Is BMW Still Attractive After Its Strong 2025 Rally And EV Expansion Plans?

- Wondering if Bayerische Motoren Werke is still good value after its strong run, or if most of the upside has already been priced in? This breakdown will help you separate narrative from numbers.

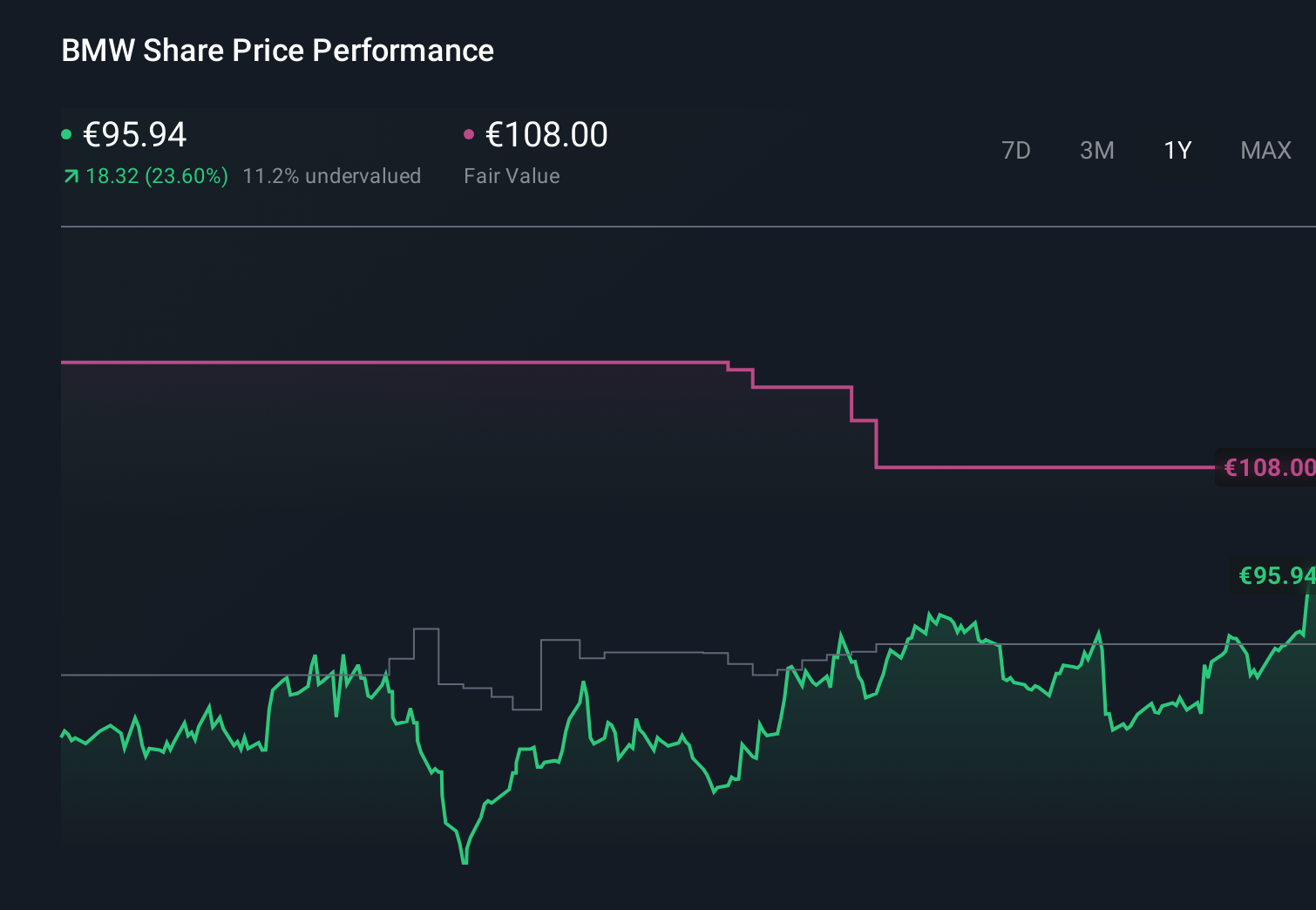

- Despite slipping 1.7% over the last week, the stock is still up 8.9% over 30 days, 18.6% year to date and 27.1% over the past year, with a hefty 69.5% gain over five years that highlights how the market has been reassessing its long term prospects.

