Has Nasdaq’s Strong 2025 Rally Already Fully Reflected Its Growth Prospects?

- If you are wondering whether Nasdaq is still attractive after such a strong run, or if the upside has already been priced in, this article will walk you through what the numbers say about its value.

- Nasdaq's share price has climbed to around $95.36, delivering roughly 1.9% over the last week, 10.9% over the last month, and 23.2% year to date, with 24.2% over 1 year, 62.4% over 3 years, and 138.1% over 5 years.

- Behind those gains, Nasdaq has stayed in the spotlight as a crucial infrastructure player in global markets, from trading platforms to regulatory technology and index licensing. Recent headlines have focused on its push deeper into technology and data solutions, as exchanges evolve from simple trading venues into full stack financial services platforms.

- Despite that momentum, Nasdaq currently scores just 0 out of 6 on our undervaluation checks. In the sections that follow, we will unpack what different valuation methods are saying about that score, then circle back to a broader way to think about Nasdaq's value by the end of the article.

Nasdaq scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Nasdaq Excess Returns Analysis

The Excess Returns model looks at how much profit a company can generate above the minimum return shareholders demand on their equity, then capitalizes those surplus profits into an intrinsic value per share.

For Nasdaq, the starting point is its Book Value of $20.99 per share and a Stable EPS of $4.10 per share, based on weighted future return on equity estimates from 4 analysts. With an Average Return on Equity of 17.70% and a Cost of Equity of $1.97 per share, the company is expected to earn an Excess Return of $2.13 per share on its equity base.

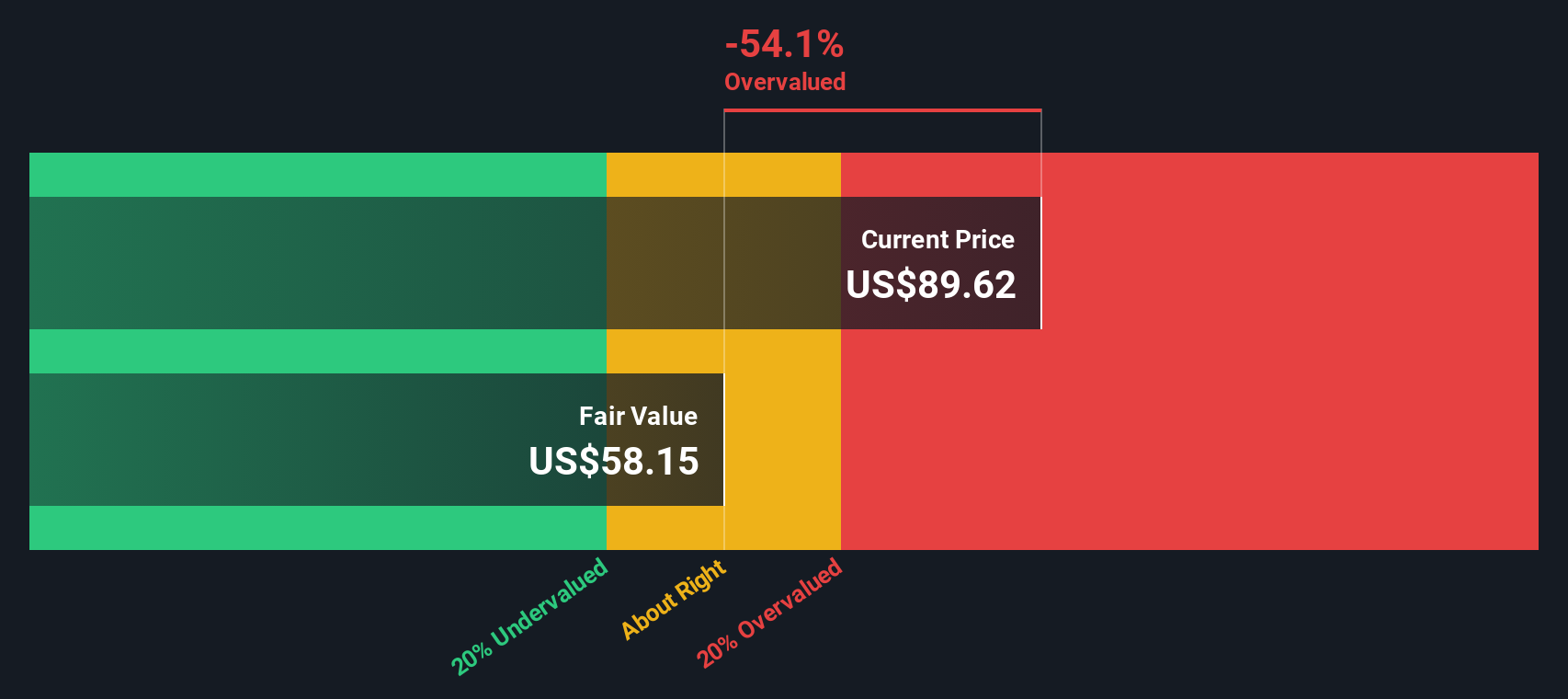

Analysts also see Stable Book Value rising to $23.15 per share, supported by projections from 3 analysts. When these excess returns are projected forward and discounted, the model arrives at an intrinsic value of about $63.63 per share for Nasdaq, implying the stock is roughly 49.9% overvalued versus the current price near $95.

