Is Cohen & Steers Stock Price Slide in 2025 Signalling a Potential Opportunity?

- If you are wondering whether Cohen & Steers at around $63 a share is a bargain or a value trap, you are not alone. That is exactly what we are going to unpack today.

- The stock has bounced about 0.6% over the last week and 6.3% over the past month, but those moves follow a much steeper slide of 31.1% year to date and 28.2% over the last year.

- This level of volatility has put Cohen & Steers back on some value investors radars as they reassess whether institutional demand for listed real assets and income strategies can support a recovery. At the same time, questions around interest rates, capital flows into funds, and the broader diversified financials space are shaping how the market prices the company today.

- Based on our checks, Cohen & Steers currently scores just 1 out of 6 for being undervalued. This might sound underwhelming until you see how different valuation approaches frame the opportunity, and we will finish by looking at a more complete way to think about its worth beyond simple multiples.

Cohen & Steers scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Cohen & Steers Excess Returns Analysis

The Excess Returns model looks at how effectively Cohen & Steers turns its equity base into profits above the return that investors require. Instead of focusing on near term earnings swings, it asks whether the firm can consistently earn more than its cost of equity over time.

For Cohen & Steers, the model starts with a Book Value of $10.79 per share and a Stable EPS of $2.35 per share, based on the median return on equity over the past 5 years. That history translates into an Average Return on Equity of 30.34%, versus a Cost of Equity of $0.63 per share. The difference between those two, an Excess Return of $1.72 per share, is what drives long run value creation, anchored by a Stable Book Value estimate of $7.76 per share from past data.

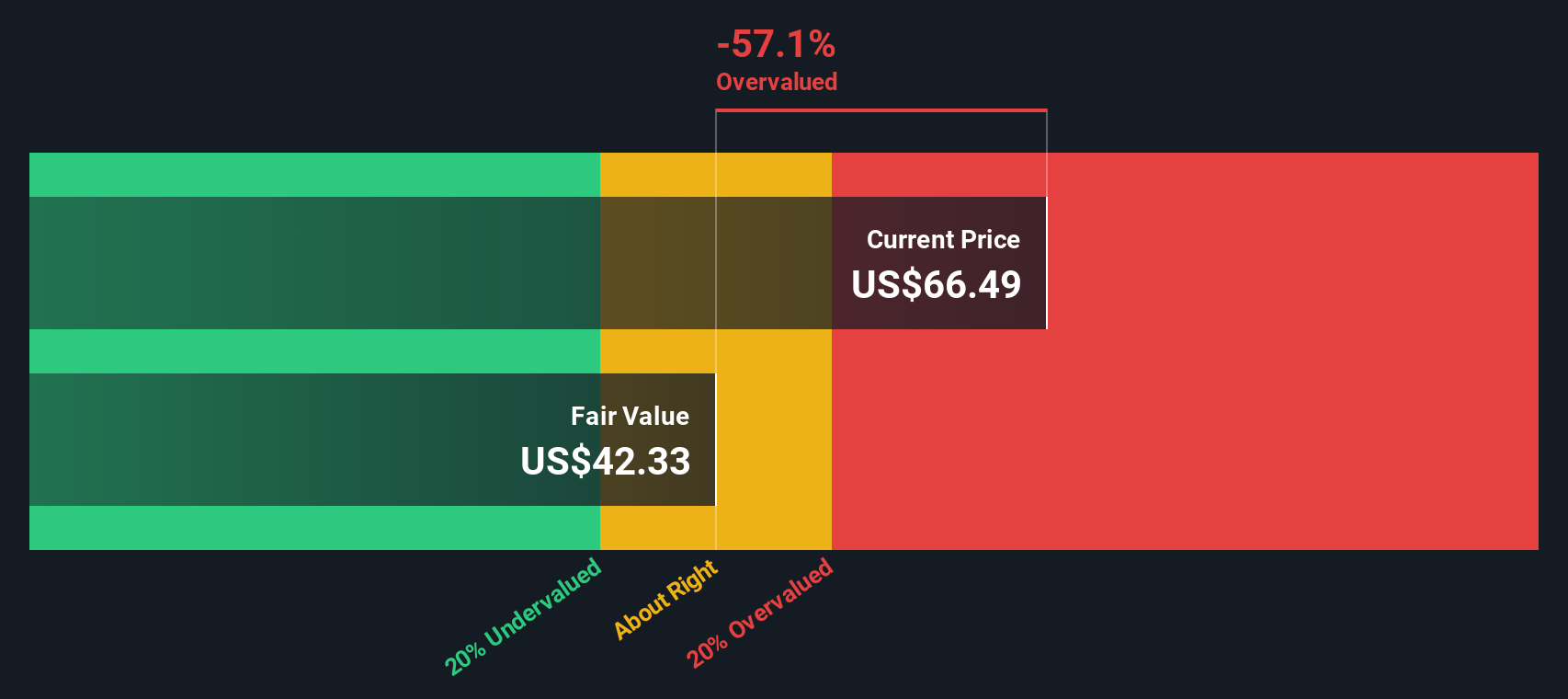

Combining these inputs, the Excess Returns valuation implies an intrinsic value of about $42.80 per share, indicating the stock is roughly 47.2% overvalued compared with the current market price. In this framework, investors are paying well ahead of the company’s projected economic value add.

