Reassessing Air Lease (AL) Valuation After a Strong Multi‑Year Share Price Rally

Air Lease (AL) has quietly ridden a strong tailwind this year, with shares up roughly 34% in 2024 and more than 80% over the past 3 years, outpacing many transport peers.

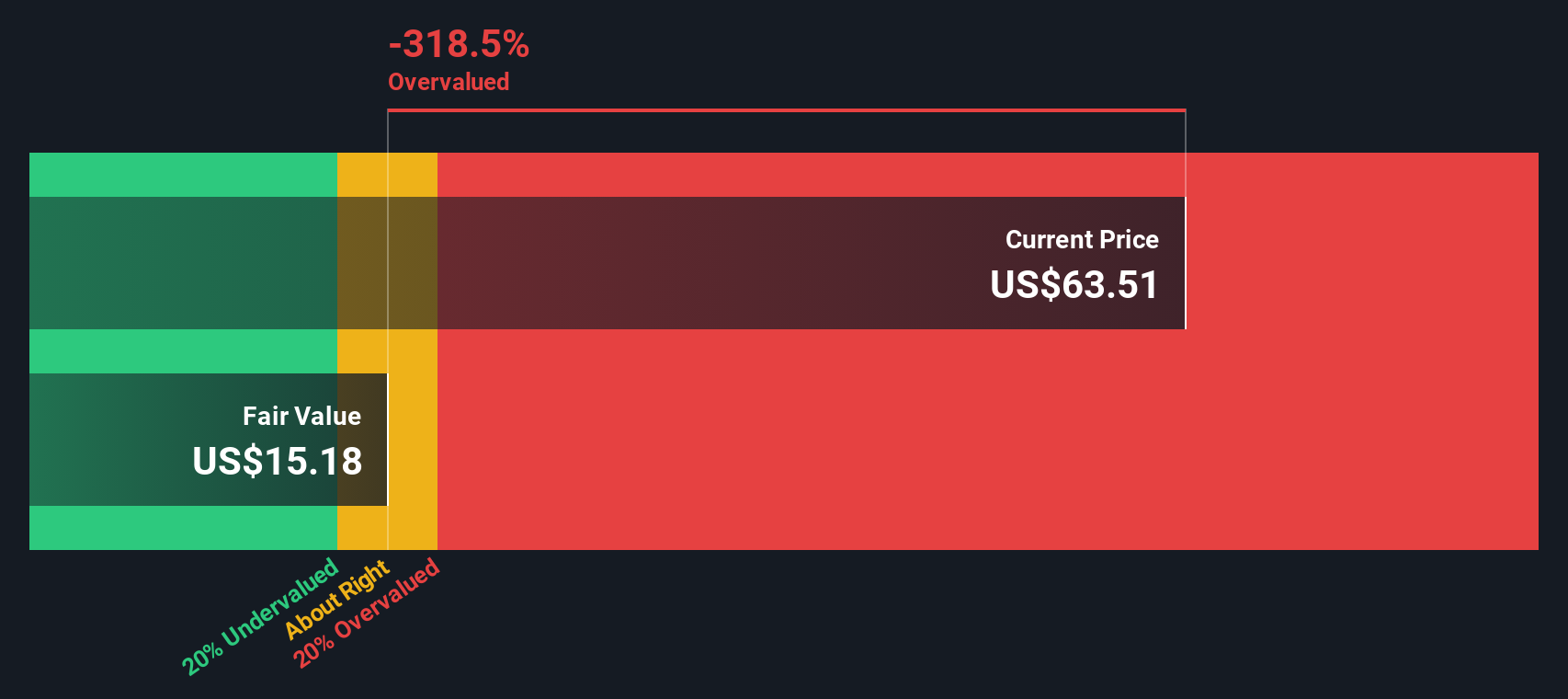

See our latest analysis for Air Lease.

That steady climb has not been about quick spikes in sentiment, with the 2024 share price return of roughly 34% and three year total shareholder return above 80% pointing to momentum that is still building rather than fading.

If Air Lease’s rally has you rethinking where the next leg of returns might come from, this could be a good moment to explore aerospace and defense stocks as potential alternatives or complements.

With shares trading just below analyst targets despite healthy revenue growth, falling profits, and a modest value score, investors now face a key question: is Air Lease still attractive, or is future growth already priced in?

Most Popular Narrative Narrative: 3.8% Undervalued

With Air Lease last closing at $64.15 against a narrative fair value of about $66.67, the prevailing view leans toward modest upside still on the table.

The analysts have a consensus price target of $65.667 for Air Lease based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $72.0, and the most bearish reporting a price target of just $50.0.

Curious why a business with shrinking margins and falling earnings still commands a richer future earnings multiple than today? The answer sits inside the revenue runway, profit reset, and bold re rating that power this fair value story.

Result: Fair Value of $66.67 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, rising financing costs and unpredictable aircraft sales could quickly weaken earnings momentum and challenge the idea that today’s modest undervaluation is sustainable.

Find out about the key risks to this Air Lease narrative.

Another View on Value

Our SWS DCF model paints a very different picture, suggesting Air Lease is trading well above its estimated fair value. While earnings look cheap on headline multiples, the cash flow view points to overvaluation. This leaves investors to decide which lens they trust more.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Air Lease for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 913 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Air Lease Narrative

If you want to dig into the numbers yourself and challenge this perspective, you can build a personalized view in just minutes, Do it your way.

A great starting point for your Air Lease research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Do not stop with a single opportunity; expand your watchlist using the Simply Wall St Screener so you can identify a wider range of potential investments.

- Capture potential mispricings by reviewing these 913 undervalued stocks based on cash flows that may offer strong upside if the market adjusts.

- Capitalize on innovation by scanning these 24 AI penny stocks positioned at the forefront of machine learning and automation.

- Support an income-focused approach by targeting these 12 dividend stocks with yields > 3% that can contribute to total returns through cash payouts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com