Is Western Alliance Still Attractively Priced After Its Post Banking Jitters Recovery?

- If you have been wondering whether Western Alliance Bancorporation is still a bargain after its recovery, you are not alone. This stock has quietly become one of the more interesting value stories in regional banking.

- The share price closed at $86.36 recently and, despite a slightly softer 7 day return of -1.4%, it is still up 9.1% over the last month, 4.2% year to date, and about 4.0% over the past year, with a strong 59.7% gain over three years that hints at substantial long term rerating.

- Recent moves have come as investors reassess regional bank risk, rotate back into financials, and reward balance sheets that appear more resilient than feared during last year's banking jitters. At the same time, the broader conversation around interest rates and credit quality has kept volatility elevated for the sector, which helps explain some of the bumps along the way.

- On our framework, Western Alliance scores a solid 5/6 valuation score, suggesting it screens as undervalued on most of the key checks we run. In the next sections we will unpack those different valuation approaches before circling back to an even richer way of thinking about what the stock is really worth.

Approach 1: Western Alliance Bancorporation Excess Returns Analysis

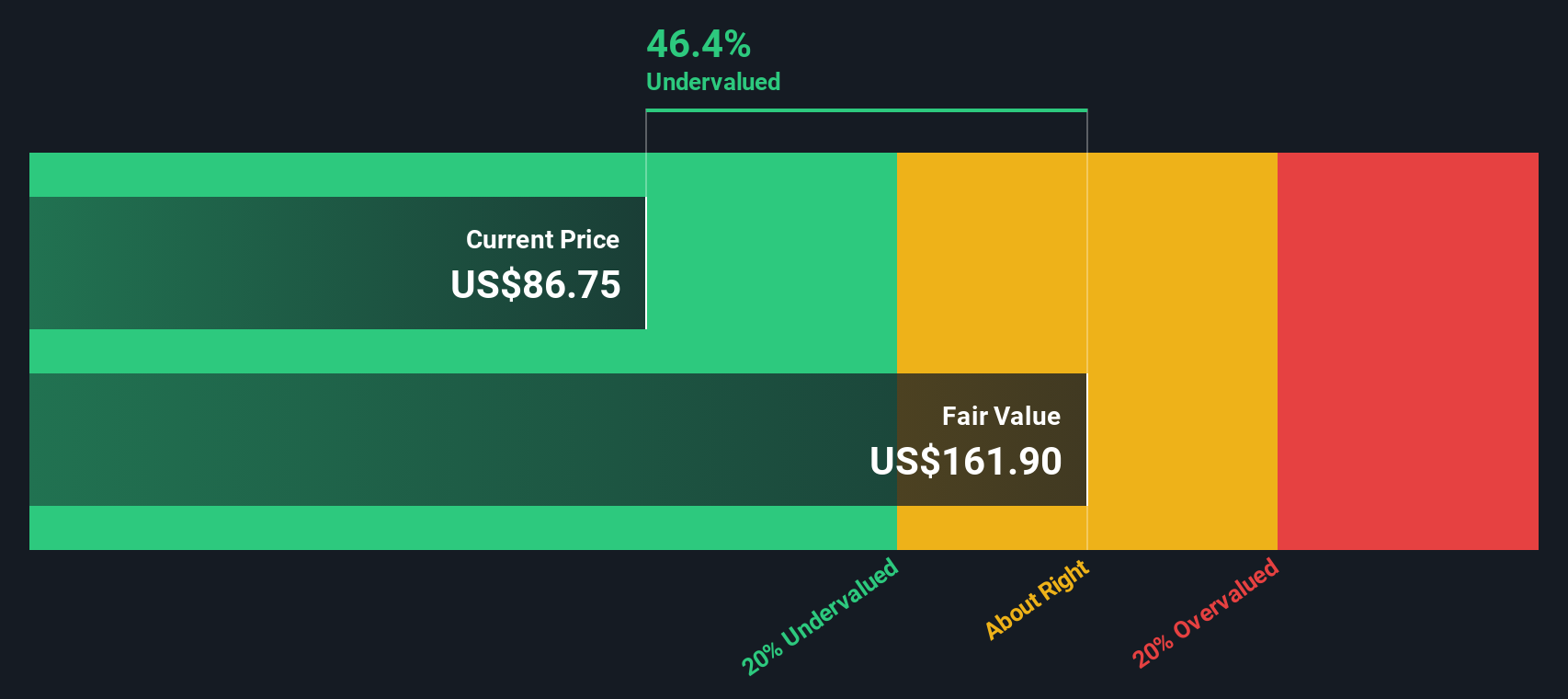

The Excess Returns model looks at how much profit Western Alliance Bancorporation can generate above the return that shareholders reasonably demand, then capitalizes those surplus profits into an estimate of intrinsic value per share.

In this framework, Western Alliance starts from a Book Value of $65.26 per share, projected to grow to a Stable Book Value of $76.46 per share, based on weighted analyst estimates. From that equity base, analysts expect Stable EPS of $10.92 per share, implying an Average Return on Equity of 14.29%.

With a Cost of Equity of $6.27 per share, the bank is estimated to earn an Excess Return of $4.65 per share, a healthy spread that supports a valuation above book value. Translating these excess returns into an intrinsic value, the model indicates a fair value of roughly $170.46 per share.