This framework suggests that even if Nasdaq continues to earn solid returns on equity, today’s price already reflects a very optimistic trajectory.

Result: OVERVALUED

Our Excess Returns analysis suggests Nasdaq may be overvalued by 49.9%. Discover 910 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Nasdaq Price vs Earnings

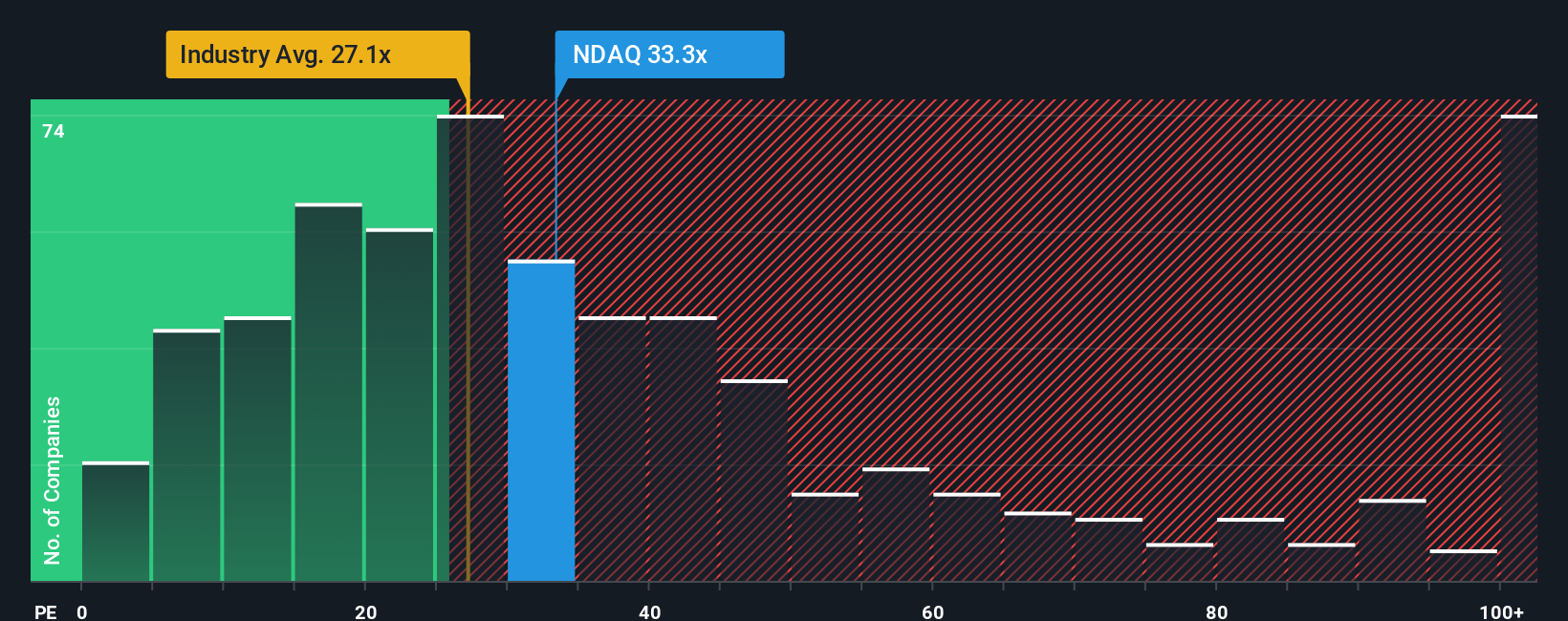

For a profitable, mature business like Nasdaq, the price to earnings ratio is a useful yardstick because it links what investors pay today to the earnings the company is actually generating. In general, faster earnings growth and lower perceived risk justify a higher PE, while slower growth or higher risk pull a fair PE down.

Nasdaq currently trades on about 33.5x earnings, a premium to both the Capital Markets industry average of roughly 25.1x and the peer average near 32.5x. On the surface, that suggests investors are willing to pay up for Nasdaq relative to its sector. However, Simply Wall St goes a step further with its Fair Ratio, an estimate of what PE you would reasonably expect given the company’s earnings growth, profit margins, risk profile, industry and market cap. For Nasdaq, that Fair Ratio is 16.0x, implying the stock is trading at more than double the multiple that would typically be justified by its fundamentals.

Because the current PE is far above the Fair Ratio, this multiple based view also points to Nasdaq looking expensive at today’s price.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1462 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Nasdaq Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, an easy tool on Simply Wall St’s Community page that lets you turn your view of a company into a simple story linked to a financial forecast and, ultimately, a fair value. In practice, a Narrative is your own explanation of what you think will drive Nasdaq’s future revenue, earnings and margins, paired with numbers like growth rates, profit margins and the valuation multiple you believe is reasonable. The platform then connects that story to a dynamic forecast and a Fair Value estimate you can compare directly with today’s share price. This can help you decide how you feel about the stock, and automatically refreshes your Narrative as new news, earnings or guidance arrive. For example, one bullish Nasdaq Narrative on the platform assumes strong execution in higher quality solutions, supporting a fair value in the low $110s. A more cautious Narrative, focused on regulatory and integration risks, pegs fair value closer to $74 and suggests limited upside at current prices.

Do you think there's more to the story for Nasdaq? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com