Reassessing Aris Mining (TSX:ARIS) After a Tripling Share Price: Is Further Upside Still Justified?

Aris Mining (TSX:ARIS) has quietly become one of the stronger performers on the TSX this year, with the stock up over 3x year to date as investors reassess its growth story.

See our latest analysis for Aris Mining.

That surge has been backed by a powerful 317% year to date share price return and a 339% one year total shareholder return, with the latest move higher suggesting bullish momentum is still building at around CA$21.96.

If Aris’s run has you rethinking where growth and risk are shifting, this could be a good moment to explore fast growing stocks with high insider ownership for other fast moving opportunities.

With shares surging and analysts still seeing upside to their price targets, the real question now is whether Aris Mining remains misunderstood value, or if the market is already pricing in its next leg of growth?

Most Popular Narrative Narrative: 21.9% Undervalued

With Aris Mining last closing at CA$21.96 against a narrative fair value of CA$28.13, the story points to meaningful upside driven by future cash flows.

Analysts are assuming Aris Mining's revenue will grow by 32.4% annually over the next 3 years.

Analysts assume that profit margins will increase from 0.8% today to 46.3% in 3 years time.

Curious how a modestly lower discount rate, sharply higher margins, and rapid top line growth can justify this jump in value? The full narrative unpacks the aggressive earnings ramp and the leaner future multiple that need to come together for that fair value to hold.

Result: Fair Value of CA$28.13 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, execution setbacks at Segovia or Marmato, or a sustained pullback in gold prices, could quickly erode the growth and margin assumptions underpinning this valuation.

Find out about the key risks to this Aris Mining narrative.

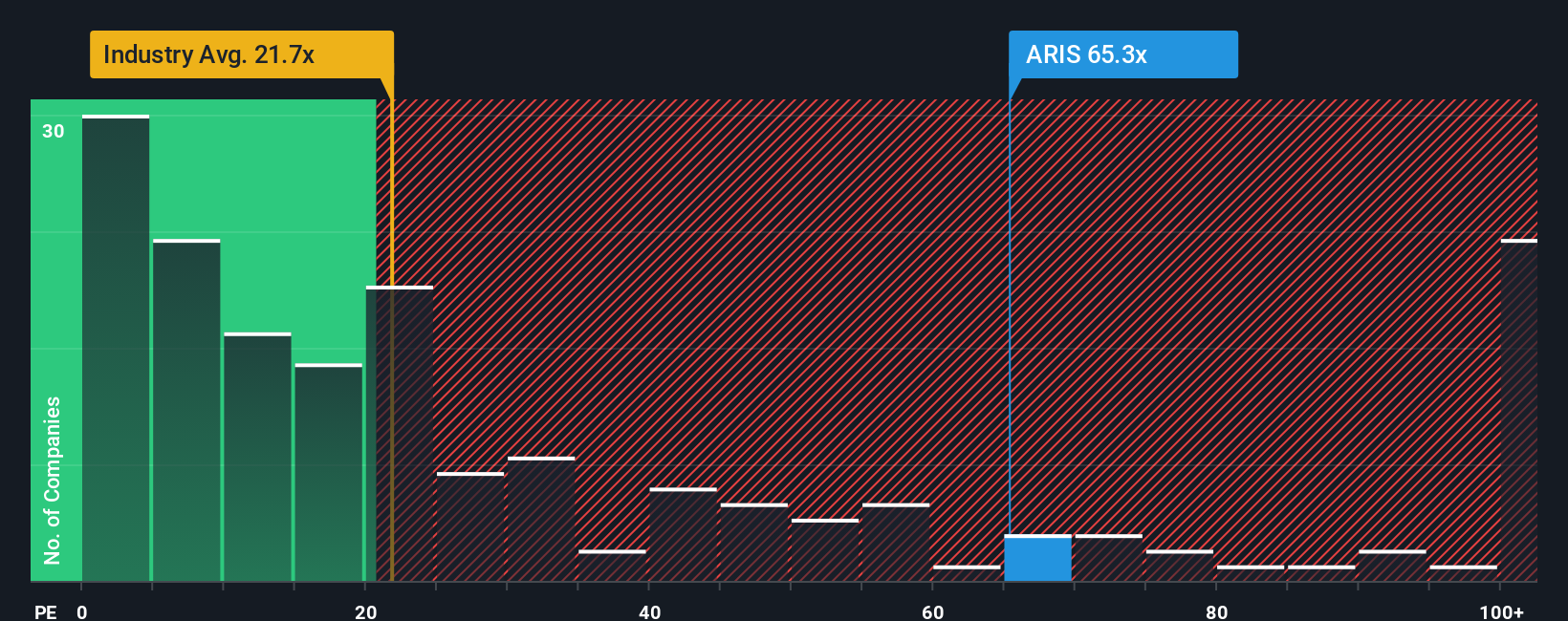

Another Angle, Lofty Multiple

That 21.9% narrative upside sits awkwardly beside the current price to earnings of 65.1 times, far richer than the Canadian metals and mining industry at 20.9 times and peers at 6.4 times, and even above a 52.4 times fair ratio the market could drift back toward if expectations cool.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Aris Mining Narrative

If you prefer to stress test these assumptions yourself and put your own spin on the outlook, you can build a complete narrative in just a few minutes: Do it your way.

A great starting point for your Aris Mining research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Ready for your next investing move?

Aris might be on a tear, but you could miss other opportunities if you stop here. Let the Simply Wall Street Screener surface your next potential advantage.

- Explore potential mispricings by targeting companies our models flag as undervalued through these 916 undervalued stocks based on cash flows, before the wider market catches on.

- Focus on powerful secular trends by looking at innovators transforming industries with these 25 AI penny stocks.

- Strengthen your income stream by concentrating on reliable payers using these 13 dividend stocks with yields > 3%, so your portfolio can better align with your income objectives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com