Is It Too Late To Consider TotalEnergies After Strong Multi Year Share Price Gains?

- Wondering if TotalEnergies is still good value after a strong multi year run, or if most of the upside is already priced in? This breakdown is designed to give you a clear, no nonsense view.

- The stock has slipped 2.3% over the last week but is still up 0.9% over 30 days, 3.9% year to date and 11.2% over the past year, on top of a 107.9% gain over five years.

- Recent headlines have focused on TotalEnergies doubling down on its integrated energy strategy, from expanding LNG projects and renewables capacity to reshaping its refining and marketing footprint. At the same time, debates around capital returns, buybacks and the energy transition have kept investors closely watching how management allocates cash.

- Right now, Simply Wall St’s valuation checks give TotalEnergies a 5/6 value score, suggesting it screens as undervalued on most of the metrics that matter. Next, we will unpack what that means under different valuation approaches, and later in the article we will look at another way to tie these numbers into a bigger picture view of fair value.

Approach 1: TotalEnergies Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow approach estimates what a business is worth today by projecting the cash it can generate in the future and then discounting those cash flows back to their value in today’s dollars.

For TotalEnergies, the model uses a 2 stage Free Cash Flow to Equity framework, starting from last twelve month free cash flow of about $14.2 billion. Analyst forecasts and Simply Wall St’s own extrapolations then project free cash flow rising to roughly $24.4 billion by 2035, reflecting steady growth over the coming decade as major projects ramp up and cash generation improves.

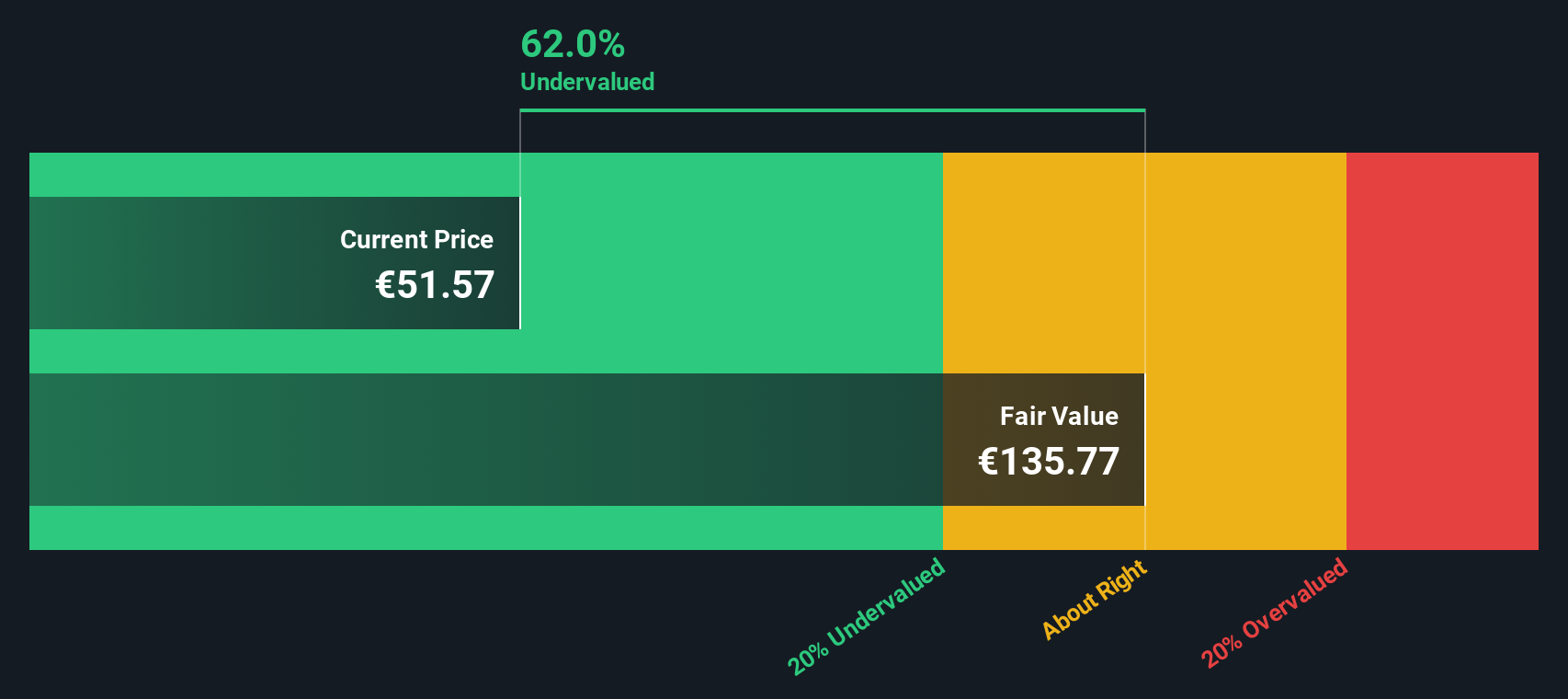

When those future cash flows are discounted back to today and divided by the number of shares, the DCF model points to an intrinsic value of about $181.86 per share. Compared with the current market price in euros, this implies a 69.3% discount. This suggests the market is pricing TotalEnergies well below its modeled long term cash generating potential.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests TotalEnergies is undervalued by 69.3%. Track this in your watchlist or portfolio, or discover 903 more undervalued stocks based on cash flows.

