What FirstCash Holdings (FCFS)'s Broad-Based Earnings Upside Means For Shareholders

- Earlier this week, FirstCash Holdings reported a very strong quarter, with accelerating revenue growth and higher earnings across its U.S. and Latin American pawn businesses, complemented by an incremental boost from its newly acquired H&T pawn stores in the U.K.

- The company also highlighted broad-based strength at American First Finance, where lower loss provisions and improved operating margins drove substantial earnings growth in its retail point-of-sale payment solutions segment.

- Next, we’ll examine how this broad-based earnings strength, particularly from American First Finance, shapes FirstCash Holdings’ investment narrative for investors.

Find companies with promising cash flow potential yet trading below their fair value.

What Is FirstCash Holdings' Investment Narrative?

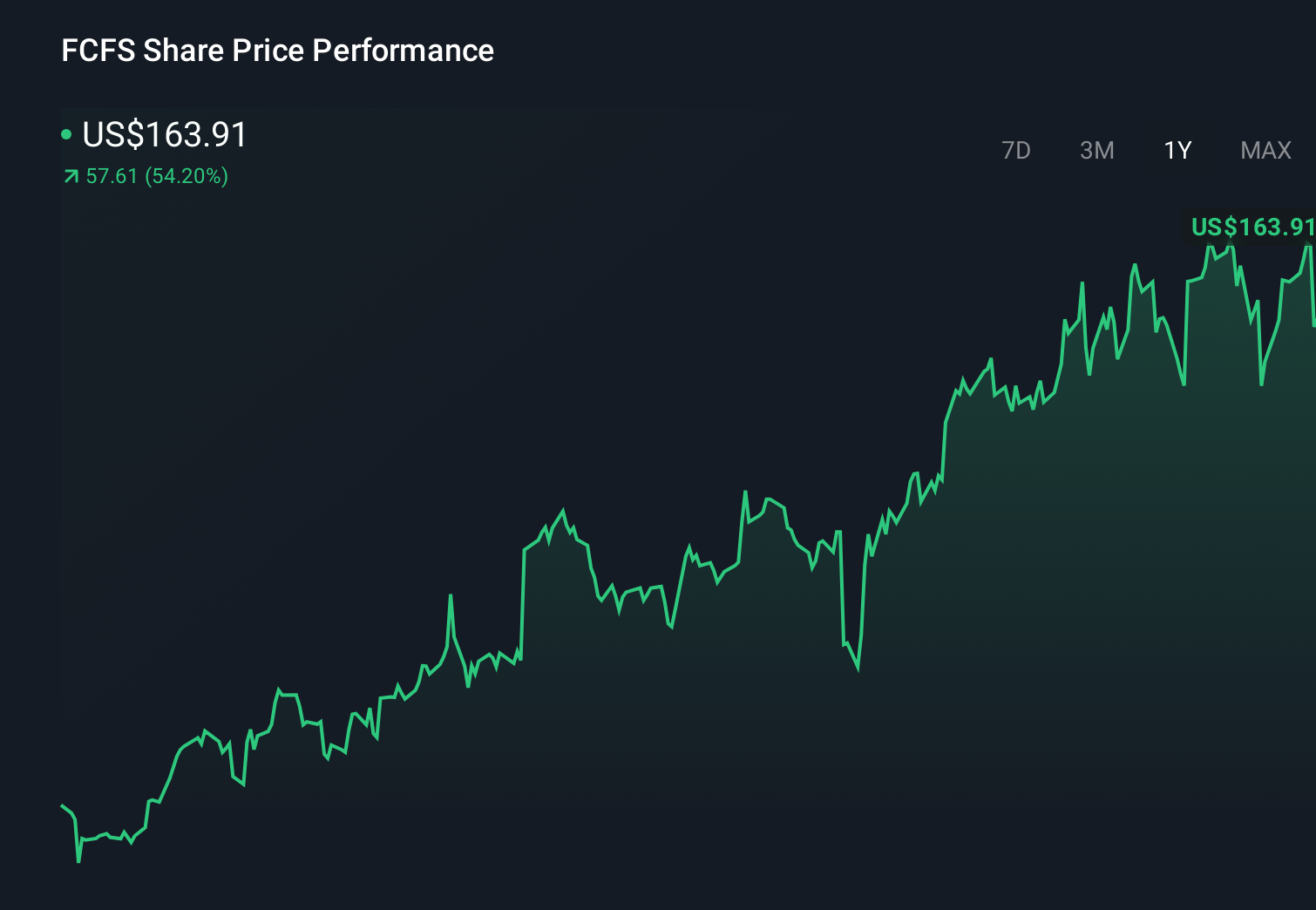

To own FirstCash, you have to believe its mix of traditional pawn lending and American First Finance’s point-of-sale products can keep compounding earnings without overreaching on risk or leverage. The latest quarter strengthens that case: broad-based growth across U.S., Latin American and now U.K. pawn stores, along with margin-driven earnings gains at American First Finance, supports the existing narrative of steady profit expansion rather than radically changing it. With the stock already up strongly year to date and trading at a higher earnings multiple than many consumer finance peers, the near term feels more about execution than discovery. Key catalysts now include integrating the H&T acquisition cleanly and sustaining lower loss provisions at American First Finance, while high debt and regulatory scrutiny remain the big watchpoints.

FirstCash Holdings' share price has been on the slide but might be dropping deeper into value territory. Find out whether it's a bargain at this price.Exploring Other Perspectives

Four Simply Wall St Community fair value views span roughly US$73 to US$182 per share, underlining how far apart private investors can be. Set against the recent earnings beat and reliance on American First Finance’s credit performance, that spread shows why it helps to weigh several opinions before deciding how resilient FirstCash’s story looks to you.

Explore 4 other fair value estimates on FirstCash Holdings - why the stock might be worth less than half the current price!

Build Your Own FirstCash Holdings Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your FirstCash Holdings research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free FirstCash Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate FirstCash Holdings' overall financial health at a glance.

Searching For A Fresh Perspective?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 36 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com