Here's Why Gold Fields (JSE:GFI) Has Caught The Eye Of Investors

For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it currently lacks a track record of revenue and profit. Sometimes these stories can cloud the minds of investors, leading them to invest with their emotions rather than on the merit of good company fundamentals. Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

If this kind of company isn't your style, you like companies that generate revenue, and even earn profits, then you may well be interested in Gold Fields (JSE:GFI). Now this is not to say that the company presents the best investment opportunity around, but profitability is a key component to success in business.

Gold Fields' Earnings Per Share Are Growing

Generally, companies experiencing growth in earnings per share (EPS) should see similar trends in share price. So it makes sense that experienced investors pay close attention to company EPS when undertaking investment research. It certainly is nice to see that Gold Fields has managed to grow EPS by 27% per year over three years. If the company can sustain that sort of growth, we'd expect shareholders to come away satisfied.

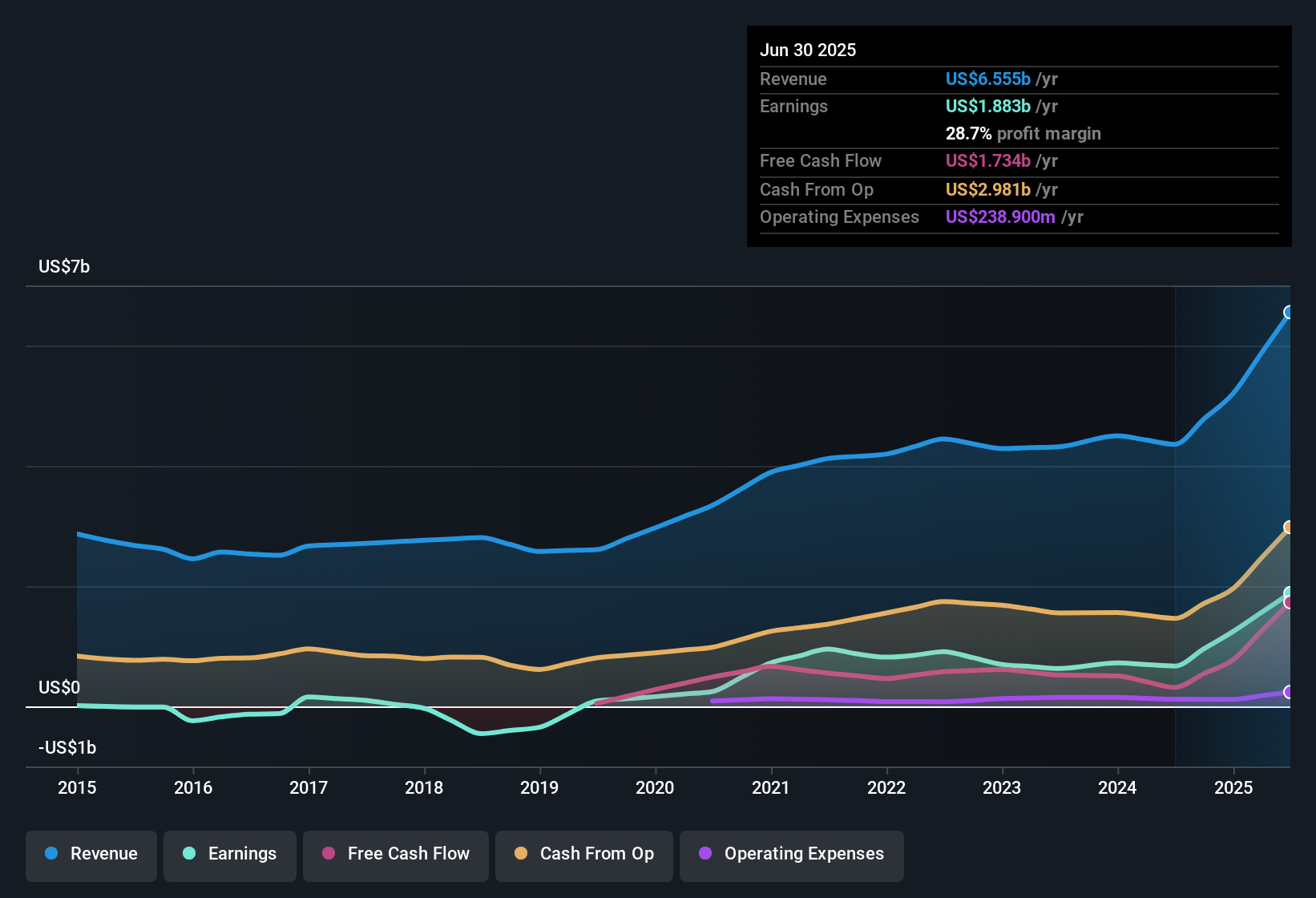

It's often helpful to take a look at earnings before interest and tax (EBIT) margins, as well as revenue growth, to get another take on the quality of the company's growth. The good news is that Gold Fields is growing revenues, and EBIT margins improved by 14.5 percentage points to 45%, over the last year. That's great to see, on both counts.

The chart below shows how the company's bottom and top lines have progressed over time. Click on the chart to see the exact numbers.

View our latest analysis for Gold Fields

In investing, as in life, the future matters more than the past. So why not check out this free interactive visualization of Gold Fields' forecast profits?

Are Gold Fields Insiders Aligned With All Shareholders?

Investors are always searching for a vote of confidence in the companies they hold and insider buying is one of the key indicators for optimism on the market. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. However, small purchases are not always indicative of conviction, and insiders don't always get it right.

The good news is that Gold Fields insiders spent a whopping US$106m on stock in just one year, without so much as a single sale. Knowing this, Gold Fields will have have all eyes on them in anticipation for the what could happen in the near future. It is also worth noting that it was CEO & Executive Director Michael Fraser who made the biggest single purchase, worth R28m, paying R346 per share.

On top of the insider buying, it's good to see that Gold Fields insiders have a valuable investment in the business. To be specific, they have US$612m worth of shares. That's a lot of money, and no small incentive to work hard. Even though that's only about 0.09% of the company, it's enough money to indicate alignment between the leaders of the business and ordinary shareholders.

While insiders are apparently happy to hold and accumulate shares, that is just part of the big picture. That's because Gold Fields' CEO, Mike Fraser, is paid at a relatively modest level when compared to other CEOs for companies of this size. The median total compensation for CEOs of companies similar in size to Gold Fields, with market caps over US$8.0b, is around US$2.7m.

The Gold Fields CEO received total compensation of just US$1.3m in the year to December 2024. That looks like a modest pay packet, and may hint at a certain respect for the interests of shareholders. CEO remuneration levels are not the most important metric for investors, but when the pay is modest, that does support enhanced alignment between the CEO and the ordinary shareholders. It can also be a sign of good governance, more generally.

Is Gold Fields Worth Keeping An Eye On?

For growth investors, Gold Fields' raw rate of earnings growth is a beacon in the night. On top of that, insiders own a significant stake in the company and have been buying more shares. These things considered, this is one stock worth watching. We should say that we've discovered 1 warning sign for Gold Fields that you should be aware of before investing here.

There are plenty of other companies that have insiders buying up shares. So if you like the sound of Gold Fields, you'll probably love this curated collection of companies in ZA that have an attractive valuation alongside insider buying in the last three months.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.