Fuji Media Holdings (TSE:4676) Will Pay A Dividend Of ¥25.00

The board of Fuji Media Holdings, Inc. (TSE:4676) has announced that it will pay a dividend on the 26th of June, with investors receiving ¥25.00 per share. Including this payment, the dividend yield on the stock will be 1.4%, which is a modest boost for shareholders' returns.

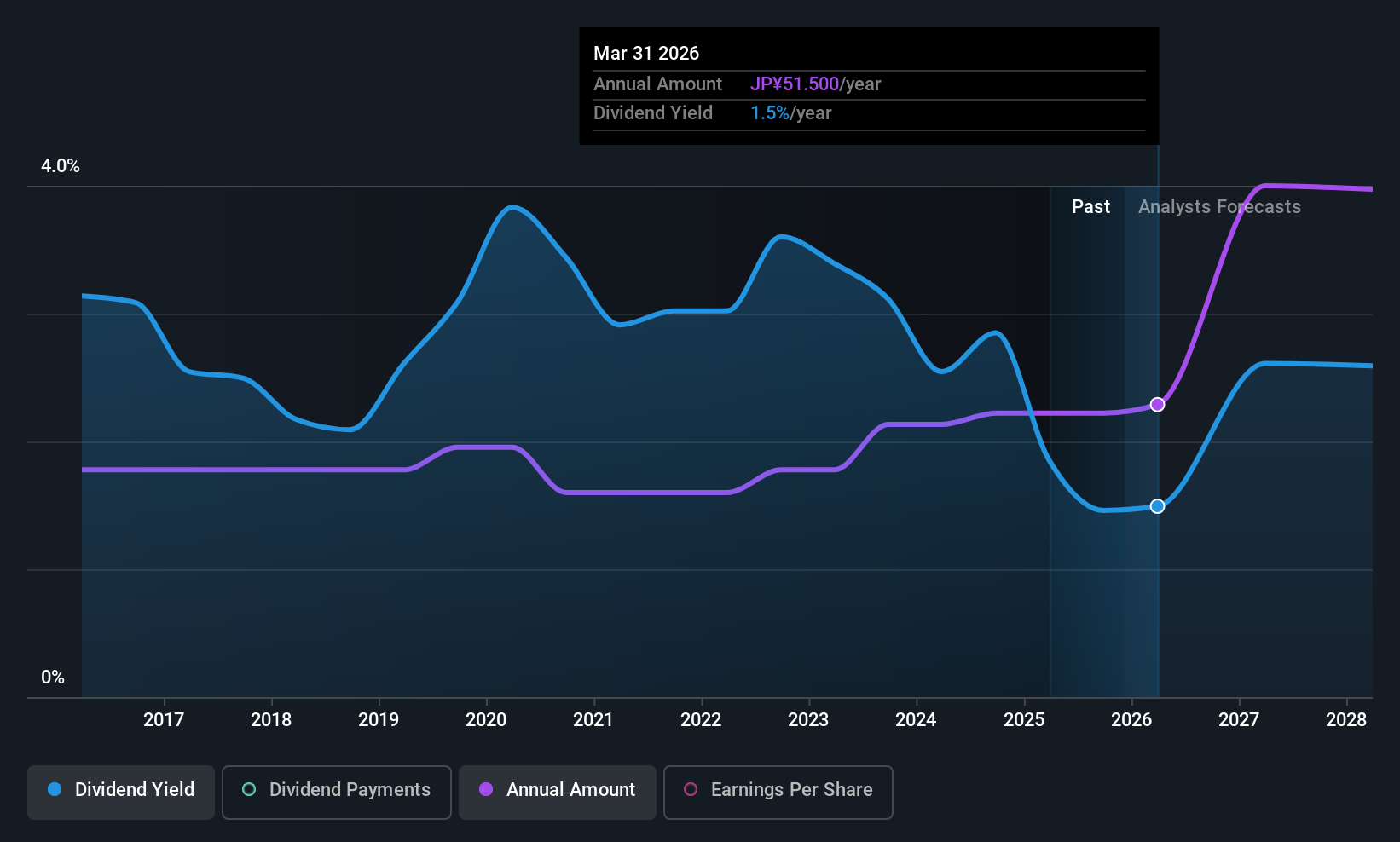

Fuji Media Holdings Might Find It Hard To Continue The Dividend

It would be nice for the yield to be higher, but we should also check if higher levels of dividend payment would be sustainable. Despite not generating a profit, Fuji Media Holdings is still paying a dividend. It is also not generating any free cash flow, we definitely have concerns when it comes to the sustainability of the dividend.

Over the next year, EPS is forecast to expand by 36.5%. This is the right direction to be moving, but it is not enough to achieve profitability. Unless this happens fairly soon, the dividend could start to come under pressure.

View our latest analysis for Fuji Media Holdings

Fuji Media Holdings Has A Solid Track Record

The company has a sustained record of paying dividends with very little fluctuation. Since 2015, the annual payment back then was ¥40.00, compared to the most recent full-year payment of ¥50.00. This works out to be a compound annual growth rate (CAGR) of approximately 2.3% a year over that time. Although we can't deny that the dividend has been remarkably stable in the past, the growth has been pretty muted.

Dividend Growth May Be Hard To Come By

Some investors will be chomping at the bit to buy some of the company's stock based on its dividend history. However, things aren't all that rosy. Over the past five years, it looks as though Fuji Media Holdings' EPS has declined at around 7.7% a year. A modest decline in earnings isn't great, and it makes it quite unlikely that the dividend will grow in the future unless that trend can be reversed. It's not all bad news though, as the earnings are predicted to rise over the next 12 months - we would just be a bit cautious until this can turn into a longer term trend.

Fuji Media Holdings' Dividend Doesn't Look Sustainable

Overall, we don't think this company makes a great dividend stock, even though the dividend wasn't cut this year. In the past the payments have been stable, but we think the company is paying out too much for this to continue for the long term. We would be a touch cautious of relying on this stock primarily for the dividend income.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Without at least some growth in earnings per share over time, the dividend will eventually come under pressure either from competition or inflation. Very few businesses see earnings consistently shrink year after year in perpetuity though, and so it might be worth seeing what the 6 analysts we track are forecasting for the future. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.