It's Down 27% But GCL Global Holdings Ltd (NASDAQ:GCL) Could Be Riskier Than It Looks

To the annoyance of some shareholders, GCL Global Holdings Ltd (NASDAQ:GCL) shares are down a considerable 27% in the last month, which continues a horrid run for the company. The recent drop completes a disastrous twelve months for shareholders, who are sitting on a 91% loss during that time.

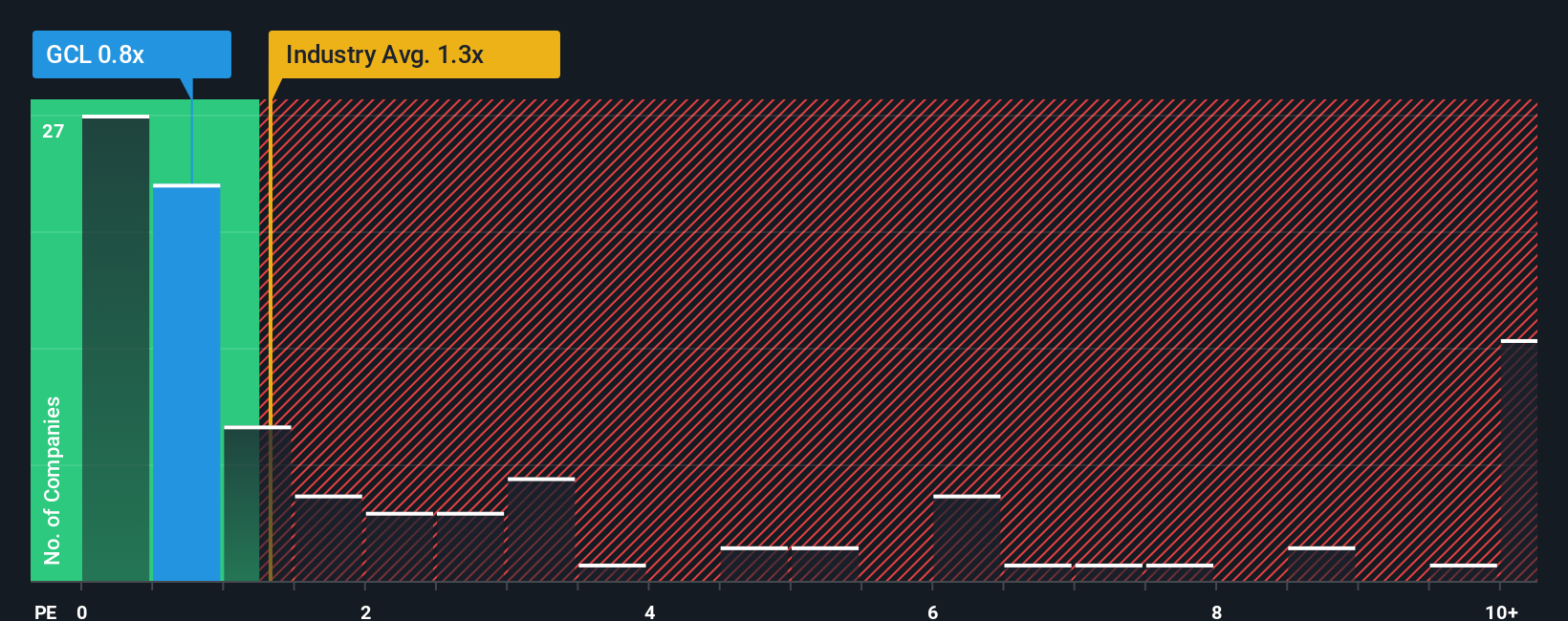

Although its price has dipped substantially, GCL Global Holdings' price-to-sales (or "P/S") ratio of 0.8x might still make it look like a buy right now compared to the Entertainment industry in the United States, where around half of the companies have P/S ratios above 1.3x and even P/S above 6x are quite common. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

Check out our latest analysis for GCL Global Holdings

How GCL Global Holdings Has Been Performing

With revenue growth that's exceedingly strong of late, GCL Global Holdings has been doing very well. Perhaps the market is expecting future revenue performance to dwindle, which has kept the P/S suppressed. Those who are bullish on GCL Global Holdings will be hoping that this isn't the case, so that they can pick up the stock at a lower valuation.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on GCL Global Holdings' earnings, revenue and cash flow.Is There Any Revenue Growth Forecasted For GCL Global Holdings?

There's an inherent assumption that a company should underperform the industry for P/S ratios like GCL Global Holdings' to be considered reasonable.

Taking a look back first, we see that the company grew revenue by an impressive 46% last year. The strong recent performance means it was also able to grow revenue by 116% in total over the last three years. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Comparing that recent medium-term revenue trajectory with the industry's one-year growth forecast of 19% shows it's noticeably more attractive.

With this in mind, we find it intriguing that GCL Global Holdings' P/S isn't as high compared to that of its industry peers. It looks like most investors are not convinced the company can maintain its recent growth rates.

What We Can Learn From GCL Global Holdings' P/S?

The southerly movements of GCL Global Holdings' shares means its P/S is now sitting at a pretty low level. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

We're very surprised to see GCL Global Holdings currently trading on a much lower than expected P/S since its recent three-year growth is higher than the wider industry forecast. Potential investors that are sceptical over continued revenue performance may be preventing the P/S ratio from matching previous strong performance. While recent revenue trends over the past medium-term suggest that the risk of a price decline is low, investors appear to perceive a likelihood of revenue fluctuations in the future.

And what about other risks? Every company has them, and we've spotted 2 warning signs for GCL Global Holdings (of which 1 doesn't sit too well with us!) you should know about.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.