Does UMB Financial’s Valuation Reflect Its Excess Returns Amid Regional Banking Uncertainty?

- If you are wondering whether UMB Financial is quietly trading at a discount or already priced for perfection, you are not alone. This stock has been drawing attention from investors hunting for value in regional banks.

- Despite some short-term noise, the share price is up 3.4% over the last month and 1.9% year to date, though it is still down 7.5% over the past year after a strong multiyear climb of 50.8% over three years and 79.4% over five years.

- Recent headlines around the regional banking space have focused on balance sheet resilience, deposit stability and how banks like UMB are positioning for a higher-for-longer interest rate backdrop. That backdrop has helped reset expectations, with investors reconsidering which banks have the diversified revenue and conservative underwriting to justify a higher valuation multiple.

- Right now, UMB Financial scores a 4 out of 6 on our undervaluation checks, which suggests there is some value on the table but also a few flags to unpack. In the sections ahead we will break down what different valuation approaches say about the stock, then finish with a more holistic way to think about UMB Financial's true worth.

Find out why UMB Financial's -7.5% return over the last year is lagging behind its peers.

Approach 1: UMB Financial Excess Returns Analysis

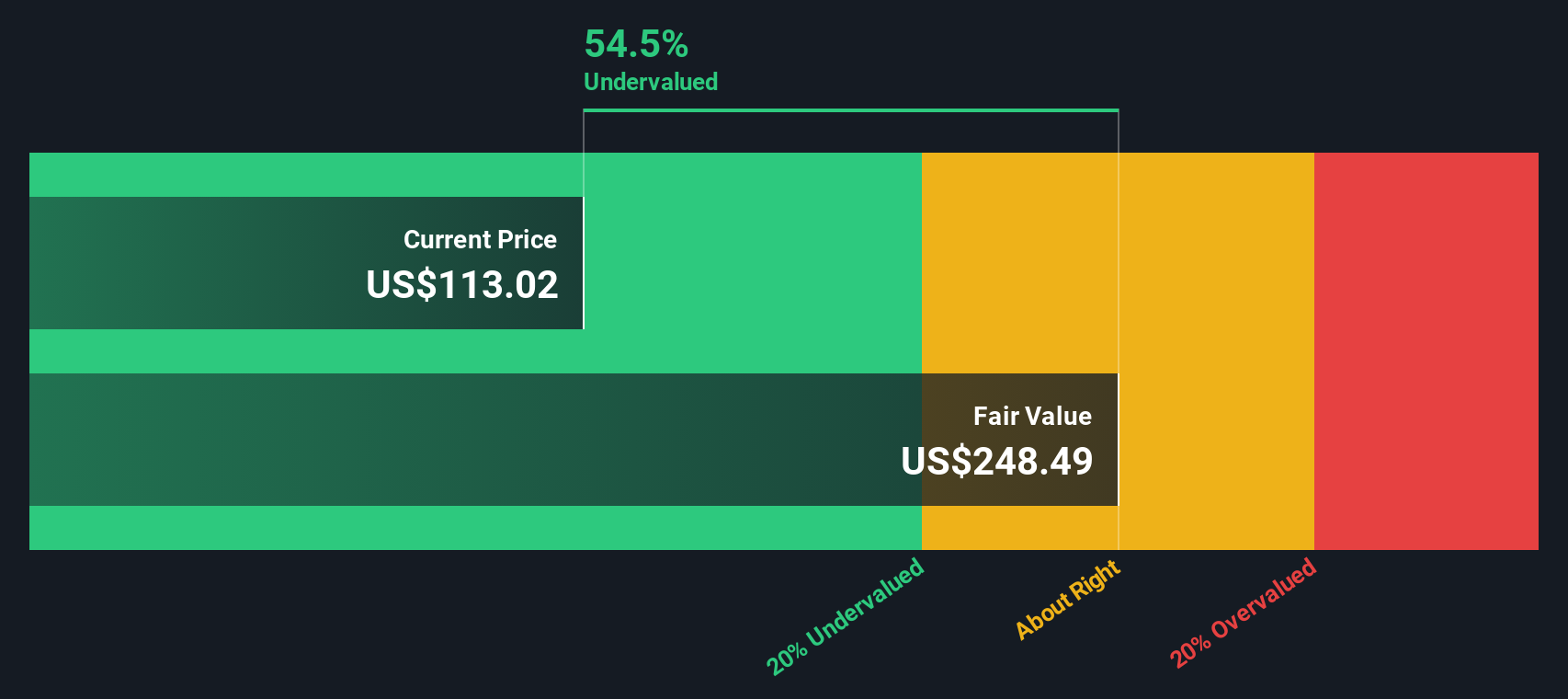

The Excess Returns model looks at how much profit UMB Financial can generate above the minimum return investors require on its equity, then capitalizes those extra profits into an intrinsic value per share.

For UMB Financial, the starting point is a Book Value of $94.13 per share and a Stable EPS of $12.10 per share, based on weighted future Return on Equity estimates from 8 analysts. With an Average Return on Equity of 11.30%, the bank is expected to earn more on its equity base than the Cost of Equity, which is estimated at $7.45 per share.

The difference between what the bank is expected to earn and what investors demand, the Excess Return, is $4.65 per share. Using a Stable Book Value of $107.08 per share, sourced from 9 analysts, and capitalizing these excess returns, the model arrives at an intrinsic value of about $232.81 per share.

Compared with the current share price, this Excess Returns valuation suggests the stock is roughly 51.1% undervalued, assuming these profitability levels are sustained.

