Is Artisan Partners Still Attractive After Its Recent Share Price Pullback?

- If you are wondering whether Artisan Partners Asset Management is quietly turning into a value opportunity or if the market is pricing it just right, this article will walk through what the numbers are really saying.

- The stock has pulled back recently, down around 3.3% over the last week and 8.8% over the past month, even though the 3 year return is still a strong 56.7% and 5 year performance sits at 22.1%.

- That combination of a recent slide and still solid multi year gains has come alongside shifting sentiment in asset managers generally, as investors reassess fee pressure, flows into active strategies, and the impact of higher for longer interest rates on equity markets. Broader debates about whether active managers can keep winning back assets from passive funds are also influencing how stocks like Artisan Partners are being priced.

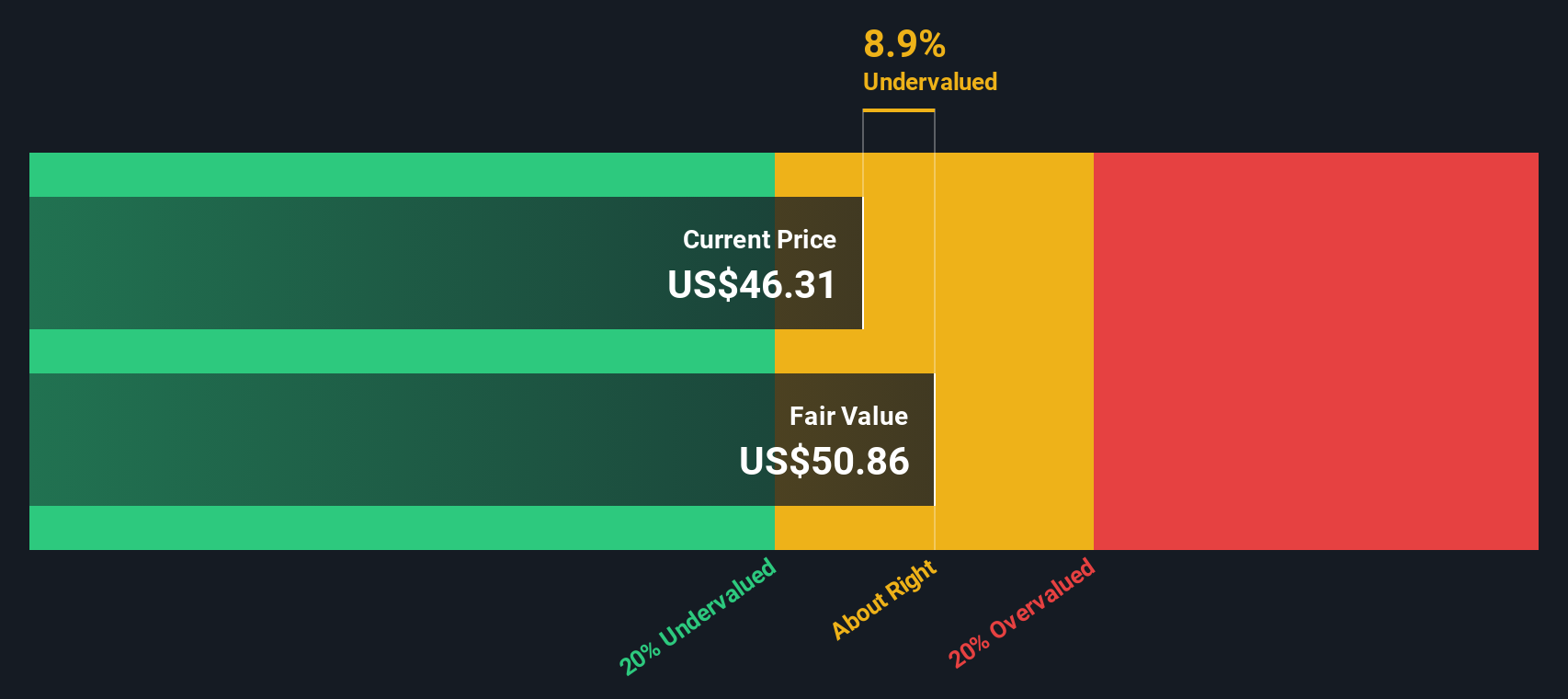

- Right now, Artisan Partners scores a 4/6 valuation score, suggesting it screens as undervalued on most of our key checks, though not all of them. Next we will break down what different valuation approaches say about the stock, before finishing with a more powerful way to think about its long term value story.

Approach 1: Artisan Partners Asset Management Excess Returns Analysis

The Excess Returns model looks at how much profit a company can generate above the return that shareholders reasonably demand, then capitalizes those excess profits into an intrinsic value per share.

For Artisan Partners, the model starts with a Book Value of $5.71 per share and a Stable EPS of $2.54 per share, based on the median return on equity from the past 5 years. With an Average Return on Equity of 53.69% and a Stable Book Value of $4.73 per share, the firm is estimated to earn an Excess Return of $2.14 per share after covering its Cost of Equity of $0.40 per share.

These excess returns are then projected forward and discounted back to arrive at an intrinsic value of about $46.71 per share. Compared with the current share price, this indicates the stock is valued at roughly a 12.0% discount to this intrinsic value, which reflects a gap between the market price and the model’s estimate of Artisan Partners ability to earn above its cost of capital.

