Did Snowflake’s AI Partnerships and Q3 Results Just Shift Snowflake's (SNOW) Investment Narrative?

- In recent weeks, Snowflake reported third-quarter fiscal 2026 results with revenue of US$1,212.91 million, narrowed losses, and reaffirmed strong free cash flow guidance, while also expanding its AI ecosystem through a US$200 million multi-year Anthropic partnership, a new Accenture Snowflake Business Group, and Collibra joining its Open Semantic Interchange initiative.

- Together, these moves deepen Snowflake’s role as an AI data infrastructure hub, aiming to keep enterprise data, governance, and advanced AI models tightly integrated within a single, cloud-based platform.

- We’ll now explore how the expanded Anthropic partnership and enterprise AI focus influence Snowflake’s existing investment narrative and long-term potential.

These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Snowflake Investment Narrative Recap

To own Snowflake, you need to believe it can stay at the center of enterprise AI and data workloads while scaling toward meaningful profitability. The latest AI partnerships and Q3 results support that thesis but do not materially change the near term tension between strong free cash flow guidance and worries about slowing core product growth and rising competitive pressure.

The expanded US$200 million multi year Anthropic agreement stands out here, because it ties Snowflake’s AI agents and Snowflake Intelligence directly to governed customer data, reinforcing one of the key growth catalysts: deeper AI driven usage on the existing platform, rather than just one off migration spikes.

Yet despite this progress, investors should also be aware that rising competition and pricing pressure from hyperscalers could...

Read the full narrative on Snowflake (it's free!)

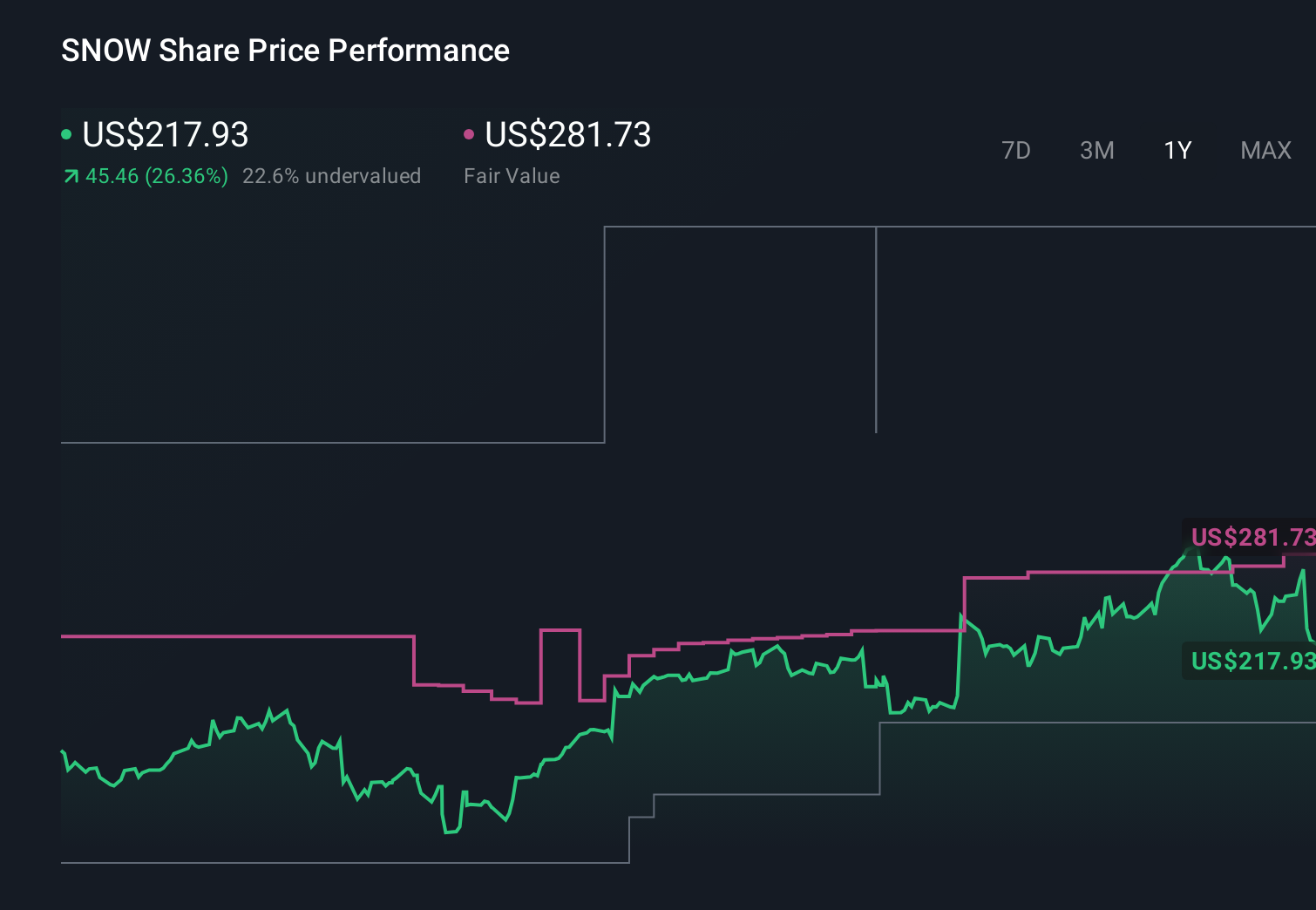

Snowflake's narrative projects $7.8 billion revenue and $497.5 million earnings by 2028. This requires 23.8% yearly revenue growth and an earnings increase of about $1.9 billion from -$1.4 billion today.

Uncover how Snowflake's forecasts yield a $281.73 fair value, a 29% upside to its current price.

Exploring Other Perspectives

Twelve Snowflake fair value estimates from the Simply Wall St Community span roughly US$153 to US$282, showing how differently you can judge the same stock. Against that backdrop, the growing importance of AI driven workloads on Snowflake’s platform could be pivotal for how those expectations around future revenue growth evolve.

Explore 12 other fair value estimates on Snowflake - why the stock might be worth as much as 29% more than the current price!

Build Your Own Snowflake Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Snowflake research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Snowflake research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Snowflake's overall financial health at a glance.

Looking For Alternative Opportunities?

Our top stock finds are flying under the radar-for now. Get in early:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Rare earth metals are the new gold rush. Find out which 37 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com