RTX (RTX): Valuation Check After Raytheon’s New Cloud and AI Partnership With AWS

RTX (RTX) just deepened its push into defense tech by having Raytheon team up with Amazon Web Services, aiming to move satellite data processing and mission control into a cloud native, AI driven model.

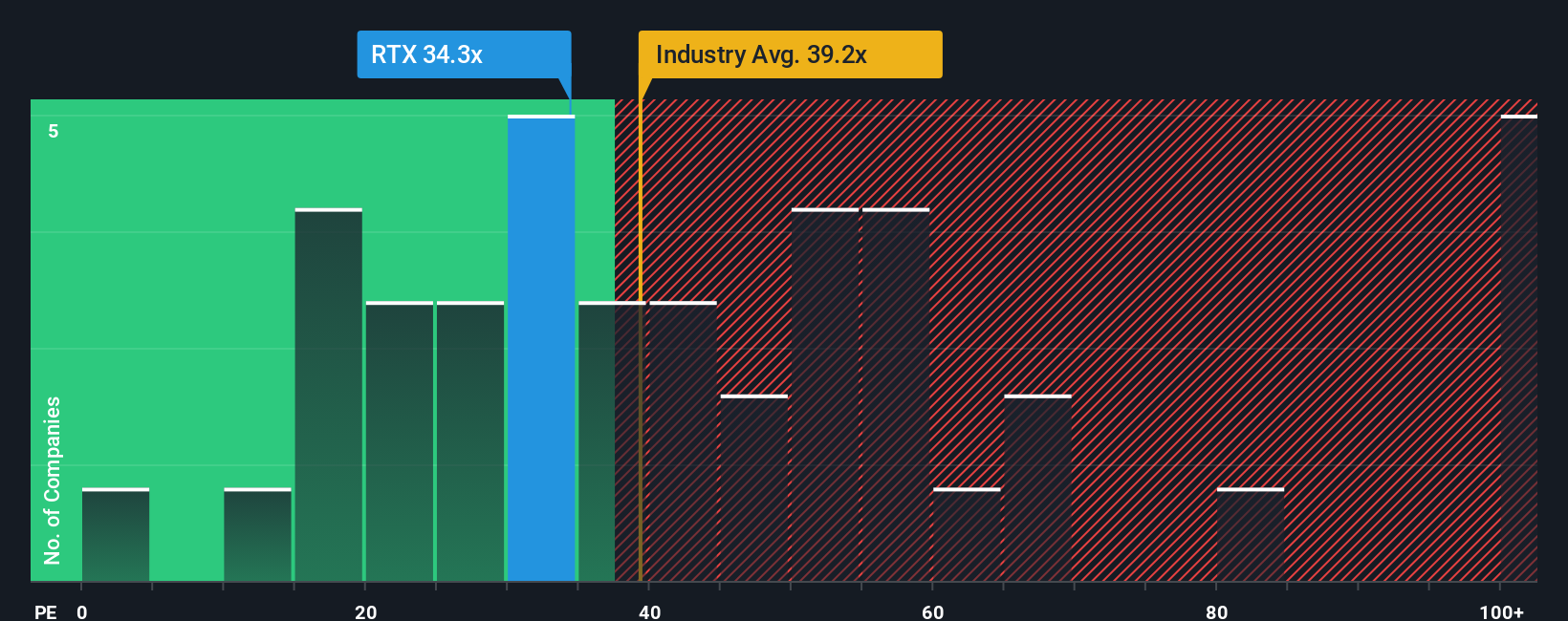

See our latest analysis for RTX.

This tie up lands at a time when RTX shares are trading around $174.72, with a strong year to date share price return of just over 50 percent and a five year total shareholder return approaching 180 percent. This suggests that momentum in the story is still very much intact.

If this kind of cloud powered defense innovation has your attention, it could be worth scanning other aerospace and defense names through aerospace and defense stocks to see what else matches your thesis.

Yet with RTX trading near record highs and only a modest discount to Wall Street targets, investors need to ask whether the stock is still undervalued or if the market is already pricing in years of cloud driven growth.

Most Popular Narrative: 9.8% Undervalued

With RTX closing at $174.72 against a narrative fair value near $193.79, the storyline leans toward upside, built on steady growth and richer margins.

Strategic portfolio optimization, with divestitures of non core assets (e.g., $1.8B sale of actuation business and $765M sale of Collins Simmonds Precision Products), is sharpening RTX's focus on core aerospace and defense, improving capital allocation and return on invested capital, and freeing balance sheet capacity for further innovation, all of which are likely to drive higher net margins and free cash flow over time.

If you want to see what kind of revenue runway and margin lift underpin that higher value, and how long earnings are expected to compound at this pace, explore the full narrative for the precise assumptions behind that target.

Result: Fair Value of $193.79 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent jet engine reliability issues and any unexpected pullback in defense budgets could quickly chip away at today’s upbeat RTX narrative.

Find out about the key risks to this RTX narrative.

Another Lens on Value

On a straight earnings multiple, RTX looks far less generous. It trades at about 35.5 times earnings versus a 35.3 times fair ratio, 34.6 times for peers, and 36.7 times for the wider Aerospace and Defense group, implying only a sliver of upside before sentiment turns.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own RTX Narrative

If you are not fully aligned with this view, or would rather dig into the numbers yourself, you can craft a personalized RTX thesis in under three minutes, Do it your way.

A great starting point for your RTX research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Ready for more high conviction opportunities?

Do not stop with RTX when the market is packed with potential. Use the Simply Wall Street Screener to spot your next strong, data backed idea today.

- Capture overlooked value by targeting these 908 undervalued stocks based on cash flows that cash flow analysis suggests the market has not fully appreciated yet.

- Ride powerful innovation trends as you assess these 26 AI penny stocks positioned to benefit from accelerating advances in artificial intelligence.

- Lock in income potential by scanning these 12 dividend stocks with yields > 3% that could strengthen your portfolio with reliable cash returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com