Moody’s (MCO) Valuation Check After New Pegasystems Partnership on Real-Time KYC and CLM Data Integration

Moody's (MCO) just tightened its grip on financial workflows, striking a strategic partnership with Pegasystems to feed its real time entity verification data directly into Pega’s AI driven CLM and KYC platform.

See our latest analysis for Moody's.

Despite the buzz around this Pegasystems deal, Moody’s share price has been treading water near $486, with a modest year to date share price gain and a far stronger three year total shareholder return suggesting longer term momentum remains intact even as shorter term sentiment cools.

If this kind of workflow and data story has your attention, it could be a good moment to explore fast growing stocks with high insider ownership for other potentially compelling setups.

With Moody’s still growing earnings at a healthy clip and trading about 11 percent below consensus targets, but after a powerful multiyear run, is this a fresh entry point or is the market already baking in the next leg of growth?

Most Popular Narrative Narrative: 10.8% Undervalued

With Moody's last closing at $486.37 against a most popular narrative fair value near the mid $540s, the story implies meaningful upside baked into steady execution.

The company's investment in advanced analytics, AI, and machine learning including 40% of Moody's Analytics products now featuring GenAI enablement and GenAI related spending growing at twice the rate of MA overall positions Moody's to capture a larger share of the data driven risk management market, resulting in higher recurring revenues and improved net margins through automation and operational efficiency.

Want to see how this automation push supposedly relates to durable growth and richer margins, while still justifying a premium earnings multiple, without any wild assumptions spelled out? Dive into the narrative and review the specific growth and profitability blueprint behind that fair value call.

Result: Fair Value of $545.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, evolving regulation around opaque private credit and fast moving AI competitors could still chip away at Moody’s pricing power and long term growth story.

Find out about the key risks to this Moody's narrative.

Another Lens on Valuation

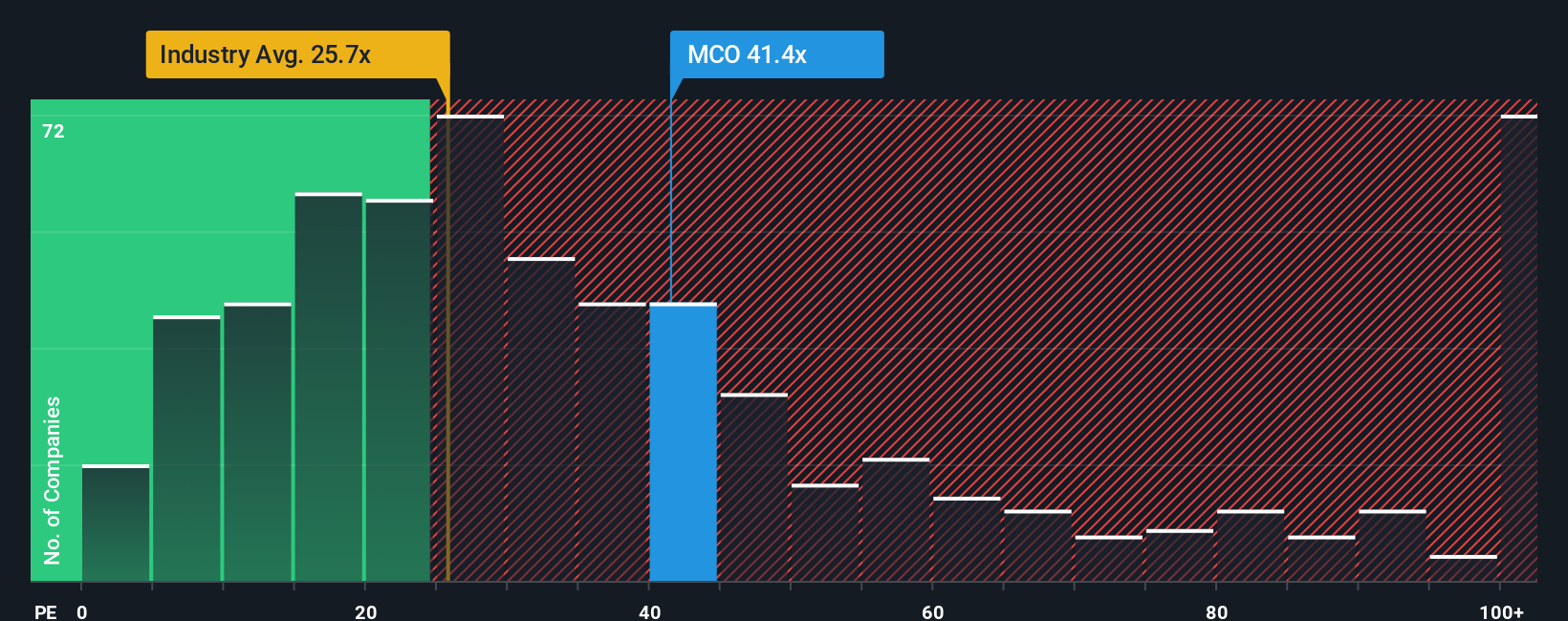

Step away from narratives and Moody's looks pricey. It trades on a P/E of 38.7 times versus 25 times for the US Capital Markets industry and 30.5 times for peers, while its fair ratio sits nearer 17.7 times. Is investors' optimism stretching valuation risk too far?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Moody's Narrative

If you see the story differently or want to stress test the numbers yourself, you can craft a personalized take in just a few minutes: Do it your way.

A great starting point for your Moody's research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Do not stop with just one opportunity. Use the Simply Wall St Screener now to uncover fresh, data driven ideas before everyone else rushes in.

- Capture potential mispricings early by running through these 894 undervalued stocks based on cash flows that may still be flying under the market’s radar.

- Explore innovation themes by targeting these 27 AI penny stocks shaping everything from automation to next generation software.

- Strengthen your income strategy by reviewing these 15 dividend stocks with yields > 3% that could support long term total returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com