Compared with the recent share price of $86.36, this suggests the stock is about 49.3% undervalued on an Excess Returns basis, assuming these profitability levels are sustained.

Result: UNDERVALUED

Our Excess Returns analysis suggests Western Alliance Bancorporation is undervalued by 49.3%. Track this in your watchlist or portfolio, or discover 914 more undervalued stocks based on cash flows.

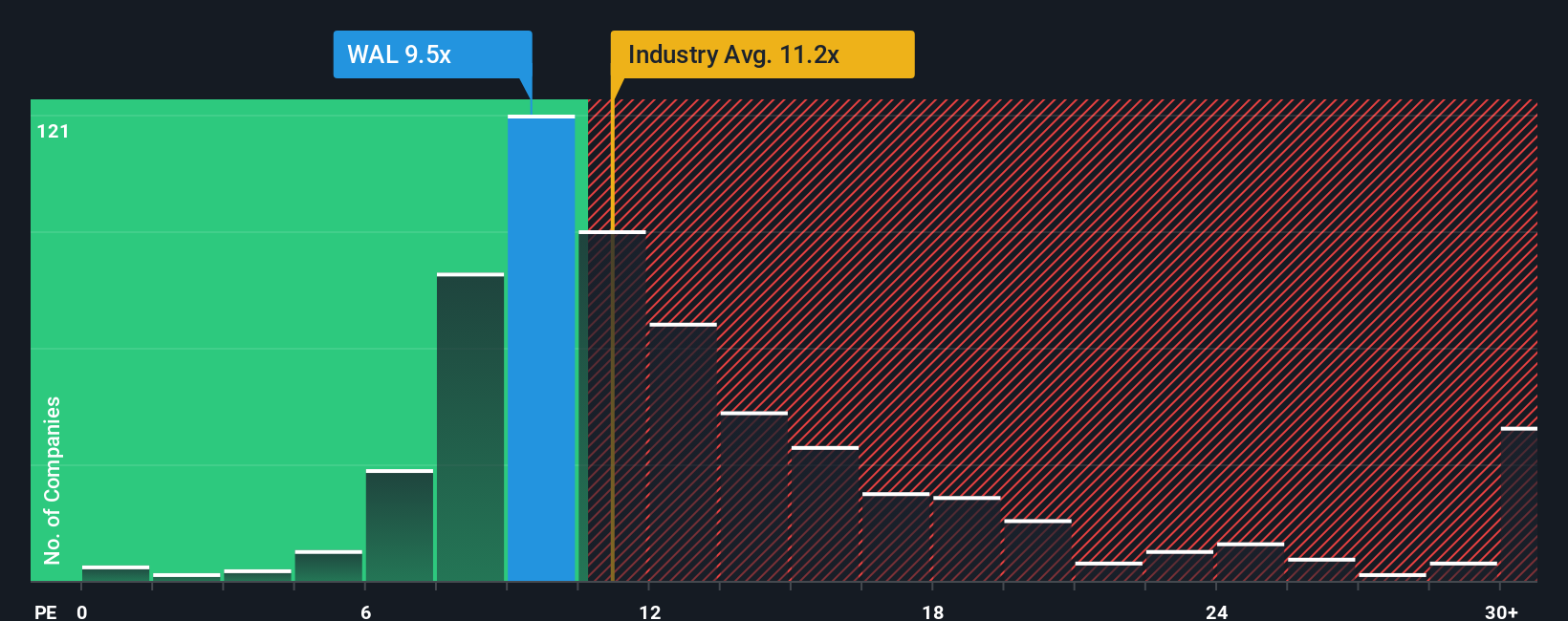

Approach 2: Western Alliance Bancorporation Price vs Earnings

For a profitable bank like Western Alliance, the price to earnings, or PE, ratio is a practical way to gauge how much investors are willing to pay for each dollar of current earnings. In general, faster growth and lower perceived risk justify a higher PE, while slower growth or higher risk argue for a discount to the market.

Western Alliance currently trades on a PE of 10.58x. That sits below both the broader Banks industry average of about 11.94x and the peer group average of roughly 14.40x, suggesting the market is still applying a modest caution premium to the stock.

Simply Wall St’s Fair Ratio framework estimates a PE of 15.75x for Western Alliance, based on factors such as its earnings growth profile, profitability, risk characteristics, industry context and market cap. This is more tailored than simple peer or industry comparisons, because it explicitly blends growth, risk and quality into one benchmark. Against that 15.75x Fair Ratio, the current 10.58x multiple implies the shares trade at a meaningful discount on an earnings basis.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1463 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Western Alliance Bancorporation Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of Western Alliance Bancorporation’s future with a clear financial forecast and a fair value estimate. On Simply Wall St’s Community page, millions of investors use Narratives to spell out the story behind their numbers, including what they expect for future revenue, earnings and margins, and the fair value they believe those assumptions support. A Narrative links three things together: the company’s story, the forecast that flows from that story, and the fair value that drops out of that forecast. It then helps you decide whether to buy or sell by comparing that Fair Value to today’s Price. Narratives also update dynamically as new information, like earnings or news about Western Alliance, comes in. For example, one investor might build a more optimistic Western Alliance Narrative aligned with the higher analyst target of $105.00, while another may focus on commercial real estate risks and align with the more cautious $85.00 view, and both perspectives are visible and testable through their numbers, not just opinions.

Do you think there's more to the story for Western Alliance Bancorporation? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com