Result: UNDERVALUED

Our Excess Returns analysis suggests UMB Financial is undervalued by 51.1%. Track this in your watchlist or portfolio, or discover 895 more undervalued stocks based on cash flows.

Approach 2: UMB Financial Price vs Earnings

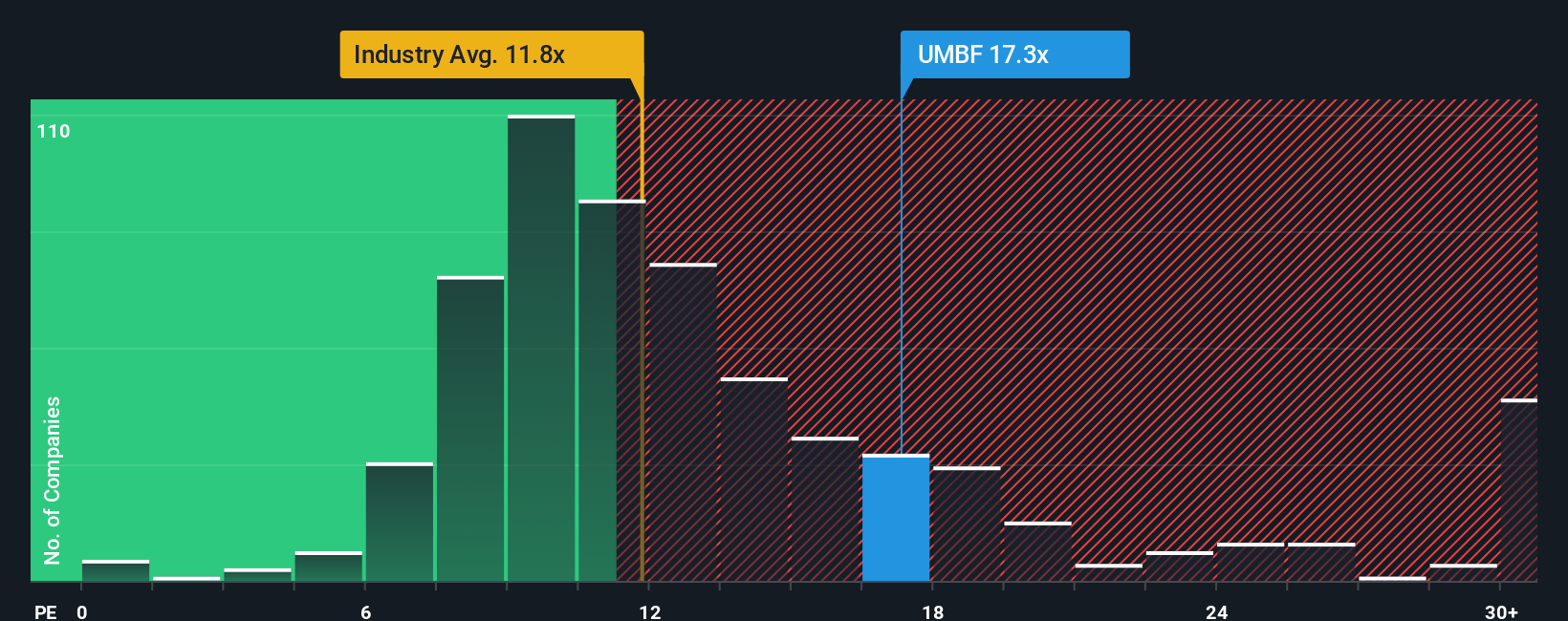

For a consistently profitable bank like UMB Financial, the price to earnings, or PE, multiple is a useful way to gauge how much investors are willing to pay for each dollar of current earnings. In general, faster growth and lower perceived risk justify a higher PE ratio, while slower growth or higher risk usually warrant a lower one. The question, then, is what a normal or fair PE looks like for this business.

UMB Financial currently trades on a PE of 14.54x, which is above the broader Banks industry average of 11.65x but only modestly ahead of its direct peer average of 13.36x. Simply Wall St’s proprietary Fair Ratio, which estimates what PE the stock deserves based on its earnings growth outlook, profitability, risk profile, size and industry, comes in higher at 16.38x. This Fair Ratio is more informative than a simple peer or industry comparison because it adjusts for UMB’s specific fundamentals rather than assuming all banks should trade on similar multiples. Comparing the current 14.54x PE to the 16.38x Fair Ratio suggests the shares trade at a discount relative to what the fundamentals support.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1450 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your UMB Financial Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, a simple tool that lets you attach a clear story about a company to the numbers you believe in, from its future revenue and earnings to its profit margins and fair value.

A Narrative connects three pieces together: what you think is happening in the business, how that story translates into a financial forecast, and what fair value those forecasts imply, so you can see exactly why a stock might be attractive or expensive.

On Simply Wall St, Narratives live in the Community page and are used by millions of investors. They make it easy to compare your view with others and to update your thinking as new information emerges.

Because each Narrative produces a fair value that you can line up against today’s share price, it becomes a practical decision tool to help you decide whether UMB Financial looks like a buy, hold, or sell at any point in time.

Narratives are dynamic, automatically refreshing when new earnings, news or guidance land. This means your fair value view for UMB Financial does not go stale the way a one-off spreadsheet might.

For example, one investor might build a bullish UMB Financial Narrative assuming fair value of about $150 per share, while a more cautious investor, focused on integration and regional risks, could land closer to $120. Yet both are using the same framework to reach different but transparent conclusions.

Do you think there's more to the story for UMB Financial? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com