- Recent headlines have focused on BMW doubling down on its electric and hybrid lineup, expanding investments in battery technology and software defined vehicles. Investors often interpret these moves as signals of long term competitiveness rather than short term hype. At the same time, industry wide debates about EV demand, regulation and supply chain resilience have added some volatility, making it even more important to distinguish sustainable value from cyclical sentiment.

- Right now BMW scores a solid 5 out of 6 on our valuation checks, suggesting it looks undervalued on most metrics. Next we will walk through the key valuation approaches behind that score and finish with a more holistic way to think about what the market might be missing. Analyst Price Targets don't always capture the full story. Head over to our Company Report to find new ways to value Bayerische Motoren Werke.

Approach 1: Bayerische Motoren Werke Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth by projecting the cash it can generate in the future and discounting those cash flows back to today, using an appropriate rate to reflect risk and the time value of money.

For Bayerische Motoren Werke, the latest twelve month free cash flow is about €646 Million. Analysts expect this to rise significantly, with projections moving into the mid single digit Billions of euros over the coming years. By 2029, free cash flow is forecast to reach roughly €6.95 Billion, and Simply Wall St extrapolates these cash flows further out using a two stage Free Cash Flow to Equity framework.

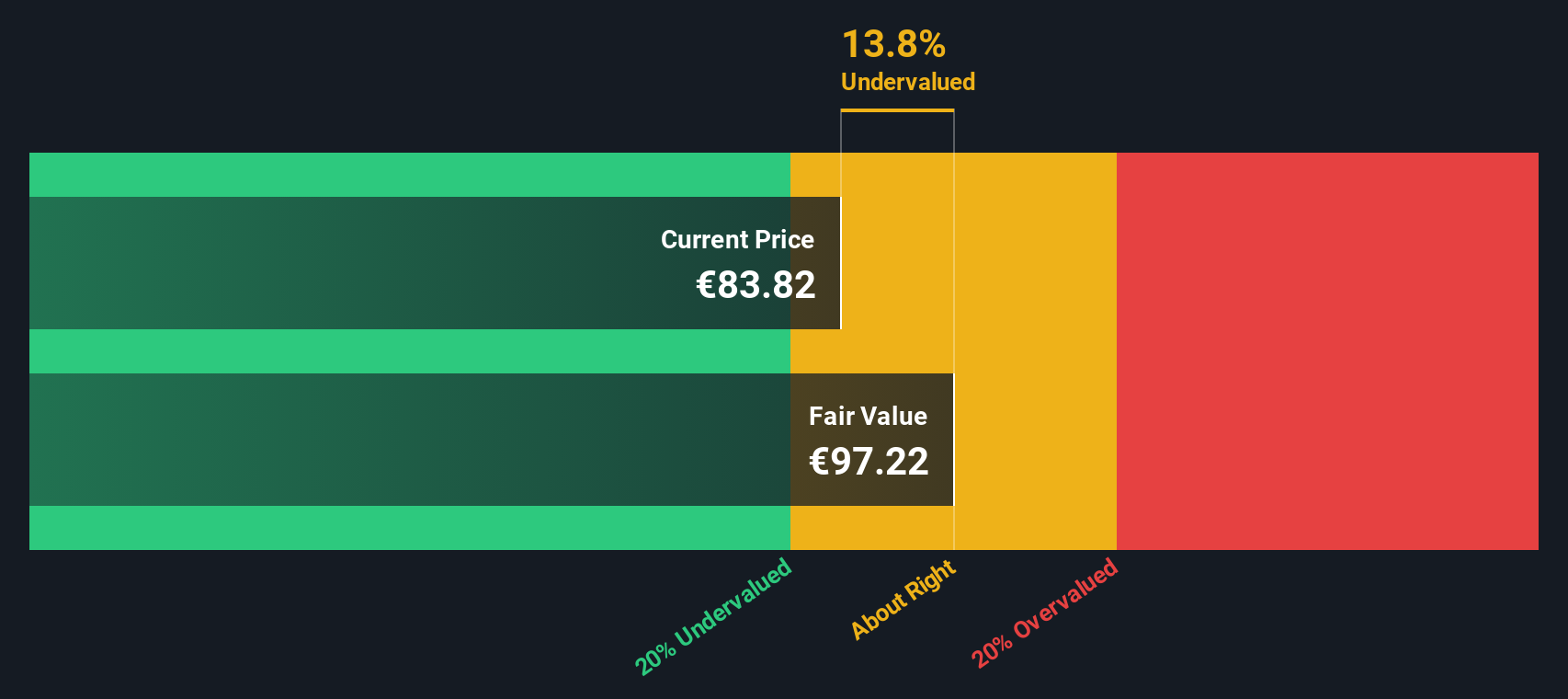

When these projected cash flows are discounted back to the present and aggregated, the model arrives at an estimated intrinsic value of about €134.20 per share. Compared with the current market price, this implies the stock is trading at roughly a 31.0% discount, indicating it appears materially undervalued on a cash flow basis.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Bayerische Motoren Werke is undervalued by 31.0%. Track this in your watchlist or portfolio, or discover 908 more undervalued stocks based on cash flows.

