Labcorp (LH): Reassessing Valuation After Reduced Growth Outlook for Contract Research Unit

Labcorp Holdings (LH) just beat earnings expectations, but the stock is reacting more to management’s cautious tone after cutting revenue growth targets for its contract research unit and trimming its full year outlook.

See our latest analysis for Labcorp Holdings.

At around $264.18 per share, Labcorp’s recent weakness, reflected in a roughly 5 percent 3 month share price return, contrasts with a solid 5 year total shareholder return of about 57 percent. This suggests momentum has cooled as investors reassess growth risks despite a stronger long run record.

If this earnings reaction has you rethinking your healthcare exposure, it could be a good moment to explore other healthcare stocks that might offer a different mix of stability and upside.

With shares trading at a discount to analyst targets yet facing slower growth in a key unit, investors now confront a familiar dilemma: is Labcorp quietly undervalued here, or is the market already bracing for weaker future expansion?

Most Popular Narrative: 11.9% Undervalued

Compared to the last close at $264.18, the most followed narrative sees Labcorp’s fair value higher. This implies the market is discounting its long term potential.

The introduction of innovative tests in oncology, women's health, autoimmune disease, and neurology is anticipated to capture more test volume and outpace growth in the broader market, positively impacting revenue and earnings. The use of AI and technology innovations is enhancing operational efficiencies, improving margins through platforms like eClaim Assist and Labcorp Diagnostic Assistant.

Want to see why steady revenue growth, rising margins, and a richer future earnings multiple still add up to upside from here? The full narrative joins the dots.

Result: Fair Value of $299.71 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, shifting policy and regulatory decisions, including potential PAMA cuts and tougher pricing pressure, could quickly erode the margin gains that analysts are banking on.

Find out about the key risks to this Labcorp Holdings narrative.

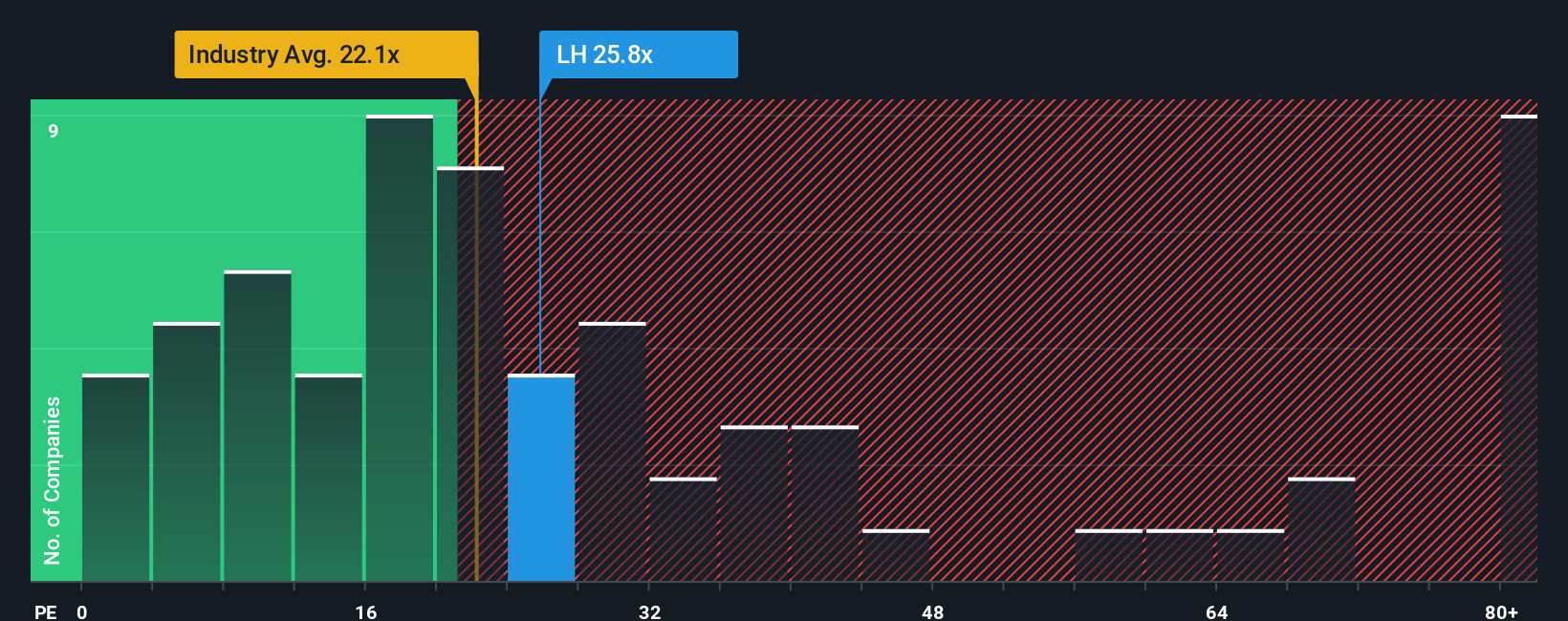

Another View: What Market Ratios Are Saying

There is a catch. On earnings, Labcorp trades at 25.6 times, richer than the broader US healthcare sector at 23.7 times, even if cheaper than close peers at 30.6 times and just under a 27.7 times fair ratio. That mix hints at more execution risk than the DCF style upside suggests. Are investors really being paid enough for that uncertainty?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Labcorp Holdings Narrative

If you see the story differently or simply want to dig into the numbers yourself, you can build a personalized view in minutes: Do it your way.

A great starting point for your Labcorp Holdings research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Ready for more investment ideas?

Before markets move on without you, tap into fresh opportunities using the Simply Wall St Screener, where curated ideas can help you act with confidence and clarity.

- Capture potential mispricings by reviewing these 907 undervalued stocks based on cash flows that pair strong fundamentals with attractive entry points.

- Position ahead of innovation waves by checking out these 26 AI penny stocks at the frontier of intelligent automation and data driven business models.

- Strengthen your passive income strategy by targeting these 13 dividend stocks with yields > 3% that may keep paying you even when markets turn choppy.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com