Assessing Aktia Pankki (HLSE:AKTIA)’s Valuation After a 40% One-Year Share Price Climb

Aktia Pankki Oyj (HLSE:AKTIA) has quietly pushed higher, with the share price up about 12% over the past month and more than 40% over the past year, catching many Finland bank investors’ attention.

See our latest analysis for Aktia Pankki Oyj.

That steady 11.40% 1 month share price return and 41.38% 1 year total shareholder return suggest momentum is still building, as investors warm to Aktia’s earnings resilience, modest growth and income profile at the current €11.92 share price.

If Aktia’s move has you rethinking your watchlist, this could be a good moment to broaden your search and discover fast growing stocks with high insider ownership.

With shares hovering near analysts’ price targets after a strong run and solid but modest growth, investors now face a key question: Is Aktia still undervalued, or is the market already pricing in its future earnings power?

Price-to-Earnings of 14.5x: Is it justified?

Aktia Pankki Oyj trades on a price-to-earnings ratio of 14.5x at the last close of €11.92, which makes the stock look modestly valued versus the broader Finnish market but relatively expensive against bank peers.

The price-to-earnings multiple compares the current share price with the company’s earnings, helping investors judge how much they are paying for each euro of profit. For a bank like Aktia, with steady but unspectacular expected revenue growth of around 2.3% per year and a Return on Equity that is currently low at 8% and only forecast to reach 12.2% in three years, this multiple indicates that the market is already assigning a reasonable value to its earnings power rather than a deep discount.

However, context matters. While Aktia’s 14.5x ratio is below the Finnish market average of 18.8x, it stands well above both the European Banks industry average of 10.7x and the peer average of 10.8x, showing investors are paying a meaningful premium for its earnings compared to similar banks.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Earnings of 14.5x (OVERVALUED)

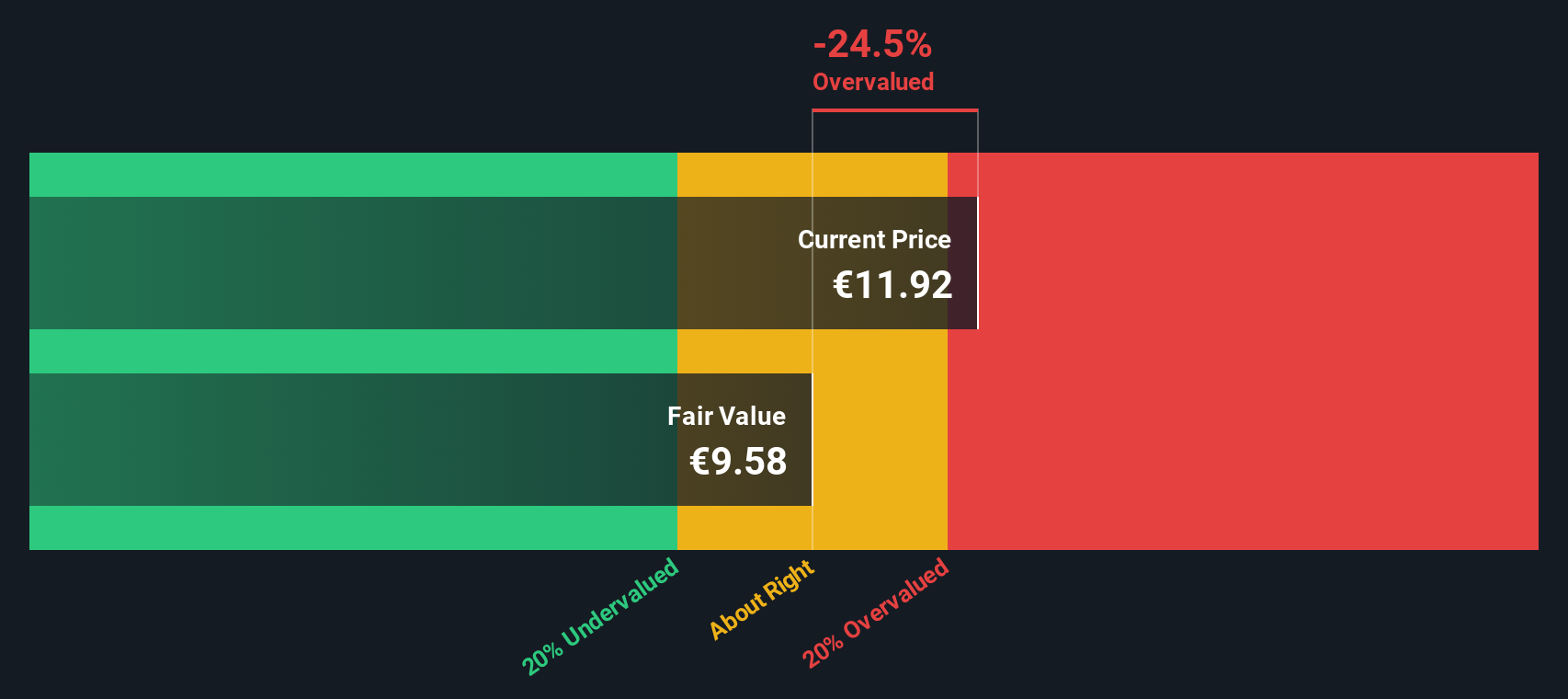

Our DCF model estimates a fair value of €9.58 per share for Aktia, compared to the current €11.92 price, indicating the stock is trading above intrinsic value.

The SWS DCF model projects the company’s future cash flows and discounts them back to today, using assumptions around growth, profitability and required returns to estimate what the business is worth now. For a mature, slow growing bank with modest 5.8% annual earnings growth over five years, negative earnings growth in the last year and forecast revenue growth below both 20% and the Finnish market, this framework suggests that today’s price bakes in more optimism than the cash flow outlook alone supports.

Look into how the SWS DCF model arrives at its fair value.

However, investors should still watch for weaker than expected revenue growth or a downturn in Finland’s economy, which could pressure margins and loan quality.

Find out about the key risks to this Aktia Pankki Oyj narrative.

Another View on Value

Our DCF model paints a cooler picture than the earnings multiple. With fair value estimated at €9.58 per share against the €11.92 market price, Aktia screens as overvalued on cash flows, not just on peer comparisons. Could recent share price momentum be running ahead of fundamentals?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Aktia Pankki Oyj for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 914 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Aktia Pankki Oyj Narrative

If our view does not fully align with yours, or you would rather dig into the numbers yourself, you can quickly build a personalised thesis in under three minutes: Do it your way.

A great starting point for your Aktia Pankki Oyj research is our analysis highlighting 1 key reward and 5 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before you move on, secure your next opportunity with the Simply Wall Street Screener, where focused stock lists turn scattered ideas into clear, actionable strategies.

- Capitalize on rapid innovation by targeting these 25 AI penny stocks that are redefining entire industries with intelligent automation and data driven products.

- Lock in potential income streams by filtering for these 13 dividend stocks with yields > 3% that can strengthen your portfolio’s yield profile.

- Catch mispriced opportunities early by scanning these 914 undervalued stocks based on cash flows where share prices have yet to reflect long term cash flow potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com