Is ConocoPhillips a Value Opportunity After Choppy 2025 Trading and DCF Upside?

- If you are wondering whether ConocoPhillips is quietly turning into a value opportunity or if the market has already priced it efficiently, you are in the right place.

- The stock has been choppy lately, slipping 4.4% over the last week, edging up 3.1% over 30 days, and still sitting slightly down year to date at 7.6%, even though the 5-year return stands at a substantial 180.2%.

- These moves are unfolding against a backdrop of shifting oil price expectations, strategic capital allocation updates, and ongoing debate about how traditional energy majors fit into a lower-carbon future. Together, these narratives are reshaping how investors think about both the upside potential and the risk profile for ConocoPhillips.

- On our framework, ConocoPhillips scores a solid 5/6 valuation checks, suggesting the market might be leaving some value on the table. Next, we will walk through the main valuation methods investors use and then finish with a more detailed way to connect those numbers to the longer-term story.

Find out why ConocoPhillips's 0.5% return over the last year is lagging behind its peers.

Approach 1: ConocoPhillips Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth by projecting its future cash flows and then discounting them back to today in dollar terms. For ConocoPhillips, the latest twelve month Free Cash Flow sits at about $7.9 billion, forming the starting point for this 2 Stage Free Cash Flow to Equity model.

Analysts provide detailed forecasts for the next few years, with Simply Wall St then extrapolating those estimates out over a 10 year horizon. Under this framework, ConocoPhillips free cash flow is projected to climb to around $14.4 billion by 2035, implying steady growth as new projects come online and existing assets mature.

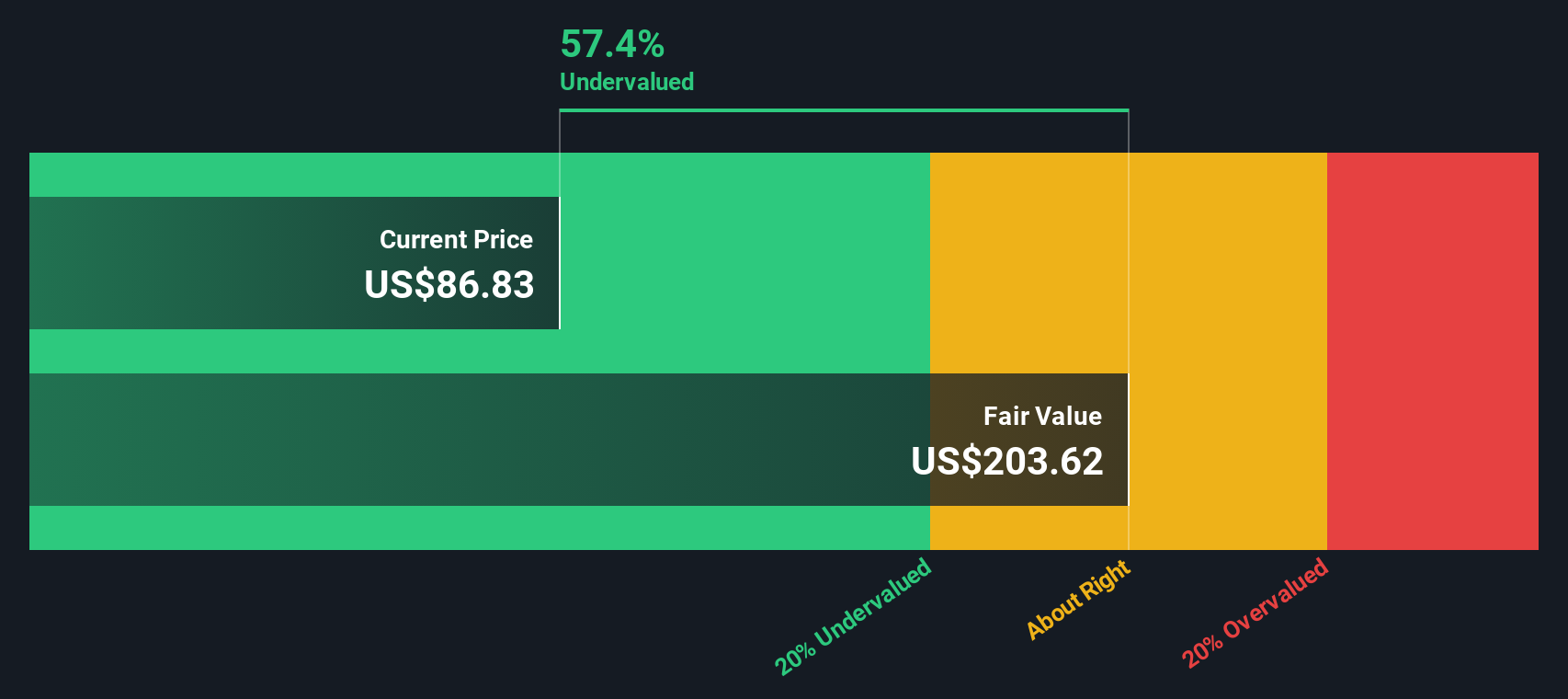

When all those projected cash flows are discounted back to today, the model arrives at an estimated intrinsic value of roughly $227.22 per share. Compared with the current share price, this implies the stock is about 59.3% undervalued, suggesting the market is pricing in a far more pessimistic future than the cash flow outlook currently supports.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests ConocoPhillips is undervalued by 59.3%. Track this in your watchlist or portfolio, or discover 916 more undervalued stocks based on cash flows.

