CommScope (COMM): Evaluating Valuation After a 2,444% Year-to-Date Share Price Rebound

CommScope Holding Company (COMM) has quietly staged a sharp turnaround, with shares up about 2,444% year to date and nearly 1,900% over the past year, catching many investors off guard.

See our latest analysis for CommScope Holding Company.

That surge has cooled a bit recently, with a 7 day share price return of negative 11.77 percent and a 30 day share price return of 7.63 percent. However, the 1 year total shareholder return of 189.89 percent still points to powerful momentum as investors reassess both its growth prospects and its risk profile around 17.77 dollars a share.

If this kind of sharp rebound has your attention, it is a good moment to scan the market for other turnaround style opportunities using our fast growing stocks with high insider ownership.

But after such a dramatic rebound and with the stock still trading below analyst targets, is CommScope a misunderstood value story in recovery, or are markets already pricing in all the meaningful future growth?

Most Popular Narrative: 21.6% Undervalued

With the narrative fair value sitting above the recent 17.77 dollars close, the story hinges on whether CommScope can turn projected upgrades into durable cash flows.

The ongoing rollout of DOCSIS 4.0 amplifiers and next-gen networking products, driven by increased investments from major cable operators, positions CommScope's ANS segment to capitalize on long-term demand for higher-speed broadband and infrastructure upgrades, supporting sustained revenue growth.

Want to see the math behind this optimism? The narrative leans heavily on accelerating top line growth and fatter margins, paired with a rich future earnings multiple. Curious how those moving parts add up to that fair value target and what it assumes about CommScope's next product cycle? Dive in to unpack the full set of projections and pressure test the story for yourself.

Result: Fair Value of $22.67 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that optimism hinges on timely DOCSIS 4.0 rollouts and sustained RUCKUS demand, both of which are vulnerable to slower upgrade cycles and more intense competitive pressure.

Find out about the key risks to this CommScope Holding Company narrative.

Another Lens On Value

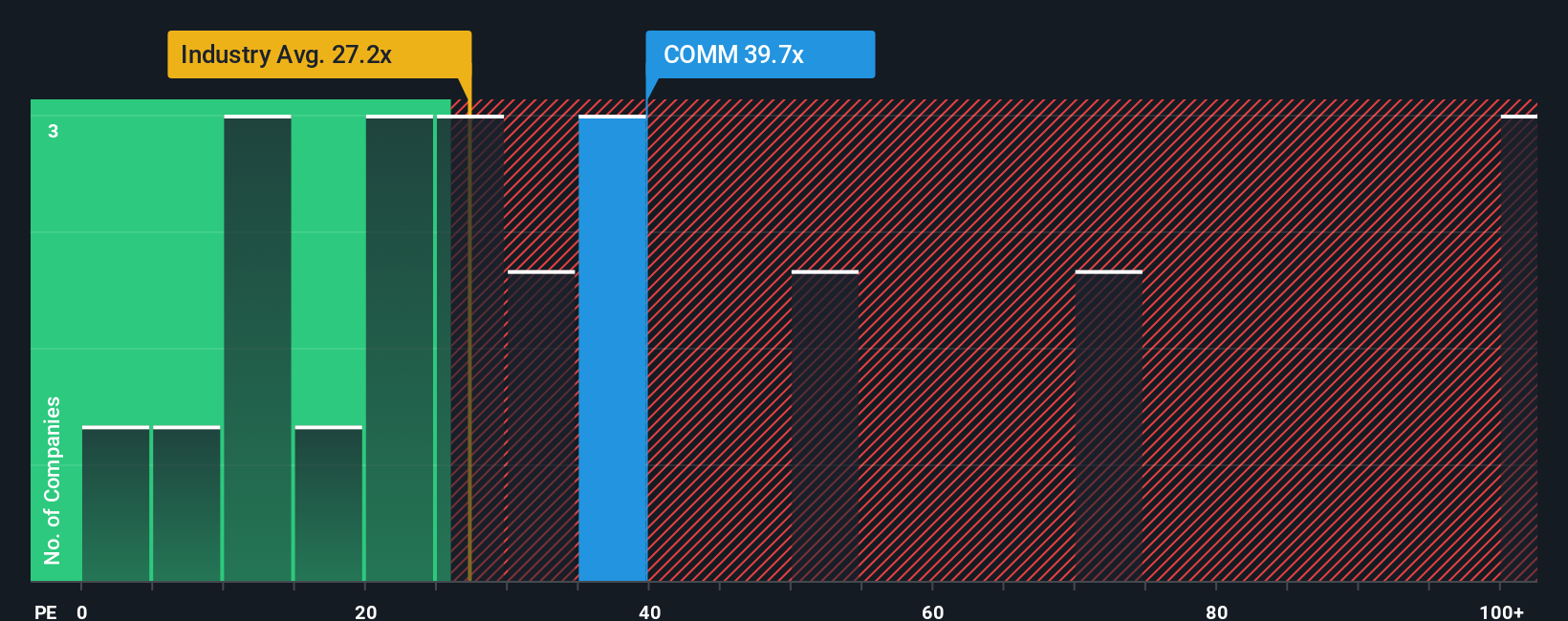

On earnings based measures, the picture is less one sided. CommScope trades on a 13.4 times price to earnings ratio, which looks cheap next to the US communications industry at 31.8 times and peers at 26.6 times, but expensive against its own fair ratio of 4.1 times. That gap hints at either upside if sentiment keeps improving, or painful compression if growth stalls. Which scenario feels more realistic to you?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own CommScope Holding Company Narrative

If you see the story differently or simply prefer to dig into the numbers yourself, you can build a complete view in just minutes: Do it your way.

A great starting point for your CommScope Holding Company research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Do not stop at one turnaround story. Use the Simply Wall Street Screener to quickly surface fresh opportunities before the crowd catches on and prices move away.

- Capture potential mispricings by scanning these 911 undervalued stocks based on cash flows that may offer strong upside based on robust underlying cash flows.

- Ride the next wave of innovation by targeting these 26 AI penny stocks positioned to benefit from accelerating adoption of artificial intelligence.

- Lock in reliable income streams by reviewing these 12 dividend stocks with yields > 3% that combine attractive yields with solid fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com