Approach 2: Bayerische Motoren Werke Price vs Earnings

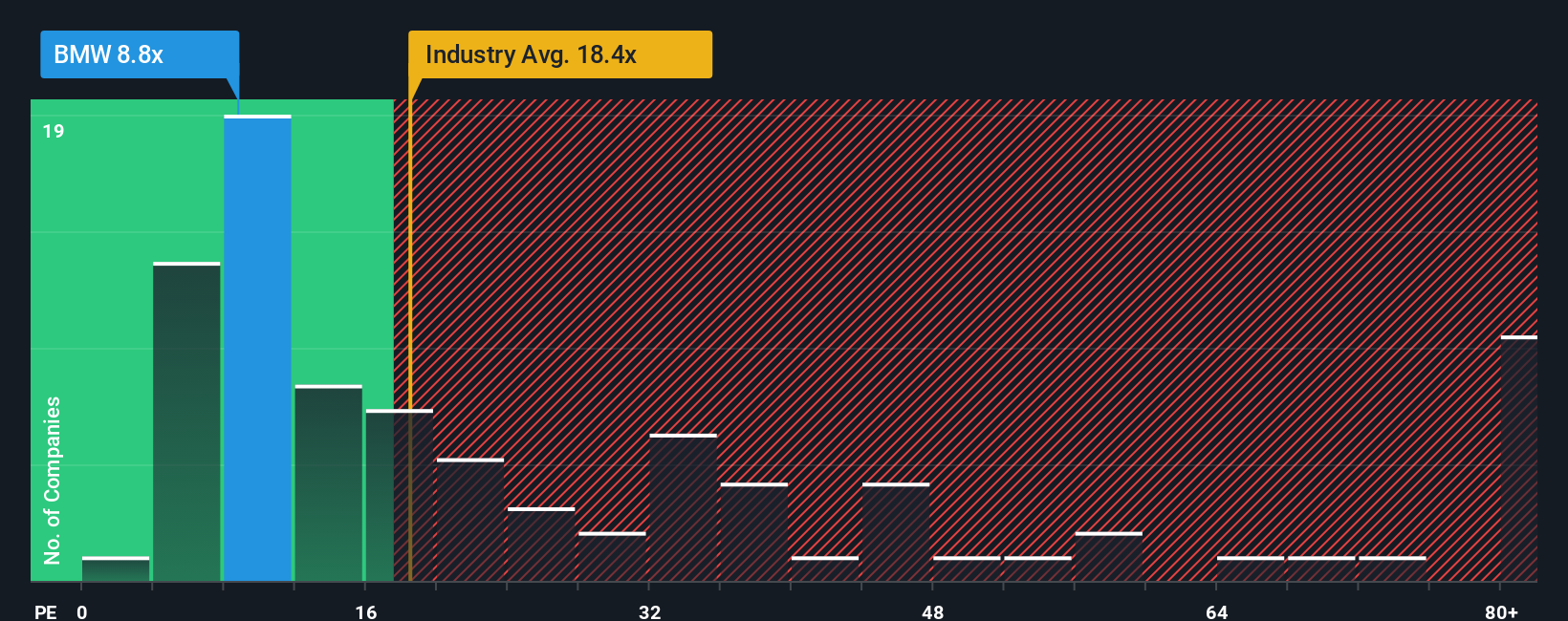

For a consistently profitable business like Bayerische Motoren Werke, the Price to Earnings (PE) ratio is a useful way to see how much investors are paying for each euro of current earnings. In general, companies with stronger and more reliable growth and lower perceived risk tend to justify a higher PE multiple, while slower growing or riskier names usually deserve a lower one.

BMW currently trades on a PE of about 8.13x, which is well below both the Auto industry average of roughly 18.69x and the broader peer group at around 23.90x. On the surface, that discount suggests the market is pricing BMW more cautiously than many of its competitors.

Simply Wall St’s Fair Ratio framework goes a step further by estimating what PE multiple would be reasonable for BMW, given its specific mix of earnings growth, profit margins, industry positioning, size and risk profile. For BMW, this Fair Ratio comes out at about 12.16x, implying the stock may warrant a higher multiple than it currently receives. With the actual PE sitting well below this Fair Ratio, the PE analysis suggests that BMW shares may be attractively priced relative to this framework.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1457 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Bayerische Motoren Werke Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to describe the story you believe about a company and then connect that story directly to numbers like future revenue, earnings, margins and ultimately a fair value estimate.

A Narrative on Simply Wall St links three things together: your view of BMW’s business, a financial forecast that reflects that view, and a derived fair value which you can then compare to today’s share price to decide whether it looks like a buy, hold or sell.

