LPL Financial (LPLA): Assessing Valuation After Strong Multi‑Year Gains and Recent Share Price Pause

LPL Financial Holdings (LPLA) has quietly held its ground, with the stock roughly flat over the past month after a strong run in the past 3 years and 5 years.

See our latest analysis for LPL Financial Holdings.

Zooming out, that recent wobble at a share price of $355.72 comes after a solid year to date share price return of 8.45 percent and an even stronger multi year total shareholder return. This suggests momentum is cooling but not broken as investors reassess growth and risk.

If LPL’s long run gains have you thinking about what else could compound from here, it is a good moment to explore fast growing stocks with high insider ownership.

With double digit earnings growth and a share price sitting modestly below analyst targets, is LPL Financial still trading at a discount, or has the market already priced in the next leg of its expansion?

Most Popular Narrative Narrative: 20.7% Undervalued

Against a last close of $355.72, the most followed narrative implies fair value closer to the mid $400s, framing LPL as a discounted compounder.

The analysts have a consensus price target of $453.417 for LPL Financial Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $504.0, and the most bearish reporting a price target of just $400.0.

Curious why a mature wealth platform is being modeled with growth and margins more often seen in high growth tech names, and a richer future earnings multiple? The narrative leans on ambitious revenue compounding, steady margin expansion, and a punchy valuation multiple to bridge today’s price to that higher fair value. Want to see exactly how those moving parts stack up and which assumptions do the real heavy lifting?

Result: Fair Value of $448.33 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that upside assumes benign conditions, while a sharp drop in interest rates or messy acquisition integrations could quickly undermine the bullish margin story.

Find out about the key risks to this LPL Financial Holdings narrative.

Another Take On Valuation

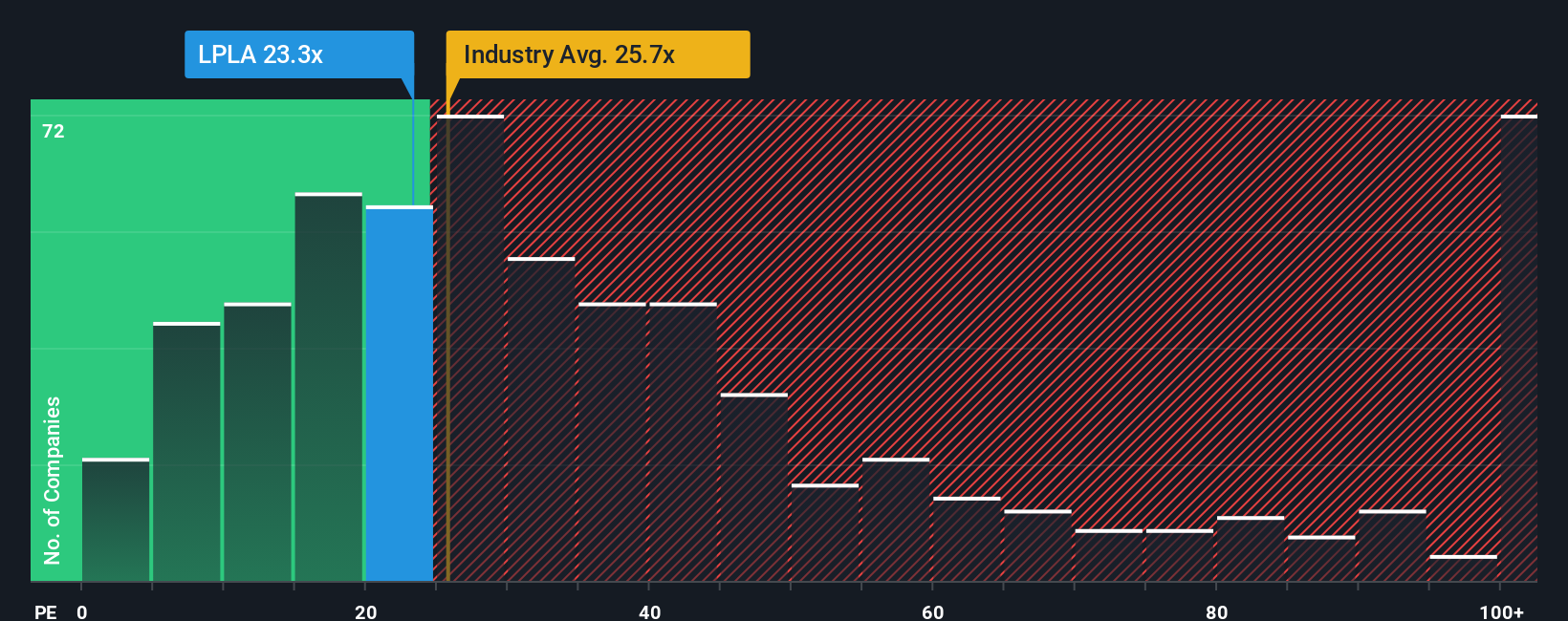

Analysts see upside, but on earnings multiples LPL looks stretched. The current P/E of 34.2 times sits well above both peers at 19.2 times and a fair ratio of 21 times, suggesting expectations are high and leaving less room for error if growth stumbles.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own LPL Financial Holdings Narrative

If you see the story differently or would rather dive into the numbers yourself, you can craft a fresh narrative in just a few minutes: Do it your way.

A great starting point for your LPL Financial Holdings research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before you move on, give yourself an edge by lining up your next opportunity with a few targeted stock ideas from the Simply Wall St Screener.

- Capitalize on mispriced opportunities by checking out these 909 undervalued stocks based on cash flows that the market may be overlooking today but cash flows suggest deserve a closer look.

- Ride powerful technology shifts by scanning these 26 AI penny stocks positioned to benefit from the adoption of machine learning and automation across industries.

- Strengthen your income foundation by reviewing these 13 dividend stocks with yields > 3% that may help boost portfolio yields while still maintaining quality fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com