Assessing FIT Hon Teng (SEHK:6088)’s Valuation After Earnings Momentum and Circular Dispatch Delay

FIT Hon Teng (SEHK:6088) is juggling two storylines right now: a solid upswing in net income and a delay in sending out a circular on key framework agreements, and investors seem more focused on the earnings momentum.

See our latest analysis for FIT Hon Teng.

With the share price now at HK$5.28 and a strong 90 day share price return of 36.08 percent, investors seem to be rewarding the earnings story. This is reflected in a 52.16 percent one year total shareholder return and an impressive 161.39 percent three year total shareholder return that suggest positive momentum is still building.

If this kind of turnaround has your attention, it could be a good moment to compare FIT Hon Teng with other hardware focused tech names using high growth tech and AI stocks.

Yet with the stock now trading close to analyst targets but still showing a sizeable intrinsic discount estimate, the real question is whether today’s price offers upside or if the market already anticipates further growth.

Price-to-Earnings of 31.5x: Is it justified?

On a price-to-earnings basis, FIT Hon Teng looks richly valued at the last close of HK$5.28 compared to both peers and its own fair ratio signal.

The price to earnings multiple compares what investors are paying today for each unit of current earnings, a core yardstick for established hardware and electronics makers. For FIT Hon Teng, a 31.5x P/E suggests the market is paying a premium for expected growth and the recent turnaround narrative.

That premium is steep when set against benchmarks. The Hong Kong Electronic industry sits around 12x, and the peer average near 19.2x, so FIT Hon Teng trades at a far higher earnings multiple than comparable names. Even against the estimated fair price to earnings ratio of 26.5x, the current 31.5x looks stretched, implying the multiple could have room to compress if sentiment cools or growth underdelivers.

Explore the SWS fair ratio for FIT Hon Teng

Result: Price-to-Earnings of 31.5x (OVERVALUED)

However, risks remain, including potential earnings disappointment relative to lofty expectations, and a rerating if analysts trim targets or momentum investors rotate away.

Find out about the key risks to this FIT Hon Teng narrative.

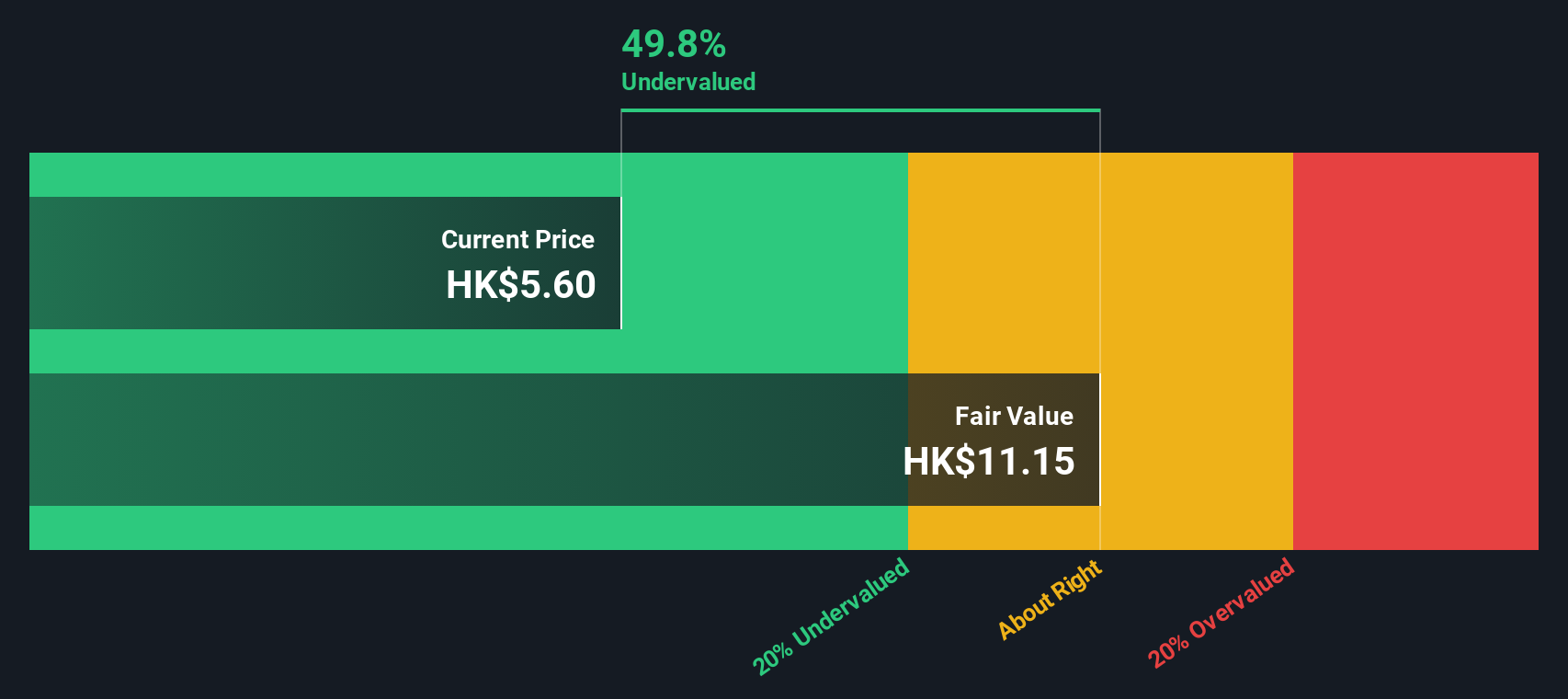

Another View: DCF Points the Other Way

While the current 31.5x earnings multiple looks stretched, our DCF model paints a very different picture, suggesting fair value near HK$11.04, around 52 percent above today’s HK$5.28 share price. If the cash flows are right, this may indicate that the market is underestimating the story.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out FIT Hon Teng for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 902 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own FIT Hon Teng Narrative

If you see the numbers differently or would rather dig into the details yourself, you can build a personalised view in just a few minutes: Do it your way.

A great starting point for your FIT Hon Teng research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Ready for your next investing move?

Do not stop at a single stock when an entire universe of opportunities is within reach. Step up your game now using these focused idea generators.

- Target reliable income streams by scanning these 15 dividend stocks with yields > 3% that could bolster your portfolio with consistent cash returns.

- Position yourself early in structural growth by reviewing these 27 AI penny stocks shaping the next wave of intelligent technology.

- Strengthen your margin of safety by evaluating these 902 undervalued stocks based on cash flows that may be trading below their intrinsic worth today.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com