Freeport-McMoRan Inc.'s (NYSE:FCX) P/E Is Still On The Mark Following 26% Share Price Bounce

Despite an already strong run, Freeport-McMoRan Inc. (NYSE:FCX) shares have been powering on, with a gain of 26% in the last thirty days. The last 30 days bring the annual gain to a very sharp 36%.

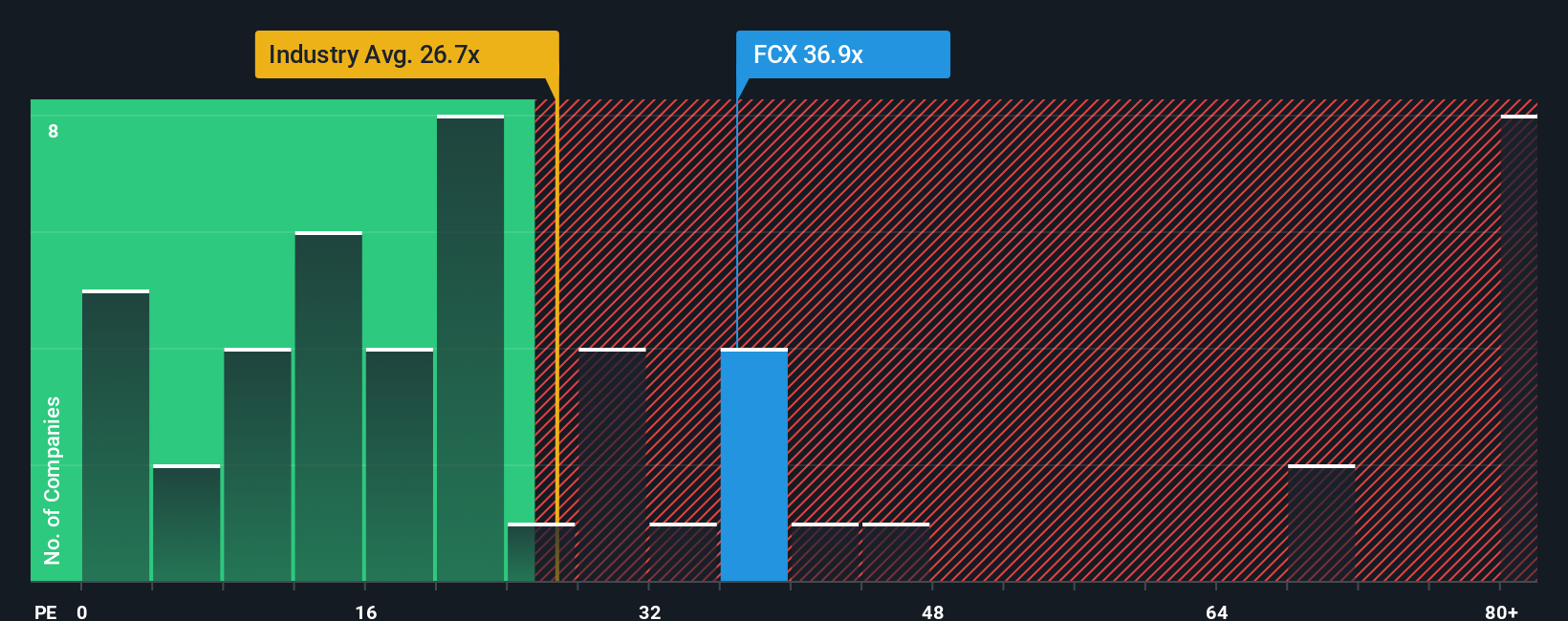

Following the firm bounce in price, Freeport-McMoRan may be sending very bearish signals at the moment with a price-to-earnings (or "P/E") ratio of 36.9x, since almost half of all companies in the United States have P/E ratios under 19x and even P/E's lower than 11x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

Freeport-McMoRan could be doing better as it's been growing earnings less than most other companies lately. One possibility is that the P/E is high because investors think this lacklustre earnings performance will improve markedly. If not, then existing shareholders may be very nervous about the viability of the share price.

Check out our latest analysis for Freeport-McMoRan

Does Growth Match The High P/E?

In order to justify its P/E ratio, Freeport-McMoRan would need to produce outstanding growth well in excess of the market.

If we review the last year of earnings growth, the company posted a worthy increase of 3.4%. Ultimately though, it couldn't turn around the poor performance of the prior period, with EPS shrinking 46% in total over the last three years. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Turning to the outlook, the next three years should generate growth of 25% each year as estimated by the analysts watching the company. With the market only predicted to deliver 12% each year, the company is positioned for a stronger earnings result.

In light of this, it's understandable that Freeport-McMoRan's P/E sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Final Word

Shares in Freeport-McMoRan have built up some good momentum lately, which has really inflated its P/E. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of Freeport-McMoRan's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. Unless these conditions change, they will continue to provide strong support to the share price.

And what about other risks? Every company has them, and we've spotted 1 warning sign for Freeport-McMoRan you should know about.

You might be able to find a better investment than Freeport-McMoRan. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.