MORI TRUST REIT (TSE:8961) Valuation Check After Its Latest Semi-Annual Dividend Increase

MORI TRUST REIT (TSE:8961) just raised its semi annual dividend to ¥1,791 per share, with investors locking in eligibility around late February 2026. This move points to steady confidence in future cash flows.

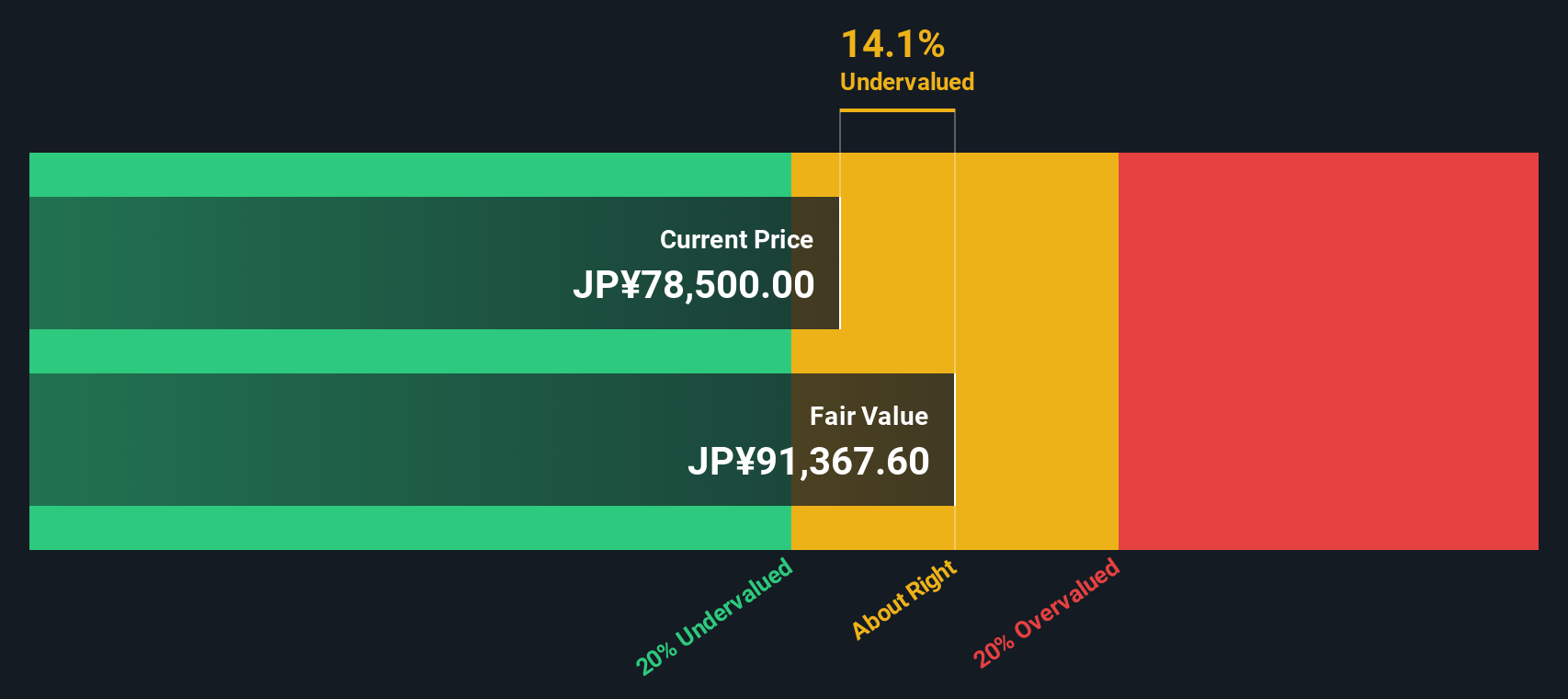

See our latest analysis for MORI TRUST REIT.

The higher payout lands against a solid backdrop, with the share price at ¥78,000 and a strong year-to-date share price return of 25 percent and a robust 1-year total shareholder return of 37.11 percent, suggesting momentum is still building as investors grow more comfortable with the REIT’s income profile.

If MORI TRUST REIT’s steady gains have you thinking about diversification, this could be a good moment to explore fast growing stocks with high insider ownership for other compelling opportunities.

Yet with the units trading slightly above analyst targets but still appearing undervalued on some intrinsic measures, investors now face a key question: is MORI TRUST REIT attractive at today’s price, or is future growth already reflected in the valuation?

Price-to-Earnings of 20.6x: Is it justified?

MORI TRUST REIT screens as attractively priced on several fronts, with our models indicating it trades at a discount despite the recent strong share price performance.

The key lens here is its price to earnings ratio of 20.6 times, a common way to judge what investors are willing to pay today for each unit of current earnings. For a mature, income focused REIT, this multiple helps frame whether the market expects stable, modest growth or is pricing in something more aggressive.

On one hand, MORI TRUST REIT looks good value relative to both its own fundamentals and the broader sector. It is trading at 20.3 percent below our estimate of its fair value, and its price to earnings ratio of 20.6 times compares favourably with our estimated fair price to earnings ratio of 23.7 times, implying the market could still move higher if sentiment aligns with fundamentals.

Against peers, however, the picture is more nuanced. The trust is judged expensive versus a simple peer average, with a price to earnings ratio of 20.6 times versus 20.1 times, but still good value when compared with the JP REITs industry average of 20.9 times. That combination suggests investors are paying a slight premium to direct peers, yet not an excessive one for a vehicle that has outperformed the wider market and industry over the past year.

Explore the SWS fair ratio for MORI TRUST REIT

Result: Price-to-Earnings of 20.6x (UNDERVALUED)

However, softer revenue growth and declining net income could signal pressure on distribution sustainability if property markets cool or financing costs rise.

Find out about the key risks to this MORI TRUST REIT narrative.

Another View: Our DCF Check

While earnings multiples hint at modest undervaluation, our DCF model is more emphatic, suggesting MORI TRUST REIT is trading about 20.3 percent below its estimated fair value of roughly ¥97,808 per unit. If cash flows hold up, is the market underestimating this income stream?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out MORI TRUST REIT for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 913 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own MORI TRUST REIT Narrative

If you see the story differently or want to dig into the numbers yourself, you can build a personalised view of MORI TRUST REIT in just a few minutes, starting with Do it your way.

A great starting point for your MORI TRUST REIT research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Ready for more high conviction ideas?

Do not stop at a single opportunity when you can quickly scan tailored shortlists on Simply Wall St and spot what others may be overlooking today.

- Capture overlooked potential by reviewing these 3633 penny stocks with strong financials, where tiny share prices meet balance sheets that appear resilient and cash flow stories that may be improving.

- Explore the forefront of innovation by assessing these 24 AI penny stocks, hand picked for notable AI exposure and clearly defined business narratives.

- Identify value focused opportunities with these 913 undervalued stocks based on cash flows, highlighting companies that currently trade at prices below estimates of their potential cash generation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com