Sensorion SA's (EPA:ALSEN) market cap surged €12m last week, retail investors who have a lot riding on the company were rewarded

Key Insights

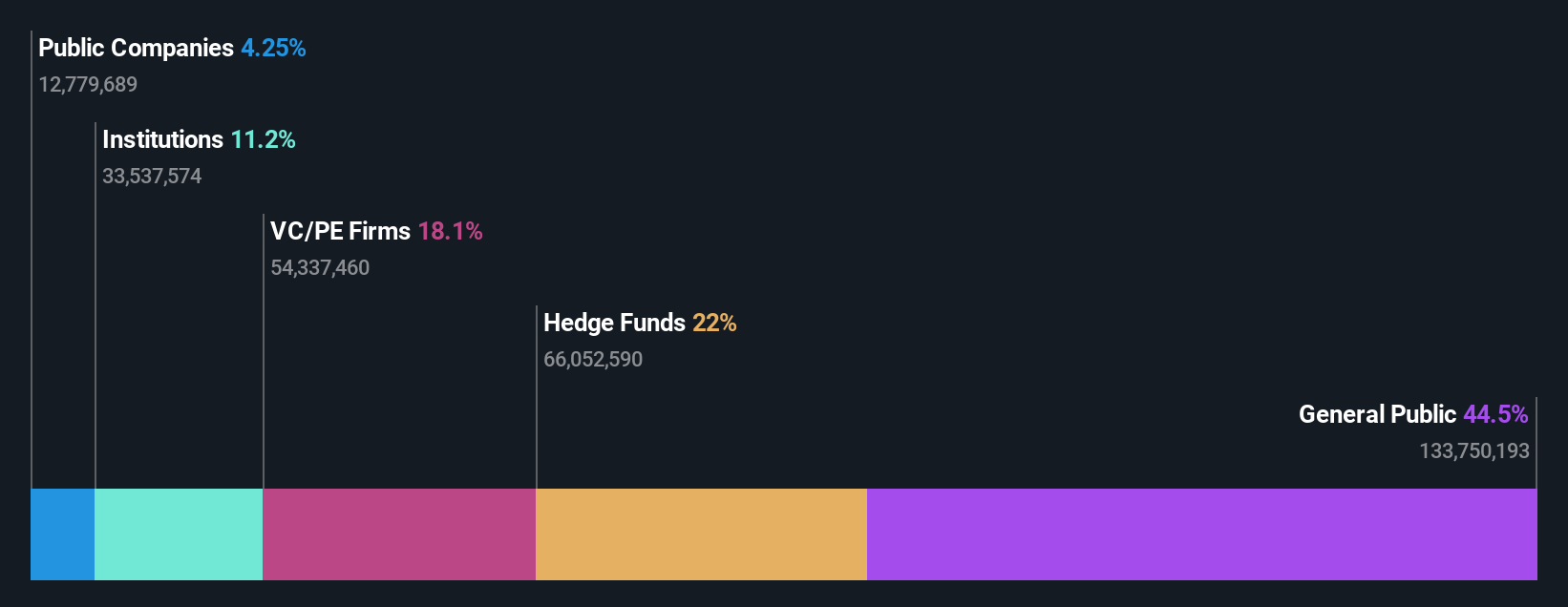

- Significant control over Sensorion by retail investors implies that the general public has more power to influence management and governance-related decisions

- 50% of the business is held by the top 4 shareholders

- 11% of Sensorion is held by Institutions

Every investor in Sensorion SA (EPA:ALSEN) should be aware of the most powerful shareholder groups. We can see that retail investors own the lion's share in the company with 45% ownership. Put another way, the group faces the maximum upside potential (or downside risk).

As a result, retail investors were the biggest beneficiaries of last week’s 13% gain.

Let's take a closer look to see what the different types of shareholders can tell us about Sensorion.

Check out our latest analysis for Sensorion

What Does The Institutional Ownership Tell Us About Sensorion?

Institutional investors commonly compare their own returns to the returns of a commonly followed index. So they generally do consider buying larger companies that are included in the relevant benchmark index.

