Evaluating PDF Solutions (PDFS) Valuation After Its Recent 65% Three-Month Share Price Surge

PDF Solutions (PDFS) has quietly put together an impressive run, with the stock up about 65% over the past 3 months as investors warm to its role in semiconductor manufacturing analytics and yield improvement.

See our latest analysis for PDF Solutions.

That 64.7% 3 month share price return comes after a much more modest 5.1% 1 year total shareholder return. This suggests momentum has only really kicked in recently as investors reassess its growth and risk profile around $31.92.

If PDF Solutions has you rethinking what leadership in chip analytics looks like, it could be a good moment to explore other high growth tech and AI stocks that are starting to attract similar attention.

With revenue growing double digits but profits still elusive and the share price now sitting just below analyst targets, is PDF Solutions a quietly mispriced enabler of chip innovation, or is the market already banking on years of future growth?

Most Popular Narrative: 8.1% Undervalued

With the narrative fair value set at $34.75 against a last close of $31.92, the story centers on earnings power catching up to rapid top line growth.

The company's disciplined operating expense growth relative to revenue, combined with high margin analytics software sales, is driving operating margin expansion, setting the stage for improved net margins and long term EPS growth.

Read the complete narrative.

Curious how a still unprofitable chip analytics specialist earns a premium style valuation? The narrative leans heavily on rapid margin expansion and ambitious earnings multiples. Want to see how those assumptions stack up over the next few years and what needs to go right for this price target to hold up?

Result: Fair Value of $34.75 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this upbeat narrative could be tested if geopolitical tensions squeeze China demand or heavy R&D spending fails to translate into profitable, scalable growth.

Find out about the key risks to this PDF Solutions narrative.

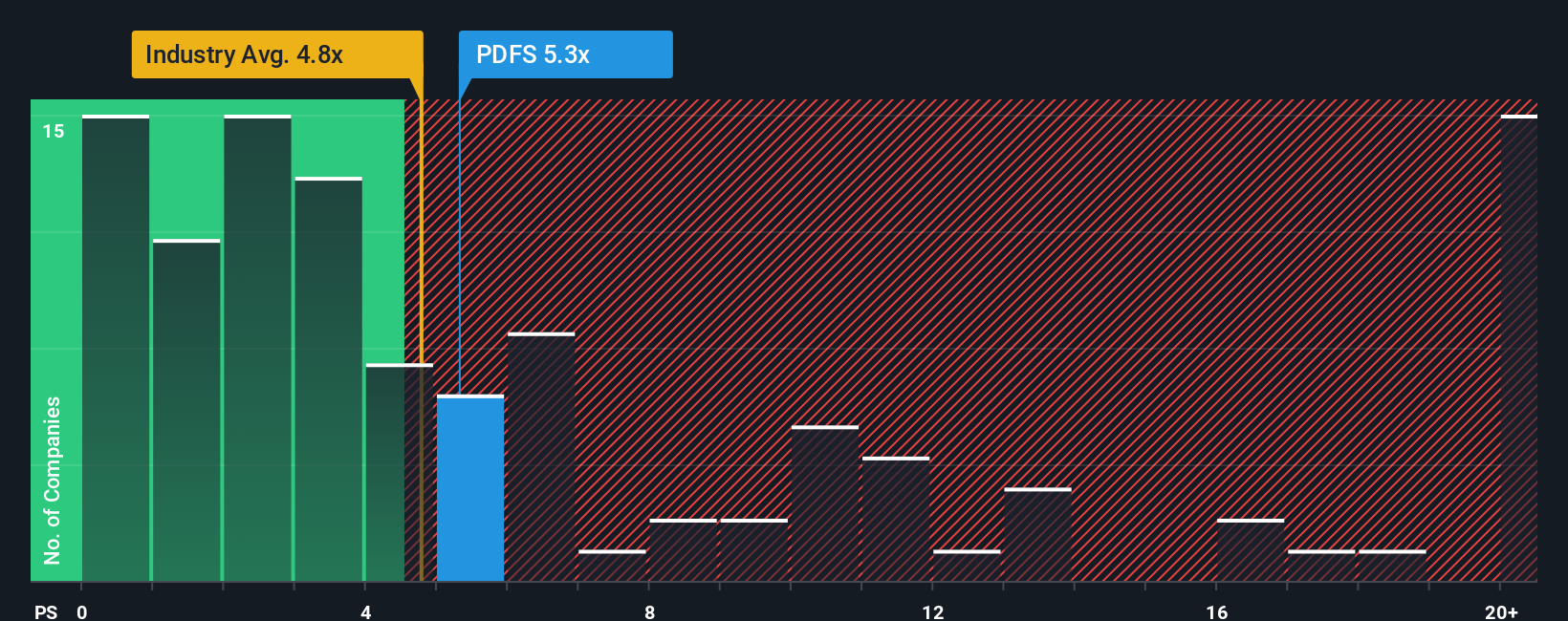

Another View: Rich on Sales

While the narrative suggests upside, a simple price to sales lens looks less generous. PDF Solutions trades at 6.1 times sales, richer than both the US semiconductor industry at 5.6 times and its peer average of 5 times. Is the market already paying up for that future growth?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own PDF Solutions Narrative

If this perspective does not fully align with your own, dive into the data yourself and craft a personalized view in minutes, Do it your way.

A good starting point is our analysis highlighting 1 key reward investors are optimistic about regarding PDF Solutions.

Ready for more investment ideas?

Before the next move in PDF Solutions unfolds, set yourself up with a watchlist of fresh opportunities using the Simply Wall Street Screener and stay a step ahead.

- Capture potential turnaround stories by scanning these 3609 penny stocks with strong financials that combine smaller market caps with surprisingly resilient fundamentals and improving financial trends.

- Position your portfolio for the next wave of automation by targeting these 25 AI penny stocks riding structural demand for intelligent software and data driven decision making.

- Strengthen your margin of safety by focusing on these 905 undervalued stocks based on cash flows where current prices sit well below cash flow based estimates of fair worth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com