We Take A Look At Why Atlanta Poland S.A.'s (WSE:ATP) CEO Has Earned Their Pay Packet

Key Insights

- Atlanta Poland to hold its Annual General Meeting on 18th of December

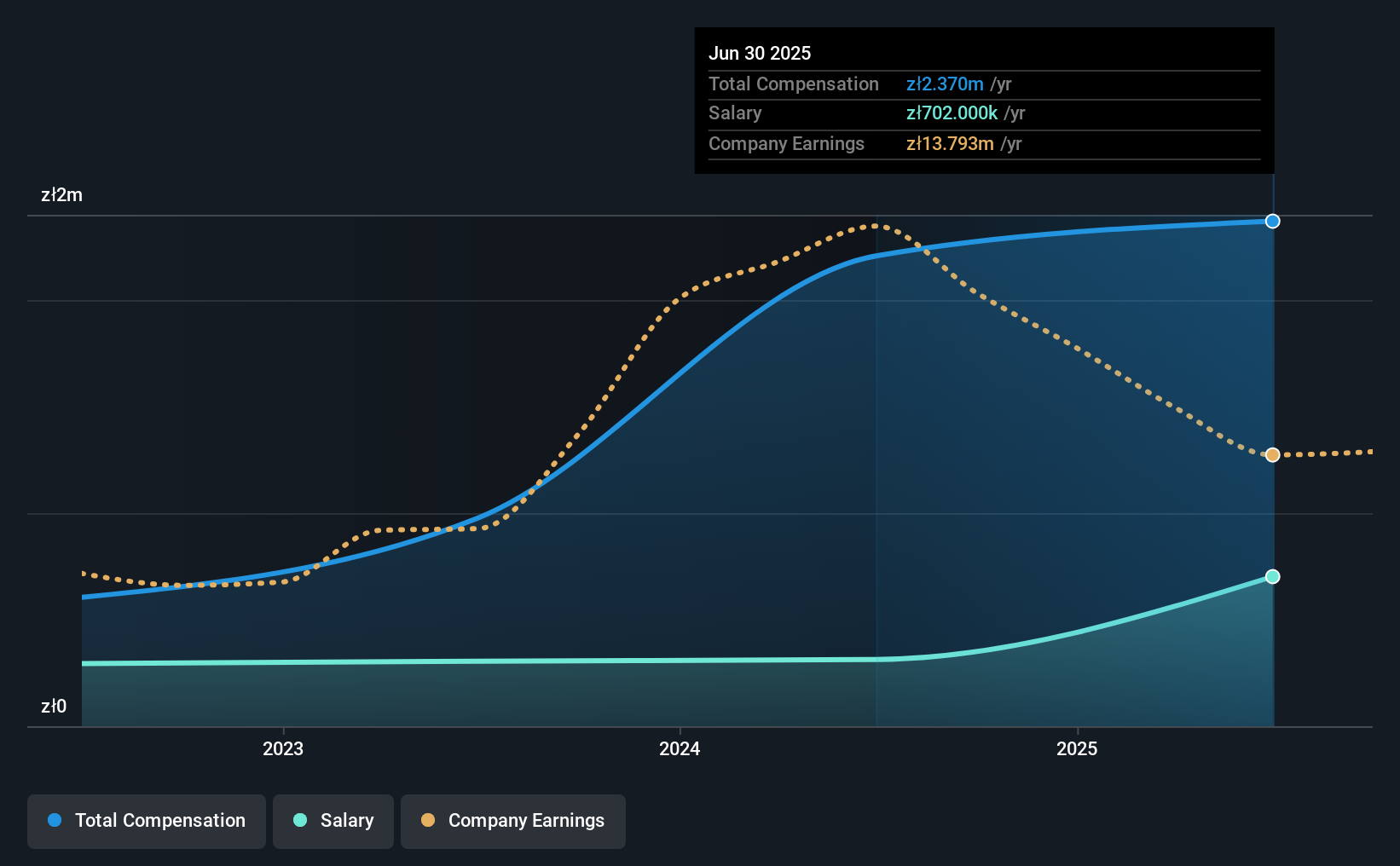

- CEO Piotr Bielinski's total compensation includes salary of zł702.0k

- The total compensation is similar to the average for the industry

- Atlanta Poland's total shareholder return over the past three years was 115% while its EPS grew by 25% over the past three years

We have been pretty impressed with the performance at Atlanta Poland S.A. (WSE:ATP) recently and CEO Piotr Bielinski deserves a mention for their role in it. Coming up to the next AGM on 18th of December, shareholders would be keeping this in mind. This would also be a chance for them to hear the board review the financial results, discuss future company strategy and vote on any resolutions such as executive remuneration. In light of the great performance, we discuss the case why we think CEO compensation is not excessive.

Check out our latest analysis for Atlanta Poland

Comparing Atlanta Poland S.A.'s CEO Compensation With The Industry

At the time of writing, our data shows that Atlanta Poland S.A. has a market capitalization of zł103m, and reported total annual CEO compensation of zł2.4m for the year to June 2025. That's a fairly small increase of 7.4% over the previous year. We think total compensation is more important but our data shows that the CEO salary is lower, at zł702k.

On comparing similar-sized companies in the Poland Consumer Retailing industry with market capitalizations below zł719m, we found that the median total CEO compensation was zł2.2m. This suggests that Atlanta Poland remunerates its CEO largely in line with the industry average.

| Component | 2025 | 2024 | Proportion (2025) |

| Salary | zł702k | zł313k | 30% |

| Other | zł1.7m | zł1.9m | 70% |

| Total Compensation | zł2.4m | zł2.2m | 100% |

Talking in terms of the industry, salary represented approximately 47% of total compensation out of all the companies we analyzed, while other remuneration made up 53% of the pie. Atlanta Poland pays a modest slice of remuneration through salary, as compared to the broader industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

A Look at Atlanta Poland S.A.'s Growth Numbers

Atlanta Poland S.A. has seen its earnings per share (EPS) increase by 25% a year over the past three years. It achieved revenue growth of 13% over the last year.

Shareholders would be glad to know that the company has improved itself over the last few years. This sort of respectable year-on-year revenue growth is often seen at a healthy, growing business. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Atlanta Poland S.A. Been A Good Investment?

We think that the total shareholder return of 115%, over three years, would leave most Atlanta Poland S.A. shareholders smiling. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

To Conclude...

Seeing that the company has put in a relatively good performance, the CEO remuneration policy may not be the focus at the AGM. Instead, investors might be more interested in discussions that would help manage their longer-term growth expectations such as company business strategies and future growth potential.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. That's why we did some digging and identified 3 warning signs for Atlanta Poland that you should be aware of before investing.

Switching gears from Atlanta Poland, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.