Islamic Arab Insurance Co. (Salama) PJSC (DFM:SALAMA) Looks Inexpensive After Falling 47% But Perhaps Not Attractive Enough

Islamic Arab Insurance Co. (Salama) PJSC (DFM:SALAMA) shareholders that were waiting for something to happen have been dealt a blow with a 47% share price drop in the last month. The recent drop completes a disastrous twelve months for shareholders, who are sitting on a 51% loss during that time.

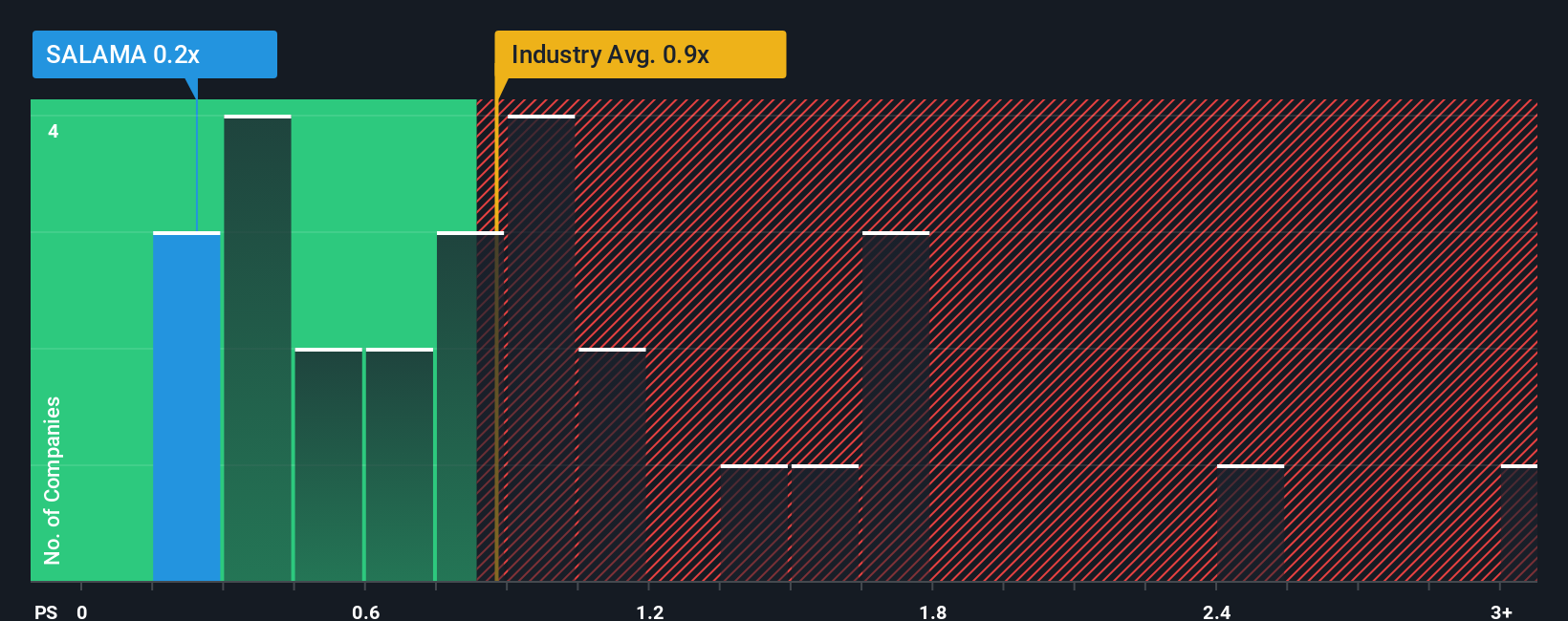

Even after such a large drop in price, considering around half the companies operating in the United Arab Emirates' Insurance industry have price-to-sales ratios (or "P/S") above 0.9x, you may still consider Islamic Arab Insurance (Salama) PJSC as an solid investment opportunity with its 0.2x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's limited.

Check out our latest analysis for Islamic Arab Insurance (Salama) PJSC

What Does Islamic Arab Insurance (Salama) PJSC's Recent Performance Look Like?

As an illustration, revenue has deteriorated at Islamic Arab Insurance (Salama) PJSC over the last year, which is not ideal at all. One possibility is that the P/S is low because investors think the company won't do enough to avoid underperforming the broader industry in the near future. Those who are bullish on Islamic Arab Insurance (Salama) PJSC will be hoping that this isn't the case so that they can pick up the stock at a lower valuation.

Although there are no analyst estimates available for Islamic Arab Insurance (Salama) PJSC, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Do Revenue Forecasts Match The Low P/S Ratio?

In order to justify its P/S ratio, Islamic Arab Insurance (Salama) PJSC would need to produce sluggish growth that's trailing the industry.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 29%. The last three years don't look nice either as the company has shrunk revenue by 4.5% in aggregate. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Comparing that to the industry, which is predicted to deliver 4.6% growth in the next 12 months, the company's downward momentum based on recent medium-term revenue results is a sobering picture.

In light of this, it's understandable that Islamic Arab Insurance (Salama) PJSC's P/S would sit below the majority of other companies. However, we think shrinking revenues are unlikely to lead to a stable P/S over the longer term, which could set up shareholders for future disappointment. Even just maintaining these prices could be difficult to achieve as recent revenue trends are already weighing down the shares.

The Final Word

Islamic Arab Insurance (Salama) PJSC's recently weak share price has pulled its P/S back below other Insurance companies. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of Islamic Arab Insurance (Salama) PJSC revealed its shrinking revenue over the medium-term is contributing to its low P/S, given the industry is set to grow. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. Given the current circumstances, it seems unlikely that the share price will experience any significant movement in either direction in the near future if recent medium-term revenue trends persist.

Before you take the next step, you should know about the 3 warning signs for Islamic Arab Insurance (Salama) PJSC (2 make us uncomfortable!) that we have uncovered.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.