Is OneStream’s 41.6% Slide in 2025 Creating a Long Term Opportunity?

- If you are wondering whether OneStream at $18.38 is a bargain or a value trap, you are not alone. This breakdown is intended to help you evaluate it with more confidence.

- The stock is down 0.9% over the last week, 22.6% over the past month, and 35.0% year to date, extending a tough 41.6% slide over the past year that has reset expectations and risk perceptions.

- Recently, investors have been digesting a wave of commentary around high growth software names, with shifting sentiment on how much they should pay for future cash flows versus current profitability. At the same time, sector wide debates about interest rates and risk appetite have put added pressure on richly valued tech stocks, which helps explain OneStream's sharp pullback.

- Despite that backdrop, OneStream scores a 4 out of 6 on our valuation checks, suggesting it appears undervalued on several key measures. Below, we unpack those approaches, followed by a broader way to think about valuation that ties them together by the end of this article.

Find out why OneStream's -41.6% return over the last year is lagging behind its peers.

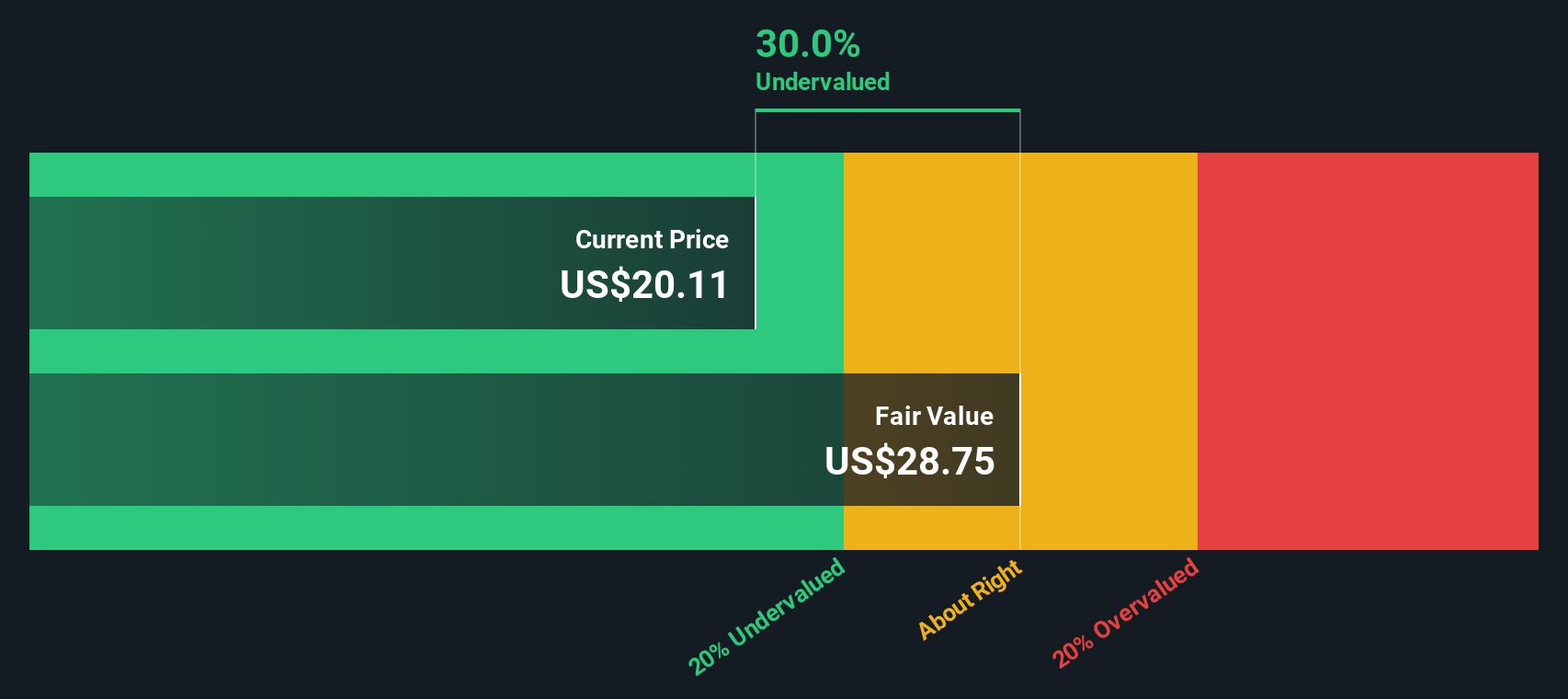

Approach 1: OneStream Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth by projecting its future cash flows and then discounting them back to today in dollar terms. For OneStream, the model starts from last twelve months free cash flow of about $93.2 Million and uses analyst forecasts for the next few years, then extends those trends further out using a 2 Stage Free Cash Flow to Equity approach.

Analysts and extrapolated estimates see free cash flow rising to around $563.6 Million by 2035, with intermediate steps such as $120.3 Million in 2026 and $305.1 Million in 2029, all adjusted back to today to reflect risk and the time value of money. Adding up these discounted cash flows produces an intrinsic value estimate of roughly $29.18 per share.