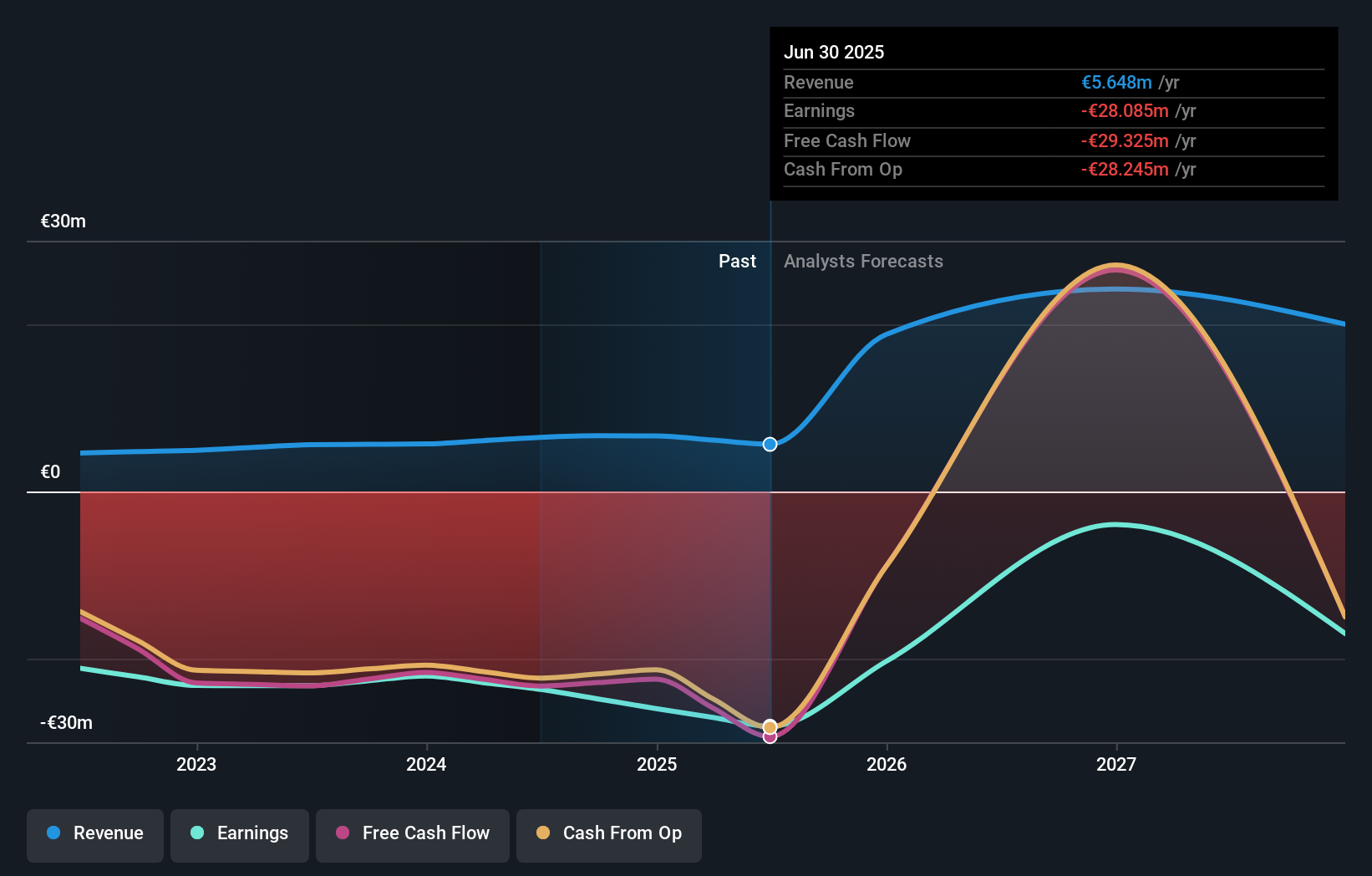

Sensorion already has institutions on the share registry. Indeed, they own a respectable stake in the company. This implies the analysts working for those institutions have looked at the stock and they like it. But just like anyone else, they could be wrong. When multiple institutions own a stock, there's always a risk that they are in a 'crowded trade'. When such a trade goes wrong, multiple parties may compete to sell stock fast. This risk is higher in a company without a history of growth. You can see Sensorion's historic earnings and revenue below, but keep in mind there's always more to the story.

It looks like hedge funds own 22% of Sensorion shares. That catches my attention because hedge funds sometimes try to influence management, or bring about changes that will create near term value for shareholders. Looking at our data, we can see that the largest shareholder is Redmile Group, LLC with 22% of shares outstanding. For context, the second largest shareholder holds about 18% of the shares outstanding, followed by an ownership of 6.0% by the third-largest shareholder.

To make our study more interesting, we found that the top 4 shareholders control more than half of the company which implies that this group has considerable sway over the company's decision-making.

While studying institutional ownership for a company can add value to your research, it is also a good practice to research analyst recommendations to get a deeper understand of a stock's expected performance. Quite a few analysts cover the stock, so you could look into forecast growth quite easily.

Insider Ownership Of Sensorion

While the precise definition of an insider can be subjective, almost everyone considers board members to be insiders. Management ultimately answers to the board. However, it is not uncommon for managers to be executive board members, especially if they are a founder or the CEO.

Most consider insider ownership a positive because it can indicate the board is well aligned with other shareholders. However, on some occasions too much power is concentrated within this group.

We note our data does not show any board members holding shares, personally. Not all jurisdictions have the same rules around disclosing insider ownership, and it is possible we have missed something, here. So you can click here learn more about the CEO.

General Public Ownership

The general public, who are usually individual investors, hold a 45% stake in Sensorion. While this group can't necessarily call the shots, it can certainly have a real influence on how the company is run.

Private Equity Ownership

With an ownership of 18%, private equity firms are in a position to play a role in shaping corporate strategy with a focus on value creation. Some investors might be encouraged by this, since private equity are sometimes able to encourage strategies that help the market see the value in the company. Alternatively, those holders might be exiting the investment after taking it public.

Public Company Ownership

Public companies currently own 4.3% of Sensorion stock. We can't be certain but it is quite possible this is a strategic stake. The businesses may be similar, or work together.

Next Steps:

It's always worth thinking about the different groups who own shares in a company. But to understand Sensorion better, we need to consider many other factors. Be aware that Sensorion is showing 2 warning signs in our investment analysis , you should know about...

But ultimately it is the future, not the past, that will determine how well the owners of this business will do. Therefore we think it advisable to take a look at this free report showing whether analysts are predicting a brighter future.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.