equity And Credit Moves?

- Gold Royalty Corp. recently filed a follow-on equity offering of its common shares and restructured its $70 million deal’s underwriting group, while previously expanding and extending a revolving credit facility to US$75 million with an accordion feature up to an additional US$25 million.

- Together, the equity raise and larger, longer-dated credit facility point to a company focused on bolstering liquidity to fund future acquisitions and investments in its royalty portfolio.

- Next, we’ll consider how the expanded US$75 million revolving credit facility could reshape Gold Royalty’s existing investment narrative.

These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Gold Royalty Investment Narrative Recap

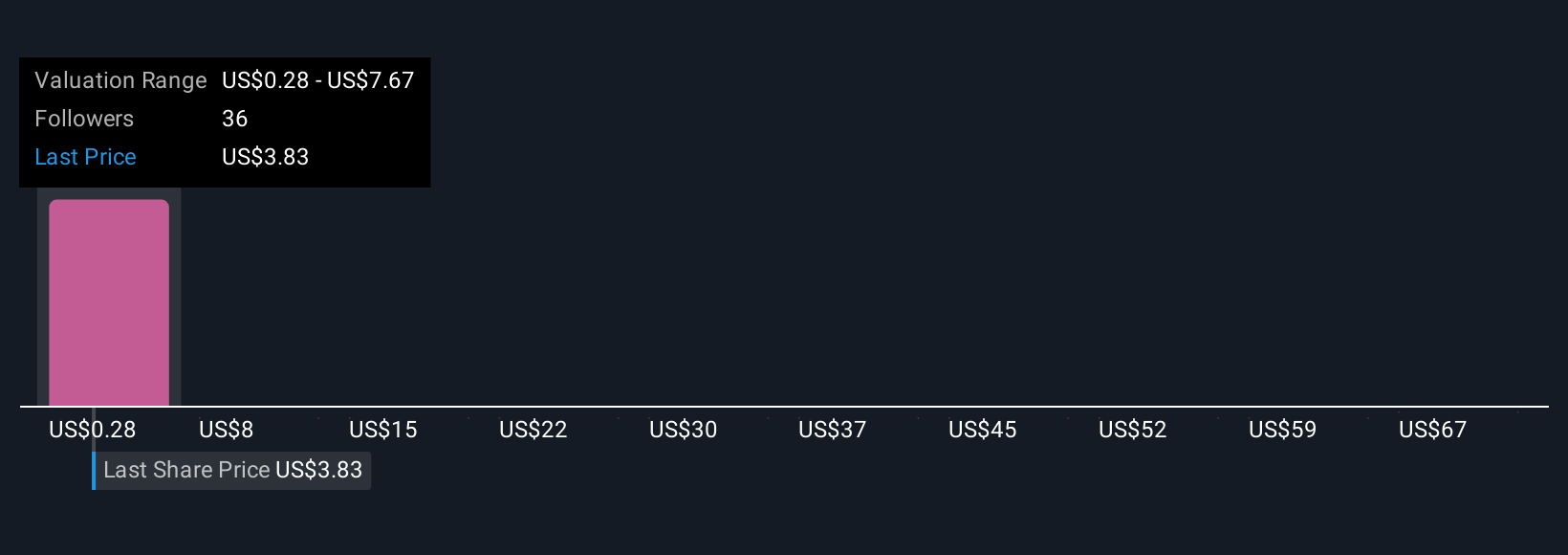

To own Gold Royalty, you need to believe its growing royalty portfolio can eventually translate rising gold-linked revenue into sustainable profits, despite current losses and a high sales multiple. The fresh follow-on equity filing and upsized US$75 million revolving facility mostly reinforce near term funding flexibility, but they do not remove the key short term tension between funding new deals and the ongoing risk of shareholder dilution.

The expanded revolving credit facility, now at US$75 million with an accordion feature up to an additional US$25 million, is especially relevant here because it gives Gold Royalty more non equity firepower to pursue acquisitions that could support its production ramp catalysts at Côté, Vareš and Borborema, while also testing how much balance sheet leverage investors are comfortable with.

Yet while funding capacity has improved, investors should be aware that continued reliance on equity issuance and in the money warrants could still...

Read the full narrative on Gold Royalty (it's free!)

Gold Royalty's narrative projects $46.6 million revenue and $14.7 million earnings by 2028.

Uncover how Gold Royalty's forecasts yield a $4.79 fair value, a 24% upside to its current price.

Exploring Other Perspectives

Three members of the Simply Wall St Community currently see fair value for Gold Royalty between US$4.79 and US$9.00 per share, underscoring how far opinions can spread. You might weigh that dispersion against the company’s reliance on a handful of ramping assets and decide how comfortable you are with the concentration risk it brings for future returns.

Explore 3 other fair value estimates on Gold Royalty - why the stock might be worth over 2x more than the current price!

Build Your Own Gold Royalty Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Gold Royalty research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Gold Royalty research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Gold Royalty's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our top stock finds are flying under the radar-for now. Get in early:

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Rare earth metals are the new gold rush. Find out which 36 stocks are leading the charge.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com