Result: UNDERVALUED

Our Excess Returns analysis suggests Artisan Partners Asset Management is undervalued by 12.0%. Track this in your watchlist or portfolio, or discover 908 more undervalued stocks based on cash flows.

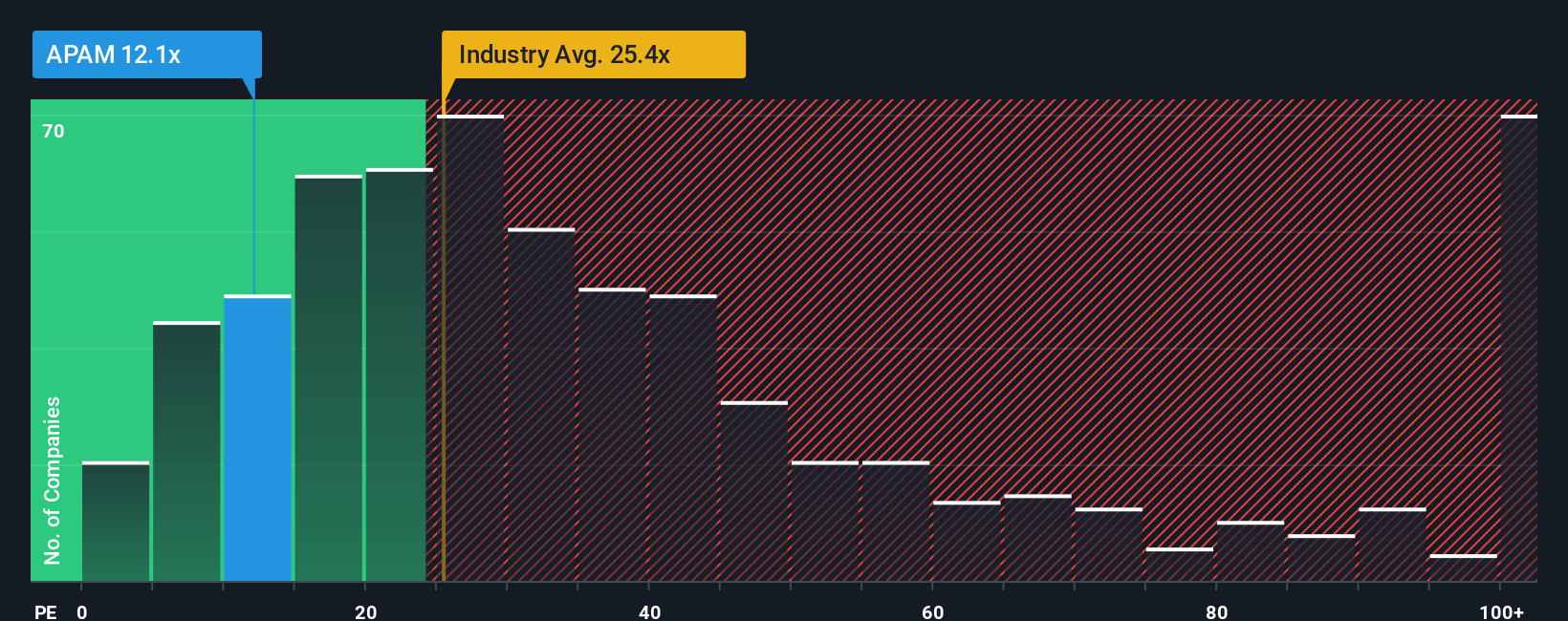

Approach 2: Artisan Partners Asset Management Price vs Earnings

For a consistently profitable business like Artisan Partners, the price to earnings, or PE, ratio is a natural way to gauge valuation because it links what investors pay directly to the company’s current earnings power. In general, companies with stronger and more reliable growth, and lower perceived risk, are often associated with higher PE multiples, while slower growing or riskier firms are often associated with lower ones.

Artisan Partners currently trades on a PE of about 11.9x, which is below both the Capital Markets industry average of roughly 25.8x and the peer group average of around 14.2x. To move beyond those broad comparisons, Simply Wall St uses a proprietary Fair Ratio. This metric estimates what a reasonable PE could be once you factor in the company’s earnings growth profile, profitability, industry positioning, market cap and specific risk characteristics.

This Fair Ratio for Artisan Partners is 14.3x, modestly above the current 11.9x multiple. That suggests the shares trade at a discount to what might be expected given their fundamentals and risk profile, indicating the stock appears undervalued on a PE basis rather than fairly priced or expensive.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1446 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Artisan Partners Asset Management Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which are simply your own story about a company linked to clear assumptions about its future revenue, earnings, margins and what you think is a fair value today. On Simply Wall St’s Community page, millions of investors use Narratives to connect the qualitative view, like Artisan Partners expanding from 5 to 11 investment teams and targeting private wealth clients, with a quantitative forecast of how fast revenue might grow, how margins might shift and what PE multiple is reasonable. Each Narrative translates those assumptions into a fair value that you can compare directly with the current share price to decide whether you see Artisan Partners as a buy, hold or sell, and it automatically updates as new earnings, news or guidance come in. For example, one investor might focus on rising costs and choose a cautious view closer to 41.50 per share, while another leans into growth across more strategies and sees upside toward 51.00, and both perspectives become living, data driven Narratives you can track over time.

Do you think there's more to the story for Artisan Partners Asset Management? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com