Will Growing Analyst Optimism on AI Competition Change Teradata's (TDC) Long‑Term Narrative?

- In recent weeks, several Wall Street analysts have shifted to more positive views on Teradata, upgrading their ratings and signaling increased confidence in its business outlook.

- This growing analyst support highlights a changing perception of Teradata’s ability to compete in the evolving analytics and AI infrastructure market.

- Now we’ll explore how this wave of analyst upgrades could reshape Teradata’s investment narrative and its perceived long-term positioning.

Find companies with promising cash flow potential yet trading below their fair value.

Teradata Investment Narrative Recap

To own Teradata, you need to believe it can convert its analytics and AI platform into steadier, higher quality recurring cloud revenue despite ongoing top line pressure and fierce competition from hyperscalers. The latest analyst upgrades from Morgan Stanley and Citizens signal improving confidence, but they do not materially change the near term catalyst around accelerating cloud migrations or the key risk of persistent revenue declines and service contraction.

In this context, Teradata’s ongoing share repurchase program, with more than US$3,855.79 million deployed since 2012 including US$25.9 million in Q3 2025 alone, stands out. For investors, these buybacks sit alongside the recent analyst upgrades as part of the same discussion about earnings quality, cash generation, and how much flexibility Teradata has if revenue headwinds and cloud migration challenges linger longer than expected.

Yet while analyst confidence has improved, investors should still watch the risk that revenue keeps slipping and recurring growth remains dependent on existing customers rather than...

Read the full narrative on Teradata (it's free!)

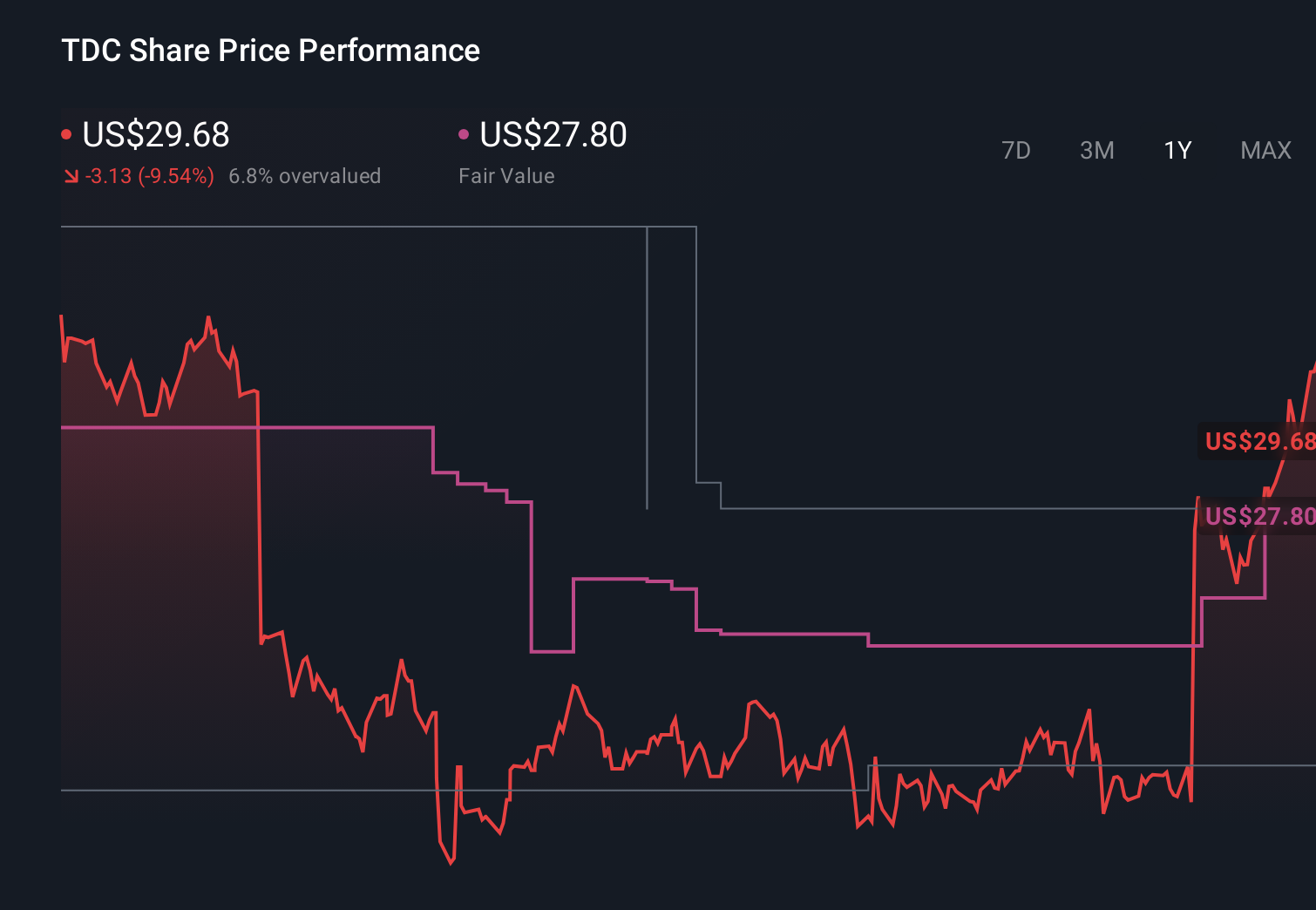

Teradata's narrative projects $1.6 billion revenue and $101.6 million earnings by 2028.

Uncover how Teradata's forecasts yield a $27.80 fair value, a 10% downside to its current price.

Exploring Other Perspectives

Three fair value estimates from the Simply Wall St Community span a wide range, from US$21 to about US$80 per share. Against that backdrop, the recent analyst upgrades and ongoing revenue headwinds show why it can help to weigh several different views on Teradata’s future performance.

Explore 3 other fair value estimates on Teradata - why the stock might be worth over 2x more than the current price!

Build Your Own Teradata Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Teradata research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Teradata research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Teradata's overall financial health at a glance.

Looking For Alternative Opportunities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- AI is about to change healthcare. These 29 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 24 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com