These Narratives are easy to use and live inside the Community section of Simply Wall St, where millions of investors publish their perspectives and have them turned into dynamic forecasts that automatically refresh when new data, such as earnings releases or major news, comes in.

For example, one BMW Narrative on the platform assumes stronger EV adoption, higher margins and a fair value around €135 per share, while a more cautious Narrative uses slower growth, lower margins and a fair value closer to €89. This shows how different investors can reasonably arrive at very different conclusions from the same starting point.

For Bayerische Motoren Werke however, we will make it really easy for you with previews of two leading Bayerische Motoren Werke Narratives:

🐂 Bayerische Motoren Werke Bull Case

Fair value: €135.07

Implied undervaluation vs last close: 31.4%

Forecast revenue growth: 5%

- Sees BMW as a long term participant in premium EVs, supported by the Neue Klasse platform, resilient luxury demand and a recovering China market.

- Expects margins to move toward a range of 8% to 10% as higher margin software, digital services and premium models scale, which in turn supports a rerating to an 8x to 10x P/E.

- Views the current low P/E and strong brand, along with battery and alternative fuel investments, as a potential mispricing that could offer meaningful upside if execution stays on track.

🐻 Bayerische Motoren Werke Bear Case

Fair value: €88.59

Implied overvaluation vs last close: 4.6%

Forecast revenue growth: 3.38%

- Builds on analyst assumptions of moderate growth and only modest margin improvement, which leads to a fair value close to today’s price.

- Highlights structural pressures in China, tariff and regulatory risks and intense BEV competition as forces that could cap profitability and constrain multiples.

- Notes that a lagging autonomous strategy and volatile EV policy frameworks may weaken BMW’s long term growth resilience, making the stock appear closer to fully priced.

Do you think there's more to the story for Bayerische Motoren Werke? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com