Approach 2: TotalEnergies Price vs Earnings

For a profitable, mature business like TotalEnergies, the price to earnings ratio is a practical way to judge value because it links what investors pay today directly to the company’s current earnings power.

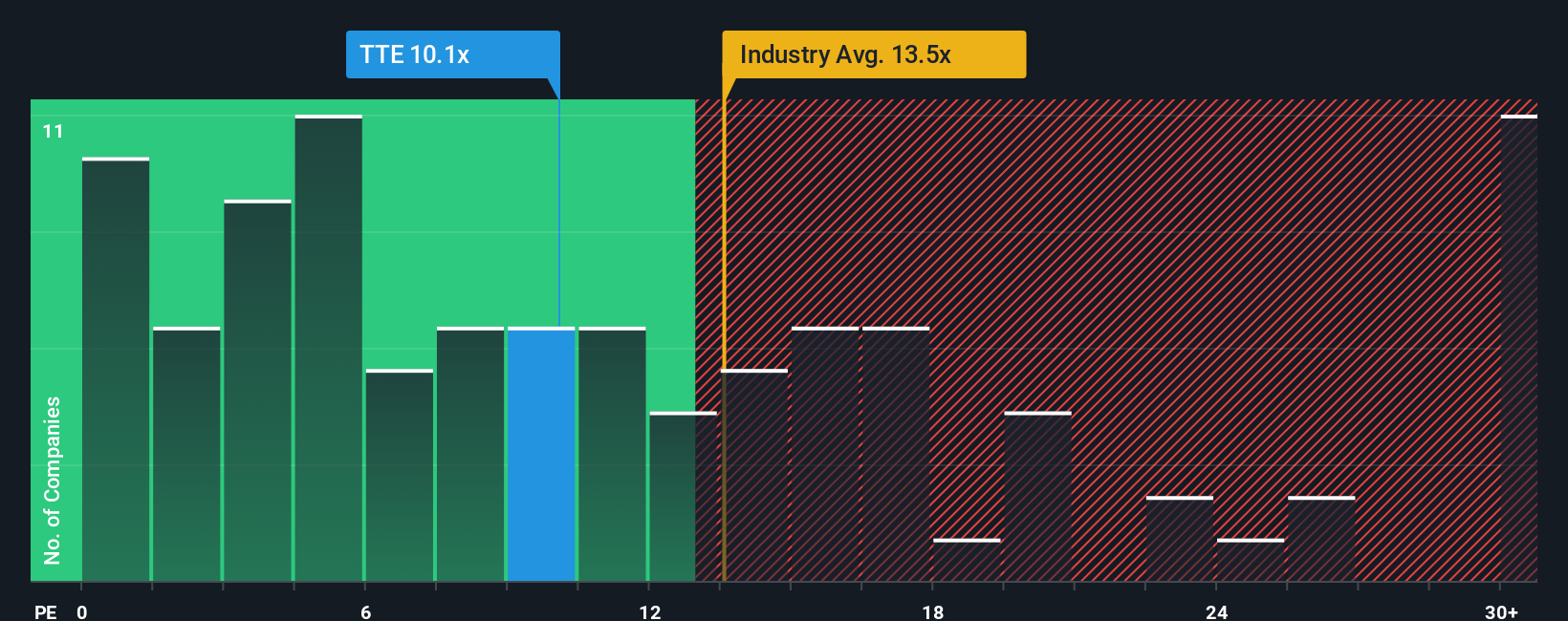

In general, companies with faster, more reliable earnings growth and lower perceived risk tend to command higher PE ratios, while slower growth or higher uncertainty usually warrant a lower multiple. TotalEnergies currently trades at about 10x earnings, which is below both the Oil and Gas industry average of around 13.4x and the broader peer group at roughly 23.1x.

Simply Wall St’s Fair Ratio framework estimates that, given TotalEnergies specific mix of earnings growth, profit margins, industry profile, market cap and risk factors, a more appropriate PE multiple would be closer to 17.7x. This tailored benchmark is more informative than a simple comparison with peers or the sector because it adjusts for the company’s own fundamentals rather than assuming all Oil and Gas stocks deserve the same multiple. On this basis, TotalEnergies current 10x PE suggests the shares remain meaningfully undervalued.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1447 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your TotalEnergies Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. This is a simple but powerful framework on Simply Wall St’s Community page that lets you turn your view of TotalEnergies into a clear story tied to specific revenue, earnings and margin assumptions. These then flow through to a forecast and a fair value you can compare against today’s price to help you decide whether to buy, hold or sell, with the platform dynamically updating those Narratives as new earnings, news and sector data arrive. You can see, for example, how a bullish investor focused on LNG growth and rising margins might justify a fair value near the top of recent targets around €77.57, while a more cautious investor worried about weak oil prices, transition risks and downstream overcapacity might anchor closer to the low end around €52.82. Both can track in real time how fresh information shifts their story, their numbers and ultimately their conviction.

Do you think there's more to the story for TotalEnergies? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com