Is Kwang Jin Ind (KOSDAQ:026910) Using Debt In A Risky Way?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Kwang Jin Ind. Co., Ltd. (KOSDAQ:026910) does carry debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

What Is Kwang Jin Ind's Debt?

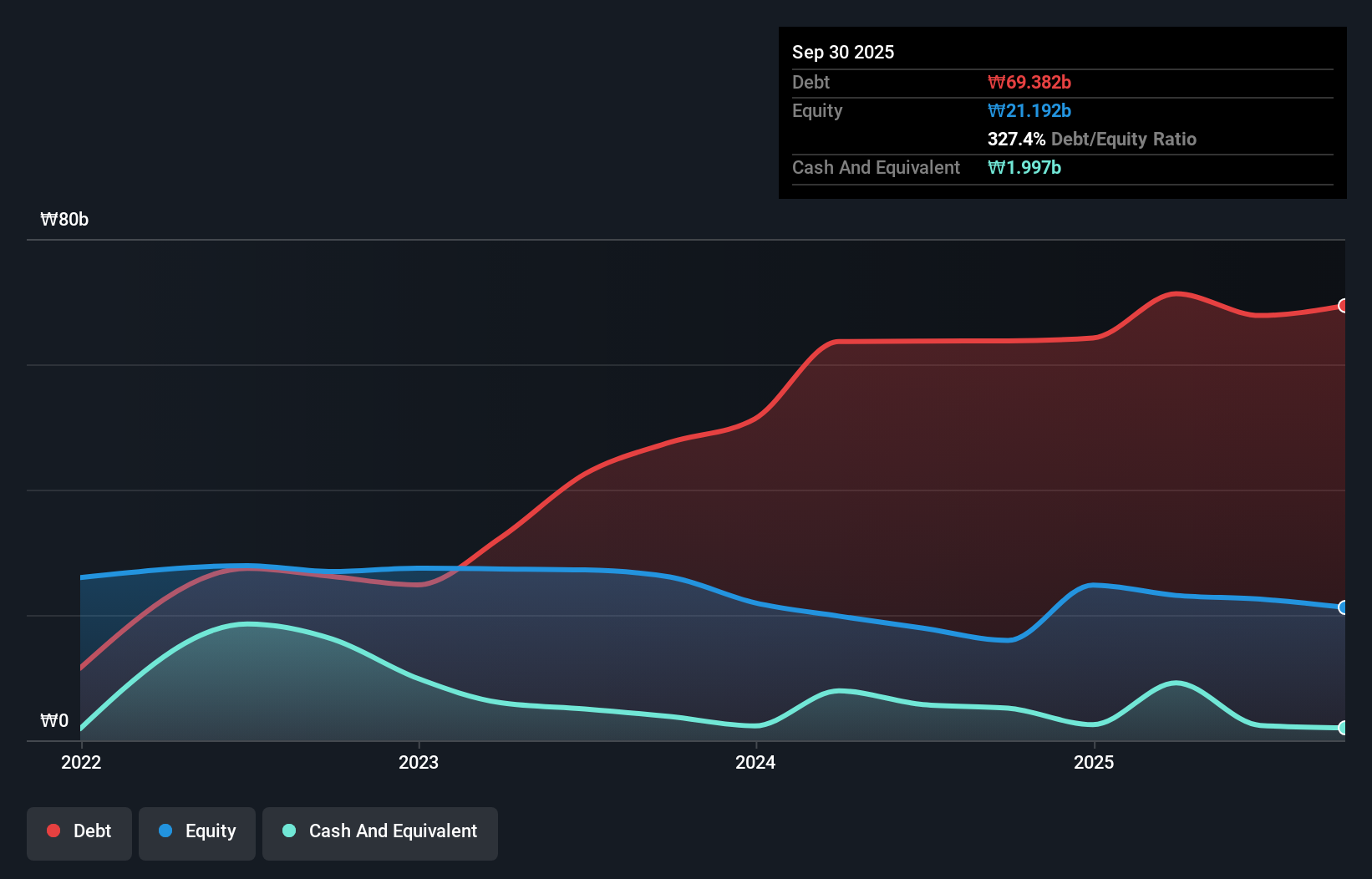

The image below, which you can click on for greater detail, shows that at September 2025 Kwang Jin Ind had debt of ₩69.4b, up from ₩63.7b in one year. On the flip side, it has ₩2.00b in cash leading to net debt of about ₩67.4b.

How Healthy Is Kwang Jin Ind's Balance Sheet?

We can see from the most recent balance sheet that Kwang Jin Ind had liabilities of ₩44.5b falling due within a year, and liabilities of ₩29.3b due beyond that. Offsetting these obligations, it had cash of ₩2.00b as well as receivables valued at ₩6.84b due within 12 months. So it has liabilities totalling ₩64.9b more than its cash and near-term receivables, combined.

This deficit casts a shadow over the ₩17.8b company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. At the end of the day, Kwang Jin Ind would probably need a major re-capitalization if its creditors were to demand repayment. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Kwang Jin Ind's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Check out our latest analysis for Kwang Jin Ind

Over 12 months, Kwang Jin Ind reported revenue of ₩58b, which is a gain of 7.6%, although it did not report any earnings before interest and tax. We usually like to see faster growth from unprofitable companies, but each to their own.

Caveat Emptor

Over the last twelve months Kwang Jin Ind produced an earnings before interest and tax (EBIT) loss. Its EBIT loss was a whopping ₩4.6b. If you consider the significant liabilities mentioned above, we are extremely wary of this investment. Of course, it may be able to improve its situation with a bit of luck and good execution. Nevertheless, we would not bet on it given that it vaporized ₩5.4b in cash over the last twelve months, and it doesn't have much by way of liquid assets. So we consider this a high risk stock and we wouldn't be at all surprised if the company asks shareholders for money before long. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. To that end, you should learn about the 2 warning signs we've spotted with Kwang Jin Ind (including 1 which is a bit concerning) .

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.