Rocket Lab (RKLB): Valuation Check After Landmark SDA Contract Win and Record Electron Launch Year

Rocket Lab (RKLB) just landed its largest ever U.S. Space Development Agency contract to build 18 missile warning satellites, while also setting a record year for flawless Electron launches. The stock has surged accordingly.

See our latest analysis for Rocket Lab.

That backdrop of record government wins and flawless launches has clearly shifted how investors see Rocket Lab, with an 81.8% 1 month share price return and a 2055.87% 3 year total shareholder return pointing to strong, still building momentum rather than a one off spike.

If this pace in space has your attention, it could be a good time to scan other aerospace opportunities through aerospace and defense stocks and see which names share similar tailwinds.

Yet with RKLB now trading above some analyst targets and showing a significant multi-year run, are investors still underestimating the long-term defense and launch opportunity, or has the market already priced in its future growth?

Most Popular Narrative: 21.1% Undervalued

KiwiInvest’s narrative points to a fair value well above Rocket Lab’s last close of $77.18, framing today’s price as a long runway rather than a peak.

These estimates produce a current fair value of ~$98 per share. The main determinant of daily stock prices over the next 10 years will be the PE ratio the market ascribes to Rocket Labs. This will fluctuate massively over time as an amplified measure of current investor confidence in the spaceflight business, the space economy, the global economy and global markets in general. Throughout, Rocket Lab will continue to innovate and grow. Periods of lower PEs will offer good buying opportunities. Only extremely high PEs represent true overvalued status, given the long term prospects of this company.

Curious how Rocket Lab gets to that future valuation from today’s losses and heavy investment cycle? The narrative leans on aggressive growth, rising margins and a punchy profit multiple. Want to see how those moving parts combine into one bold space blueprint.

Result: Fair Value of $98 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, investors still need to weigh execution risk on Neutron, along with the possibility of tighter defense budgets slowing contract wins and revenue growth.

Find out about the key risks to this Rocket Lab narrative.

Another View on Valuation

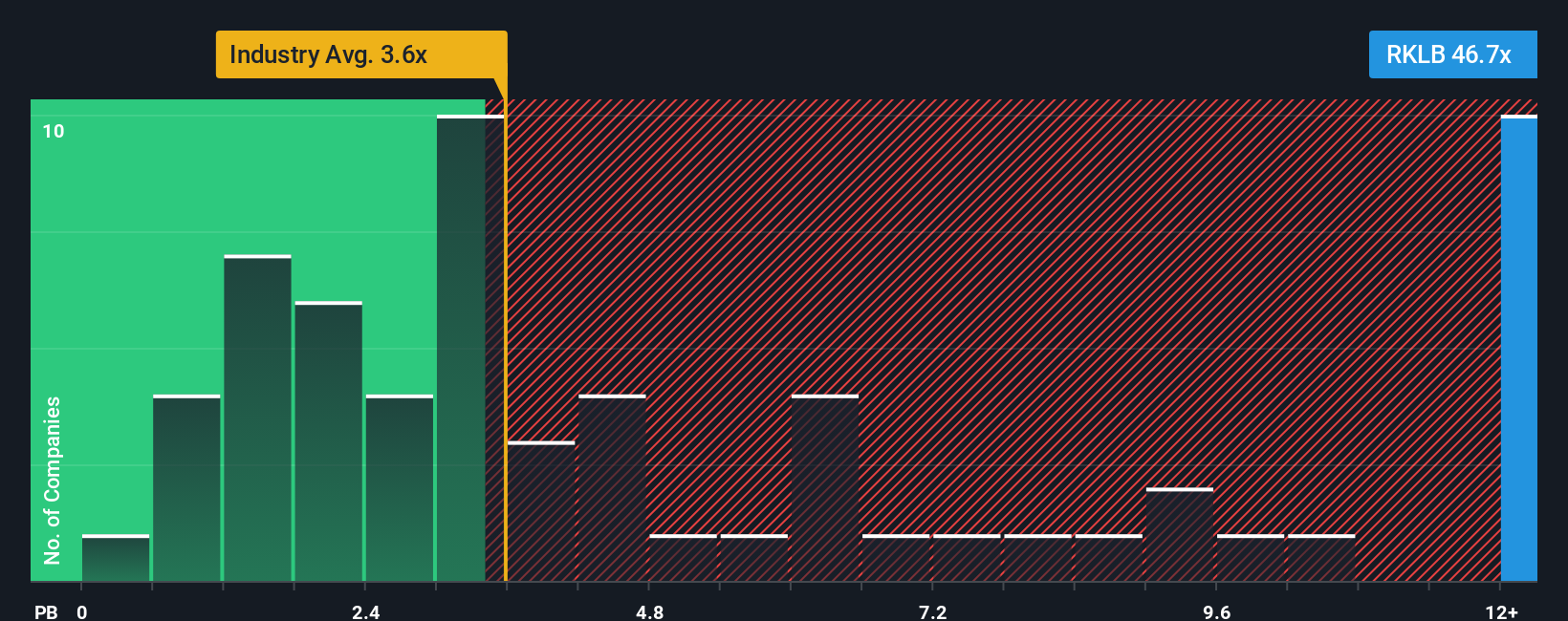

While KiwiInvest sees Rocket Lab as about 21% undervalued, our pricing lens tells a different story. On a price to book basis RKLB trades at 32.2 times, far richer than both US Aerospace and Defense peers at 3.8 times and its own fundamentals.

That kind of premium can work if growth and execution stay flawless. It also leaves little room for launch delays, contract hiccups or funding shocks before sentiment reverses. Is this a justified ticket to the space backbone, or a valuation orbit that is hard to sustain?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Rocket Lab Narrative

If you see Rocket Lab’s story differently or want to test your own assumptions against the numbers, you can build a fresh view in minutes: Do it your way.

A great starting point for your Rocket Lab research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before you move on, lock in an edge by scanning fresh opportunities through the Simply Wall Street Screener, so you are not chasing yesterday’s winners.

- Capitalize on mispriced quality by targeting companies that look cheap on cash flow using these 908 undervalued stocks based on cash flows before the crowd catches on.

- Explore innovation trends by focusing on early-stage names in these 24 AI penny stocks that may reshape entire industries.

- Strengthen your income strategy by pinpointing reliable payers through these 10 dividend stocks with yields > 3% to help you manage your search for yield.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com