Approach 2: ConocoPhillips Price vs Earnings

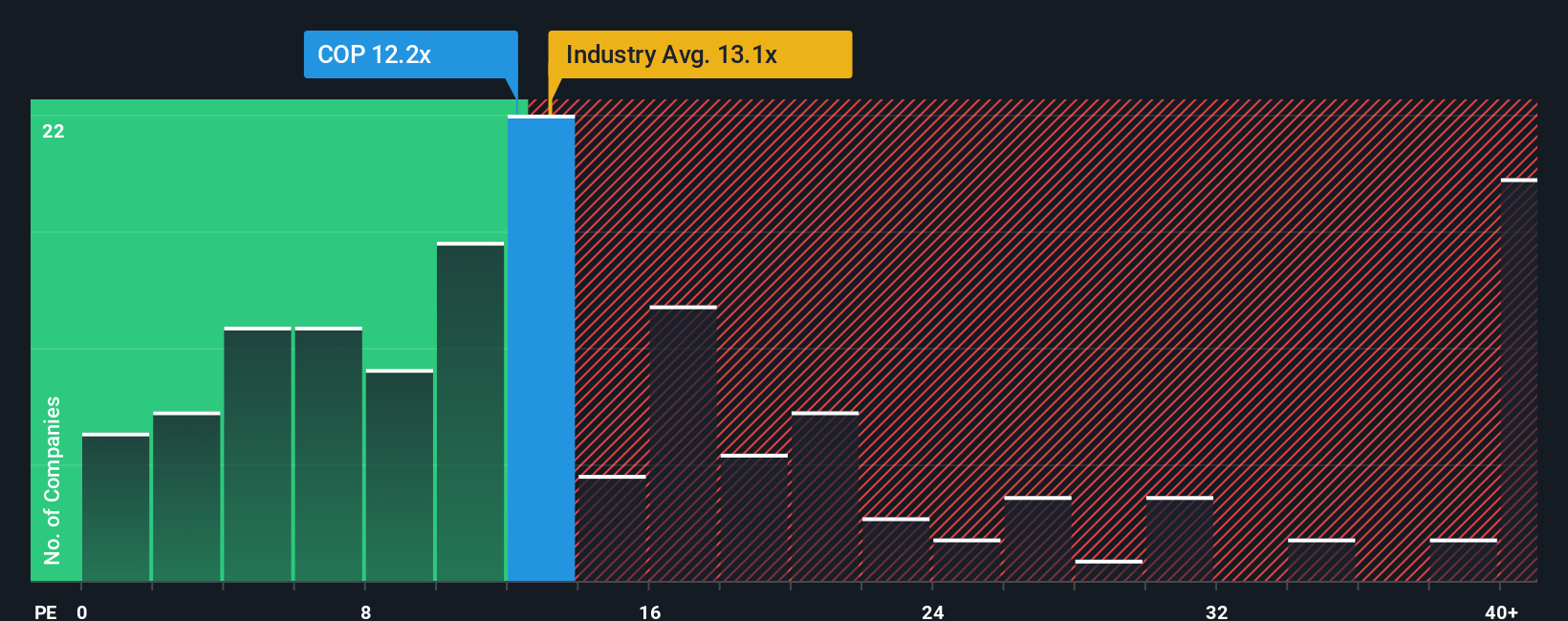

For a mature, consistently profitable producer like ConocoPhillips, the Price to Earnings (PE) ratio is a practical way to gauge how much investors are willing to pay for each dollar of current earnings. In general, faster growth and lower perceived risk justify a higher PE, while slower growth or higher volatility usually mean a lower, more conservative multiple is appropriate.

ConocoPhillips currently trades on a PE of about 12.9x. That sits slightly below the broader Oil and Gas industry average of around 13.1x and a bit above the selected peer group at roughly 11.8x, which implies the market is applying a fairly standard valuation for a large cap energy name. Simply Wall St goes a step further by estimating a “Fair Ratio” of 20.7x, a proprietary measure of what PE might be justified once factors like earnings growth, profitability, risk profile, industry positioning and market cap are all considered together. This can be more informative than a simple peer or industry comparison, which may miss company specific strengths or risks. Comparing the current 12.9x PE to the 20.7x Fair Ratio suggests the shares still trade at a meaningful discount relative to their fundamentals.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1456 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your ConocoPhillips Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple tool on Simply Wall St’s Community page that lets you spell out your story for ConocoPhillips. You can link that story to your assumptions for future revenue, earnings and margins, and automatically turn those into a fair value you can compare against today’s price to help you decide whether to buy, hold or sell. The Narrative then updates dynamically as new information like earnings or oil market news comes in. For example, a bullish investor who thinks LNG projects ramp smoothly, margins expand and the stock deserves something near the most optimistic fair values on the platform will naturally land closer to the high end of current COP estimates. A more cautious investor, worried about project delays, lower long term oil prices and energy transition risk, might anchor near the low end of fair values. Both can clearly see how their different stories drive different forecasts and price targets.

Do you think there's more to the story for ConocoPhillips? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com