Result: OVERVALUED

Our Excess Returns analysis suggests Cohen & Steers may be overvalued by 47.2%. Discover 918 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Cohen & Steers Price vs Earnings

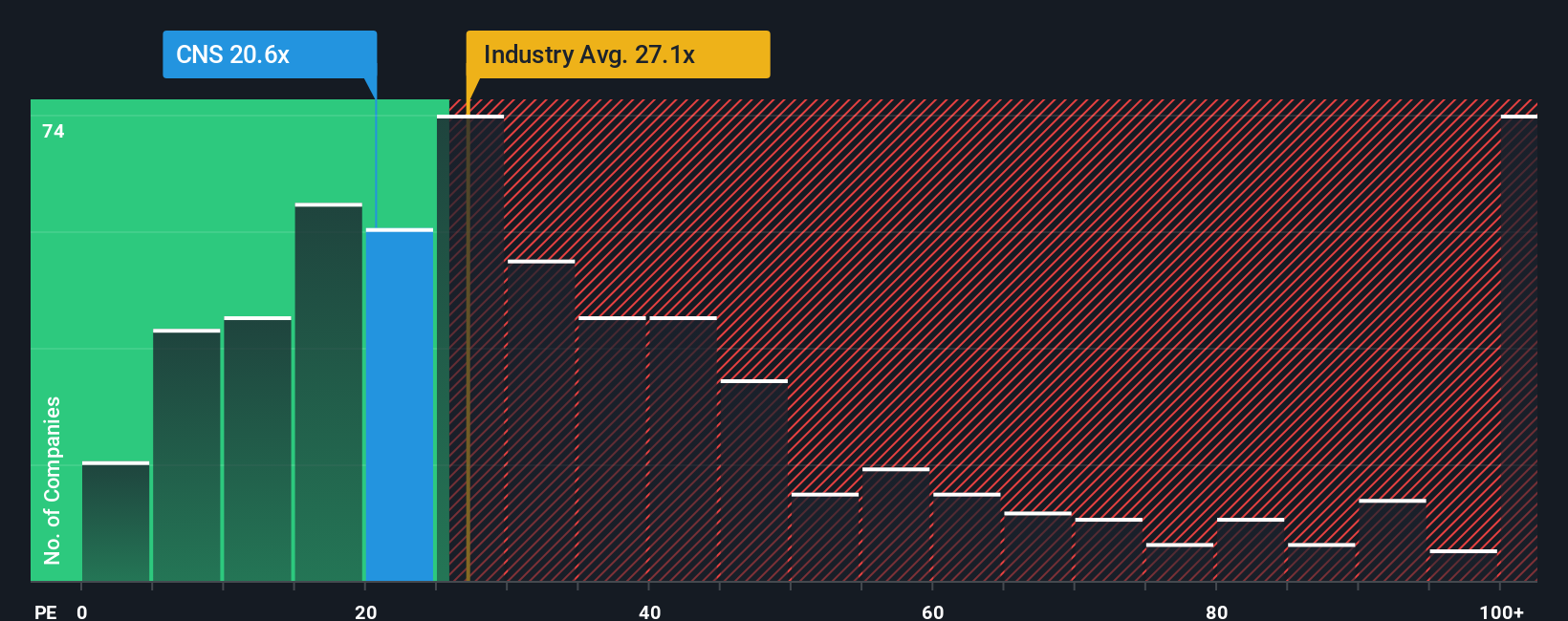

For a consistently profitable business like Cohen & Steers, the price to earnings, or PE, ratio is a useful yardstick because it links what investors are paying directly to the company’s current earnings power. In general, faster growth and lower perceived risk justify a higher “normal” PE, while slower growth, cyclicality, or elevated risks usually mean the market will only pay a lower multiple.

Cohen & Steers currently trades at about 19.6x earnings. That sits below the broader Capital Markets industry average of roughly 25.3x, but above the peer group average of around 13.0x, suggesting investors are already ascribing a quality and growth premium versus direct comparables. To refine this view, Simply Wall St’s proprietary Fair Ratio framework estimates what PE multiple the stock deserves based on its growth outlook, profitability, risk profile, industry, and size.

On this basis, Cohen & Steers’ Fair Ratio is 15.0x, meaning the shares trade at a noticeable premium to what those fundamentals would typically support. While industry and peer comparisons are helpful, the Fair Ratio is more tailored, and it points to the stock being somewhat expensive at current levels.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1460 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Cohen & Steers Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, an easy tool on Simply Wall St’s Community page that lets you spell out your story for a company, link that story to a set of revenue, earnings and margin forecasts, and translate those forecasts into a Fair Value you can compare against today’s price to decide whether to buy, hold or sell. Your Narrative automatically updates as new news or earnings arrive. For Cohen & Steers, one investor might build a Narrative around strong long term AUM growth from active ETFs, recovering real estate and global distribution, and arrive at a Fair Value near the most bullish 80 dollars target. Another, more cautious investor might emphasize fee pressure, passive competition and concentration risks, and land closer to the 66 dollars bearish target. Both can clearly see how their assumptions drive their valuation and how the gap between Fair Value and price changes over time.

Do you think there's more to the story for Cohen & Steers? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com