These 4 Measures Indicate That Kaisa Capital Investment Holdings (HKG:936) Is Using Debt Extensively

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Kaisa Capital Investment Holdings Limited (HKG:936) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does Kaisa Capital Investment Holdings Carry?

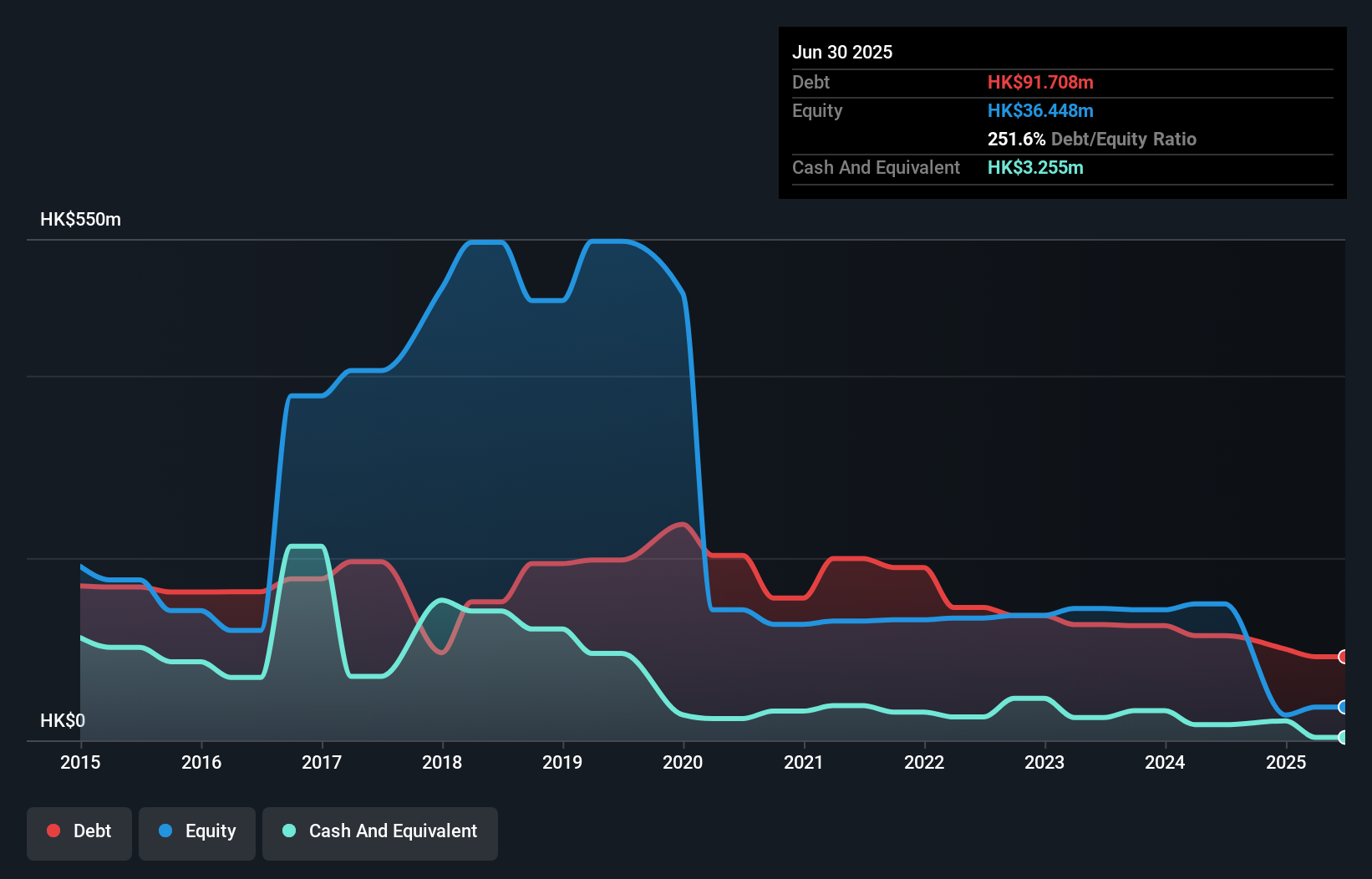

You can click the graphic below for the historical numbers, but it shows that Kaisa Capital Investment Holdings had HK$91.7m of debt in June 2025, down from HK$114.8m, one year before. On the flip side, it has HK$3.26m in cash leading to net debt of about HK$88.5m.

A Look At Kaisa Capital Investment Holdings' Liabilities

We can see from the most recent balance sheet that Kaisa Capital Investment Holdings had liabilities of HK$363.3m falling due within a year, and liabilities of HK$89.5m due beyond that. On the other hand, it had cash of HK$3.26m and HK$63.6m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by HK$386.0m.

This deficit is considerable relative to its market capitalization of HK$402.8m, so it does suggest shareholders should keep an eye on Kaisa Capital Investment Holdings' use of debt. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

Check out our latest analysis for Kaisa Capital Investment Holdings

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Even though Kaisa Capital Investment Holdings's debt is only 2.4, its interest cover is really very low at 0.35. The main reason for this is that it has such high depreciation and amortisation. These charges may be non-cash, so they could be excluded when it comes to paying down debt. But the accounting charges are there for a reason -- some assets are seen to be losing value. In any case, it's safe to say the company has meaningful debt. Shareholders should be aware that Kaisa Capital Investment Holdings's EBIT was down 82% last year. If that decline continues then paying off debt will be harder than selling foie gras at a vegan convention. When analysing debt levels, the balance sheet is the obvious place to start. But it is Kaisa Capital Investment Holdings's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, Kaisa Capital Investment Holdings actually produced more free cash flow than EBIT. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

On the face of it, Kaisa Capital Investment Holdings's interest cover left us tentative about the stock, and its EBIT growth rate was no more enticing than the one empty restaurant on the busiest night of the year. But on the bright side, its conversion of EBIT to free cash flow is a good sign, and makes us more optimistic. Overall, we think it's fair to say that Kaisa Capital Investment Holdings has enough debt that there are some real risks around the balance sheet. If all goes well, that should boost returns, but on the flip side, the risk of permanent capital loss is elevated by the debt. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. These risks can be hard to spot. Every company has them, and we've spotted 4 warning signs for Kaisa Capital Investment Holdings (of which 2 are potentially serious!) you should know about.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.