ikuyo Co.,Ltd.'s (TSE:7273) Share Price Is Still Matching Investor Opinion Despite 25% Slump

To the annoyance of some shareholders, ikuyo Co.,Ltd. (TSE:7273) shares are down a considerable 25% in the last month, which continues a horrid run for the company. The good news is that in the last year, the stock has shone bright like a diamond, gaining 189%.

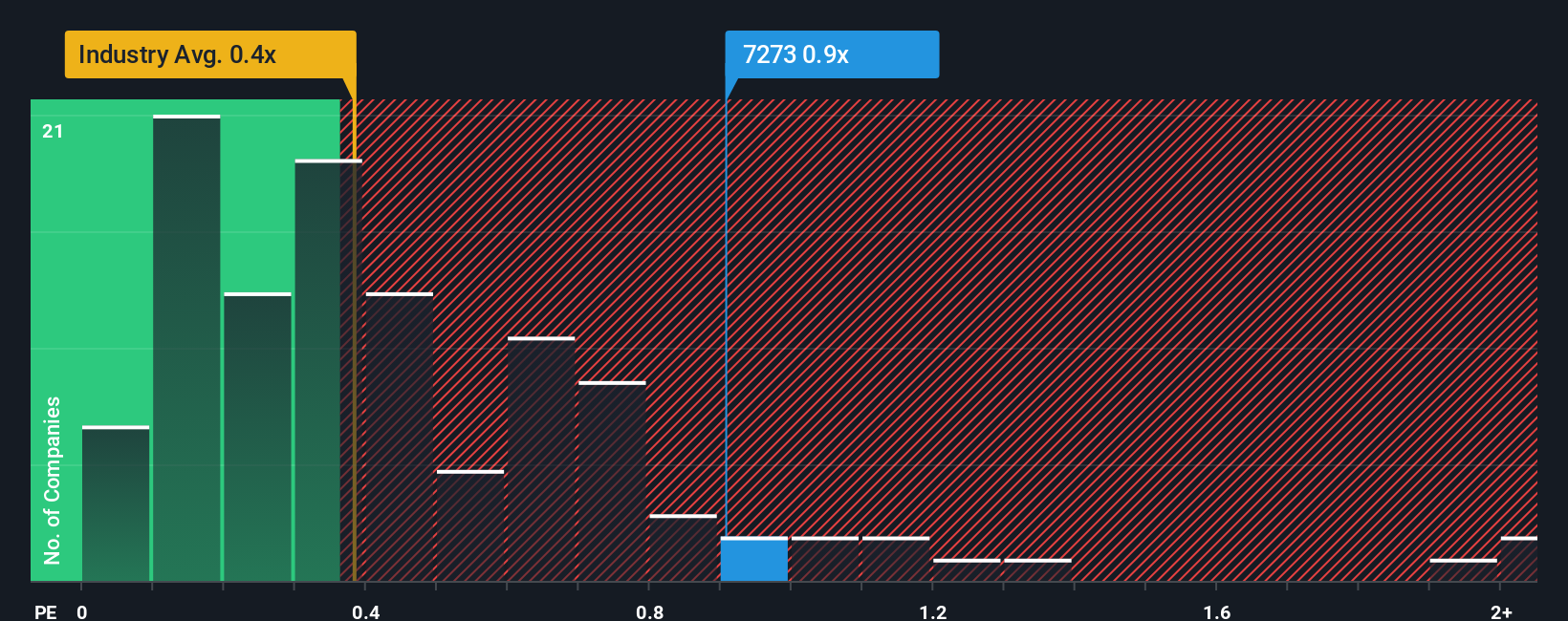

Even after such a large drop in price, you could still be forgiven for thinking ikuyoLtd is a stock not worth researching with a price-to-sales ratios (or "P/S") of 0.9x, considering almost half the companies in Japan's Auto Components industry have P/S ratios below 0.4x. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

Check out our latest analysis for ikuyoLtd

How ikuyoLtd Has Been Performing

With revenue growth that's exceedingly strong of late, ikuyoLtd has been doing very well. It seems that many are expecting the strong revenue performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Although there are no analyst estimates available for ikuyoLtd, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Do Revenue Forecasts Match The High P/S Ratio?

There's an inherent assumption that a company should outperform the industry for P/S ratios like ikuyoLtd's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 35% gain to the company's top line. The latest three year period has also seen an excellent 77% overall rise in revenue, aided by its short-term performance. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Comparing that recent medium-term revenue trajectory with the industry's one-year growth forecast of 1.7% shows it's noticeably more attractive.

In light of this, it's understandable that ikuyoLtd's P/S sits above the majority of other companies. Presumably shareholders aren't keen to offload something they believe will continue to outmanoeuvre the wider industry.

The Final Word

Despite the recent share price weakness, ikuyoLtd's P/S remains higher than most other companies in the industry. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of ikuyoLtd revealed its three-year revenue trends are contributing to its high P/S, given they look better than current industry expectations. Right now shareholders are comfortable with the P/S as they are quite confident revenue aren't under threat. Barring any significant changes to the company's ability to make money, the share price should continue to be propped up.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 3 warning signs with ikuyoLtd (at least 2 which don't sit too well with us), and understanding these should be part of your investment process.

If these risks are making you reconsider your opinion on ikuyoLtd, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.