Essential Properties Realty Trust: Assessing Valuation After Its Latest Dividend Increase for Q4 2025

Essential Properties Realty Trust (EPRT) just gave income investors something new to chew on by lifting its quarterly dividend for the fourth quarter of 2025, a move that signals confidence in both cash flows and the pipeline.

See our latest analysis for Essential Properties Realty Trust.

The higher payout comes on the heels of a fresh $400 million at the market equity program, and while the share price is only modestly higher year to date, the three year total shareholder return above 50% shows momentum has been building over the longer haul.

If this kind of steady REIT story has you thinking about what else is out there, it could be a good moment to explore fast growing stocks with high insider ownership.

With revenue and net income still climbing at double digit rates and the share price sitting at a notable discount to analyst targets, the key question now is whether EPRT is genuinely undervalued or if the market is simply pricing in years of future growth.

Most Popular Narrative Narrative: 13.4% Undervalued

With Essential Properties Realty Trust last closing at $31.08 against a narrative fair value near $35.89, the story leans toward upside, backed by ambitious growth assumptions and a rich earnings multiple.

The analysts have a consensus price target of $35.889 for Essential Properties Realty Trust based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $40.0, and the most bearish reporting a price target of just $33.0.

Want to see how double digit revenue growth, shifting profit margins and a higher future earnings multiple all fit together, and why this narrative still calls the stock undervalued?

Result: Fair Value of $35.89 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, rising competition in net lease deals, along with heavier exposure to car wash and restaurant tenants, could pressure yields and test rent resilience.

Find out about the key risks to this Essential Properties Realty Trust narrative.

Another Angle on Valuation

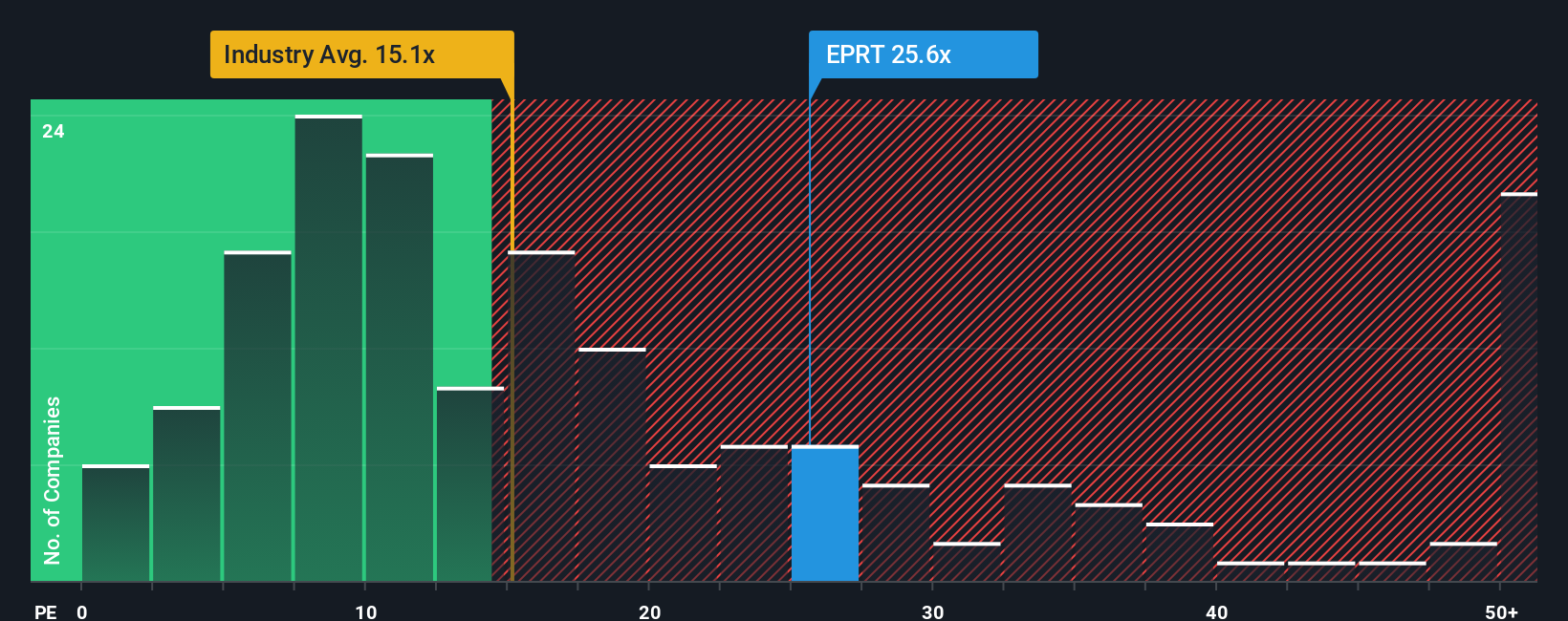

On earnings, the picture looks tighter. EPRT trades on a 25.7x price to earnings ratio, richer than the global REIT industry at 15.6x, but cheaper than peers at 32.5x and below a 33.8x fair ratio. This hints at upside, but also raises the question of how much optimism is already baked in.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Essential Properties Realty Trust Narrative

If this perspective does not quite match your view, or you prefer hands on research, you can build a custom take in minutes: Do it your way.

A great starting point for your Essential Properties Realty Trust research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you stop here, you could miss stocks setting up their next big move, so put Simply Wall Street's powerful screener to work for your watchlist today.

- Capture early stage growth potential by reviewing these 3592 penny stocks with strong financials that pair tiny share prices with surprisingly strong financial foundations.

- Strengthen your long term income stream by focusing on these 15 dividend stocks with yields > 3% that aim to balance yield with sustainability.

- Position yourself ahead of sentiment shifts by targeting these 896 undervalued stocks based on cash flows that markets may be overlooking right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com