ABM Industries (ABM): Rethinking Valuation After Recent 1-Month Share Price Rebound

ABM Industries (ABM) has quietly outperformed the broader market over the past month, with the stock climbing about 9% even as its year to date and 1 year returns remain negative.

See our latest analysis for ABM Industries.

That recent 1 month share price return of 8.54% to about $45.90 stands in contrast to a weaker year to date share price return and a negative 1 year total shareholder return. This suggests near term momentum is improving even as the longer term picture remains more muted.

If ABM’s shift in momentum has you rethinking your watchlist, this could be a good time to explore fast growing stocks with high insider ownership for other ideas with strong conviction behind them.

With ABM trading at a notable discount to analyst targets despite steady revenue growth and sharply improving earnings, investors now face a key question: is this a mispriced value opportunity, or is the market already discounting future gains?

Most Popular Narrative Narrative: 20.9% Undervalued

With ABM closing at $45.90 versus a narrative fair value of $58, the story hinges on whether today’s earnings power can scale meaningfully higher.

The strong growth in electrification, microgrids, and data center infrastructure, fueled by both sustainability trends and the surging need for resilient/efficient power solutions (accelerated by AI adoption), positions ABM's Technical Solutions segment for durable revenue and earnings expansion as these end markets scale.

Curious how modest top line growth can still back a higher price tag? The narrative leans on ambitious margin expansion and a sharply different earnings profile. Want to see how those moving parts are modeled over time? Read how they stack revenue, profits, and the final multiple into one valuation roadmap.

Result: Fair Value of $58 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, if margin pressures from pricing concessions persist, or if shorter term, lower margin contracts fail to scale, today’s undervaluation case could quickly unravel.

Find out about the key risks to this ABM Industries narrative.

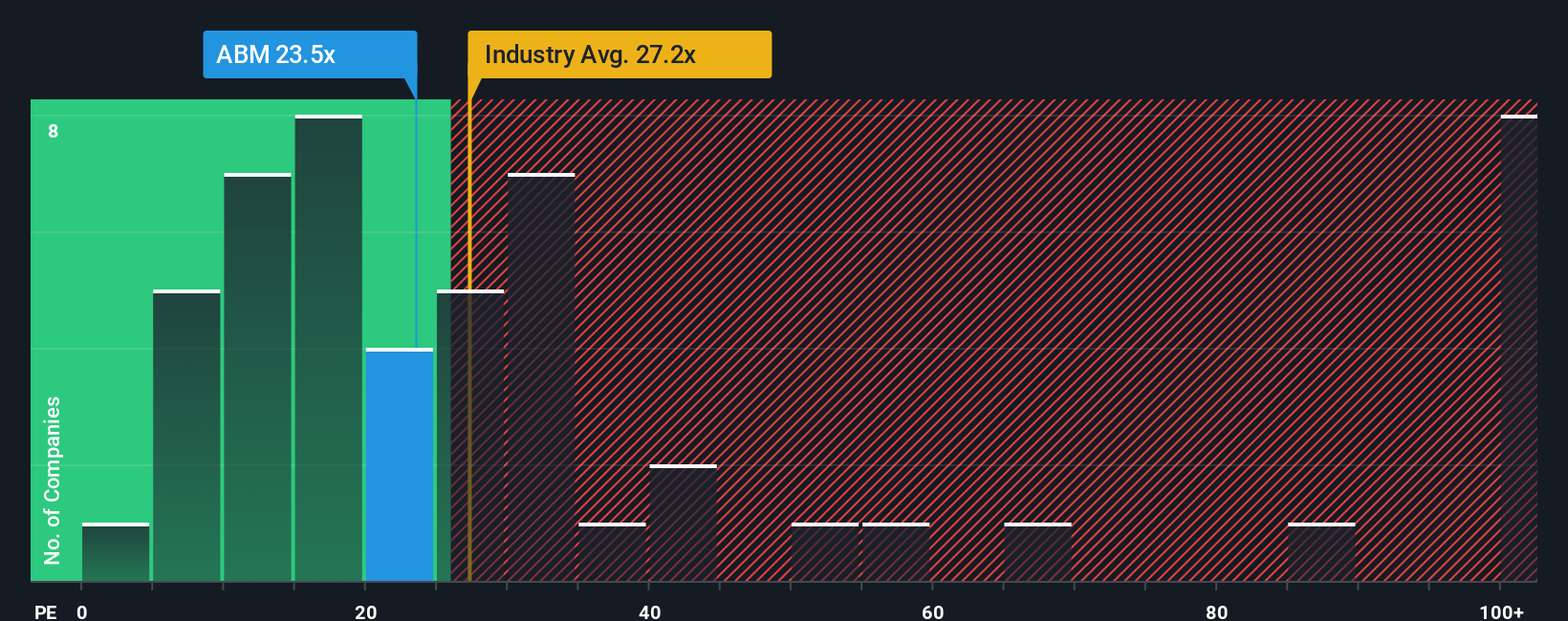

Another View: What Earnings Ratios Are Saying

On current earnings, ABM trades at about 24.3 times profits, slightly richer than the US Commercial Services average of 23.5 times, but cheaper than close peers at 47.3 times and below a fair ratio of 30.6 times. Is that a comfortable margin of safety, or a value trap if margins disappoint?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own ABM Industries Narrative

If you see the story differently or want to stress test the numbers yourself, build a personalized view in just a few minutes: Do it your way.

A great starting point for your ABM Industries research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before you move on, lock in your next opportunity by scanning focused stock ideas built from real fundamentals, growth potential, and risk checks on Simply Wall St.

- Capture contrarian upside by targeting mispriced businesses using these 907 undervalued stocks based on cash flows grounded in forward cash flows and earnings quality.

- Capitalize on the momentum behind intelligent automation with these 26 AI penny stocks that could reshape how entire industries operate.

- Strengthen your income strategy by reviewing these 12 dividend stocks with yields > 3% that aim to pair attractive yields with sustainable payout profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com