Against the current share price of $18.38, this implies the stock trades at about a 37.0% discount to the DCF based fair value, suggesting meaningful upside if the cash flow path plays out as expected.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests OneStream is undervalued by 37.0%. Track this in your watchlist or portfolio, or discover 899 more undervalued stocks based on cash flows.

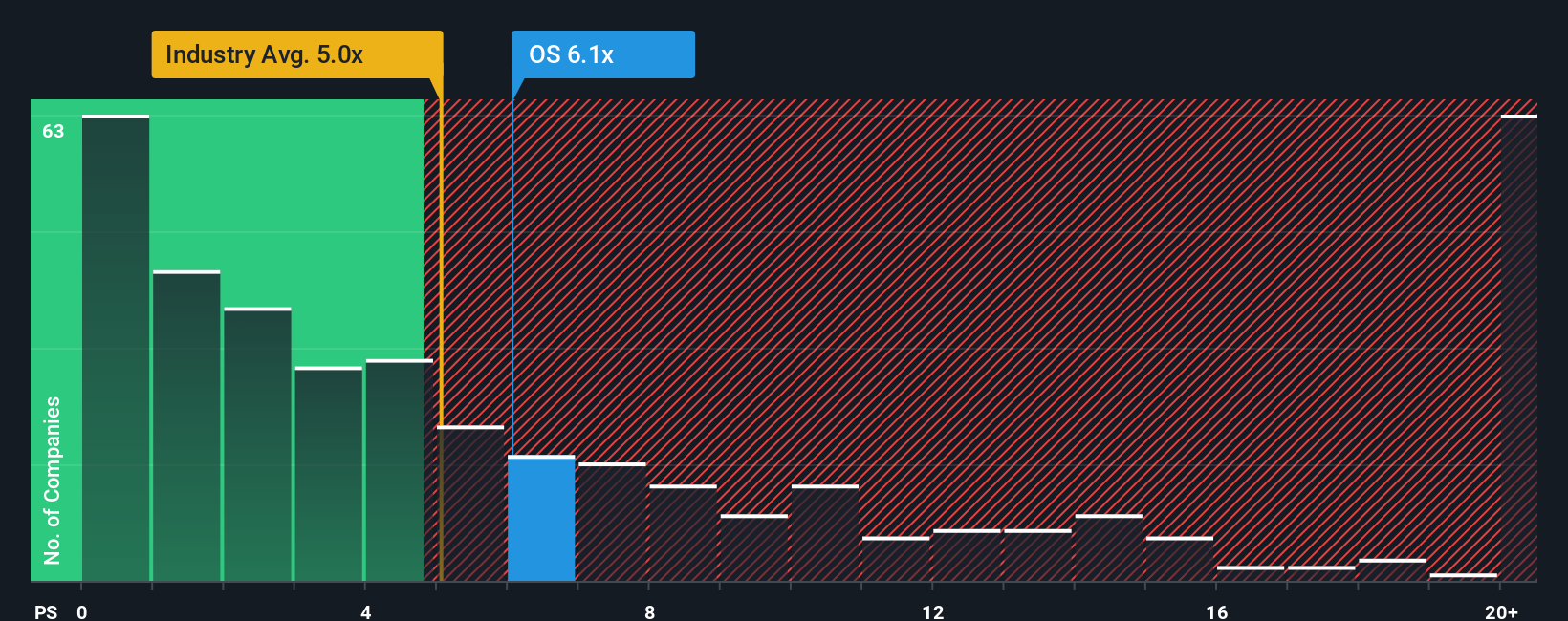

Approach 2: OneStream Price vs Sales

For software names that are still prioritizing growth over bottom line profits, the price to sales ratio is often the cleanest way to compare valuation, because revenue is less volatile and less affected by accounting choices than earnings.

In general, higher growth and lower perceived risk justify a higher sales multiple, while slower growth or higher uncertainty usually call for a lower one. OneStream currently trades on a price to sales ratio of about 6.06x. That is slightly above the broader Software industry average of roughly 4.95x and just below the peer group average of around 6.42x. This suggests the market is already paying up a bit for its growth profile.

Simply Wall St’s Fair Ratio framework goes a step further by estimating what multiple a stock should trade on after accounting for factors like expected growth, profitability, risk profile, industry dynamics and market cap. For OneStream, this Fair Ratio sits at about 5.40x, which is below today’s 6.06x market multiple. On that basis, the shares look somewhat expensive relative to what its fundamentals would typically warrant.

Result: OVERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1450 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your OneStream Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which are simply your story about a company, tied directly to your assumptions for its future revenue, earnings, margins and fair value. A Narrative connects what you believe about the business, for example how fast OneStream can grow, how durable its AI advantages are, or how intense competition might become, to a specific financial forecast and then to a clear fair value estimate. On Simply Wall St’s Community page, used by millions of investors, Narratives are an easy tool that show whether your Fair Value is above or below today’s Price, helping you decide how OneStream compares to your own expectations. They also update dynamically as new information like earnings, guidance, or AI partnership news comes in, so your view stays current without you rebuilding a model from scratch. For example, one Narrative on OneStream might see the Microsoft AI alliance as supporting sustained 20 percent plus growth and justify a fair value near 38 dollars, while a more cautious Narrative focused on competitive and public sector risks might land closer to 23 dollars, yet both are expressed through the same simple framework.

Do you think there's more to the story for OneStream? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com