How Pediatric FUROSCIX Expansion And New Patents At MannKind (MNKD) Has Changed Its Investment Story

- MannKind Corporation recently reported that the FDA approved a supplemental New Drug Application expanding FUROSCIX on-body Infusor use to pediatric patients weighing at least 43 kg, while the USPTO issued five new patents potentially protecting the FUROSCIX ReadyFlow Autoinjector through 2040.

- By simultaneously widening the eligible patient population and reinforcing long-term patent coverage for its FUROSCIX platform, MannKind has strengthened both the clinical and competitive foundation of this drug-device franchise.

- Next, we’ll explore how expanded pediatric approval for FUROSCIX could influence MannKind’s investment narrative and future growth assumptions.

These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

MannKind Investment Narrative Recap

To own MannKind, you need to believe its drug device platforms can broaden beyond Afrezza and Tyvaso DPI into a more diversified, durable portfolio. The FUROSCIX pediatric expansion and ReadyFlow patents appear additive, but the most important near term catalyst remains FDA review of the FUROSCIX ReadyFlow Autoinjector, while execution risk around commercialization costs and market uptake still looms largest.

The December 1 FDA acceptance of the sNDA for the FUROSCIX ReadyFlow Autoinjector, with a July 26, 2026 PDUFA date, ties directly into this latest pediatric and IP news by underscoring how central FUROSCIX has become to MannKind’s next phase of potential growth and to reducing its dependence on a narrow revenue base.

Yet even with these approvals and patents, investors should still be aware of concentration risk in a small set of products and...

Read the full narrative on MannKind (it's free!)

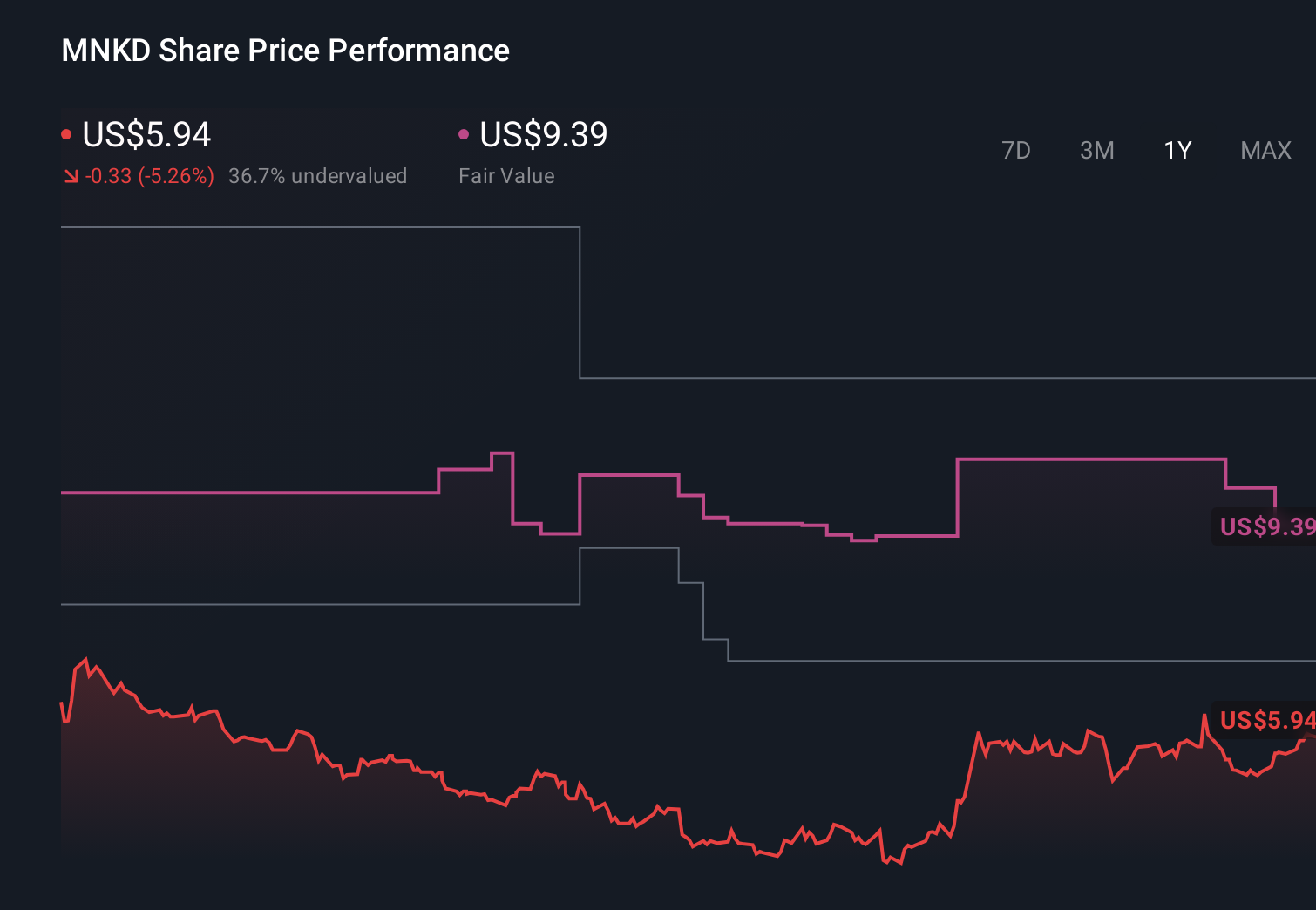

MannKind's narrative projects $437.5 million revenue and $70.4 million earnings by 2028.

Uncover how MannKind's forecasts yield a $9.61 fair value, a 62% upside to its current price.

Exploring Other Perspectives

Four fair value estimates from the Simply Wall St Community span roughly US$7.40 to US$18.25 per share, underscoring how far opinions can diverge. You should weigh those views against MannKind’s reliance on a concentrated portfolio and consider how that could affect longer term performance.

Explore 4 other fair value estimates on MannKind - why the stock might be worth just $7.42!

Build Your Own MannKind Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your MannKind research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free MannKind research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate MannKind's overall financial health at a glance.

Searching For A Fresh Perspective?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- We've found 10 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com