Advanced Energy Industries (AEIS): Evaluating Valuation After Launch of High-Density NeoPower Module

Advanced Energy Industries (AEIS) just rolled out a new dual output NeoPower module that can deliver up to 16 isolated outputs from a single supply, targeting space constrained industrial, medical, and test systems.

See our latest analysis for Advanced Energy Industries.

Despite a sharp 4.96% one day share price pullback to $204.49, momentum is still firmly intact. A 20.47% 90 day share price return and a 76.63% one year total shareholder return underscore how product launches like NeoPower are contributing to a longer term growth story.

If this kind of power electronics story has your attention, it is worth seeing what else is happening across high growth tech and AI stocks right now for potential next ideas.

Yet with shares already up sharply over the past year and trading not far from analyst targets, investors now face a tougher question: Is Advanced Energy still undervalued, or is the market already discounting years of growth?

Most Popular Narrative Narrative: 9.1% Undervalued

With the most followed narrative putting fair value at about $225 versus the $204.49 close, expectations lean toward more upside if execution holds.

Continuous acceleration in the global adoption of advanced semiconductor manufacturing (including leading-edge logic and memory), combined with the proliferation of digitization and IoT, is leading to strong customer pull for AE's new technology platforms (eVoS, eVerest, NavX). Revenue from these platforms is expected to double in 2025 and ramp further as fabs move to volume production, supporting both future revenue and margin expansion.

Want to see the math behind this optimistic view? The narrative leans on aggressive earnings expansion, richer margins, and a future multiple that assumes durable tech leadership. Curious which assumptions really move that fair value?

Result: Fair Value of $225 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, concentrated hyperscaler exposure and a softer than expected semiconductor capex cycle could quickly compress growth expectations and challenge the 9.1% undervaluation case.

Find out about the key risks to this Advanced Energy Industries narrative.

Another Angle on Valuation

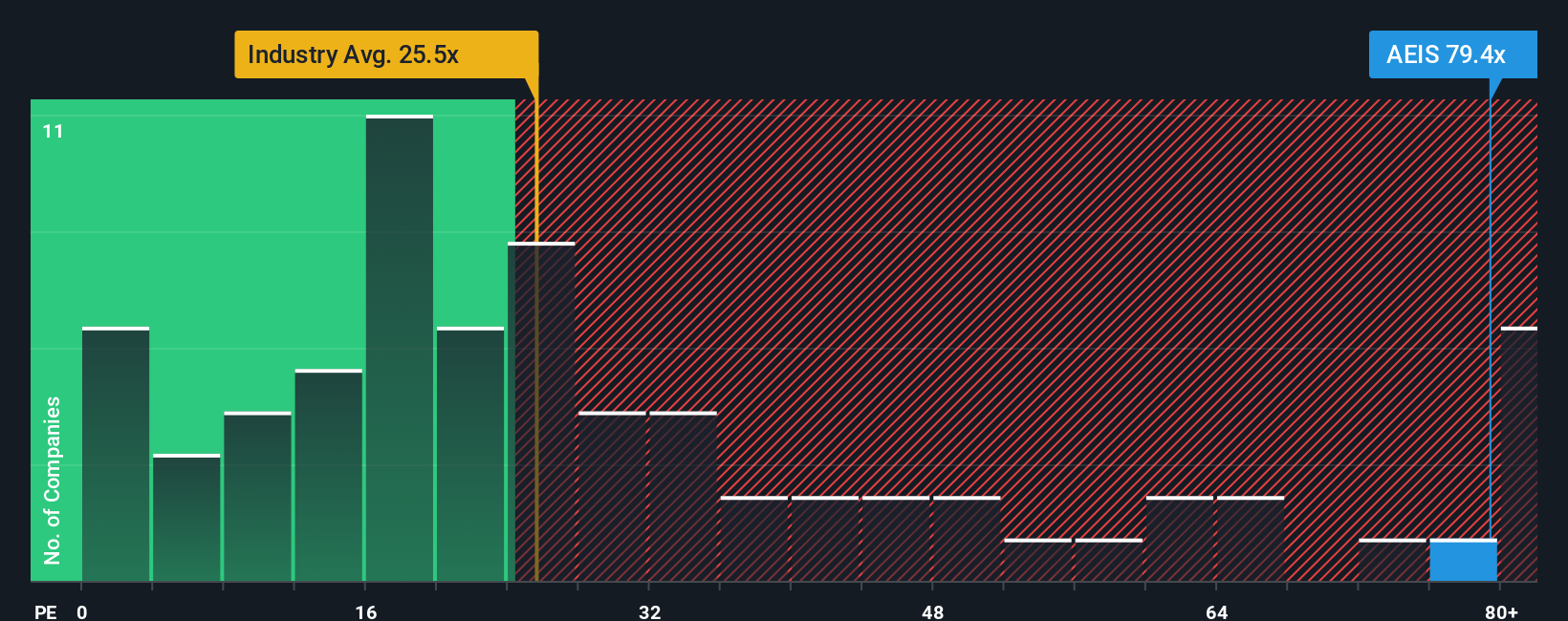

Step back from narratives and the numbers look harsher. At 52.9 times earnings versus an industry 24.3 times and a fair ratio of 38.2 times, the shares screen as expensive. If sentiment cools, how much multiple compression are you really comfortable riding out?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Advanced Energy Industries Narrative

If you rely on your own analysis and prefer the numbers to tell your story, you can build a custom view in minutes, starting with Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Advanced Energy Industries.

Looking for more investment ideas?

Before momentum shifts again, make your next move count by scanning targeted opportunities on Simply Wall Street that match your strategy instead of letting them pass you by.

- Capture potential mispricings by scanning these 910 undervalued stocks based on cash flows that may be trading below their long term cash flow potential.

- Tap into structural growth trends by reviewing these 29 healthcare AI stocks transforming diagnostics, hospital workflows, and patient outcomes.

- Boost your income game by targeting these 13 dividend stocks with yields > 3% that can help anchor total returns with reliable payouts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com